When done well, investing in stocks is among the most effective ways to build long-term wealth.

Here's a step-by-step guide to investing money in the stock market to help ensure you're doing it the right way.

1. Determine your investing approach

1. Determine your investing approach

The first thing to consider is how to start investing in stocks the right way for you. Some investors choose to buy individual stocks, while others take a less active approach.

Try this. Which of the following statements best describes you?

- I'm an analytical person and enjoy crunching numbers and doing research.

- I hate math and don't want to do a ton of "homework."

- I have several hours each week to dedicate to stock market investing.

- I like to read about the different companies I can invest in, but I don't have any desire to dive into anything math related.

- I'm a busy professional and don't have the time to learn how to analyze stocks.

The good news is that regardless of which of these statements you agree with, you're still a great candidate to become a stock market investor. The only thing that will change is the how.

The different ways to invest in the stock market

Individual stocks

You can invest in individual stocks if -- and only if -- you have the time and desire to thoroughly research and evaluate stocks on an ongoing basis. If this is the case, we 100% encourage you to do so. It is entirely possible for a smart and patient investor to beat the market over time. On the other hand, if things like quarterly earnings reports and moderate mathematical calculations don't sound appealing, there's absolutely nothing wrong with taking a more passive approach.

Index funds

In addition to buying individual stocks, you can choose to invest in index funds, which track a stock index like the S&P 500. When it comes to actively vs. passively managed funds, we generally prefer the latter (although there are certainly exceptions). Index funds typically have significantly lower costs and are virtually guaranteed to match the long-term performance of their underlying indexes. Over long periods, the S&P 500 has produced total annualized returns of about 10%, and performance like this can build substantial wealth over time.

Robo-advisors

Finally, another option that has exploded in popularity in recent years is the robo-advisor. This is a brokerage that essentially invests your money on your behalf in a portfolio of index funds appropriate for your age, risk tolerance, and investing goals. Not only can a robo-advisor select your investments, but many will also optimize your tax efficiency and make changes over time automatically.

Robo Advisor

2. Decide how much to invest

2. Decide how much you will invest in stocks

First, let's talk about the money you shouldn't invest in stocks. The stock market is no place for money that you might need within the next five years, at a minimum.

While the stock market will almost certainly rise over the long run, there's simply too much uncertainty in stock prices in the short term -- in fact, a drawdown of 20% in any given year isn't unusual, and occasional drops of 40% or even more do happen. Stock market volatility is normal and should be expected.

Such sharp drops have happened a couple of times in recent history. During the 2007–09 bear market caused by the financial crisis, the S&P 500 dropped by more than 50% from its previous highs. In 2020, during the early days of the COVID-19 pandemic, the market plunged by more than 40% before it started to recover.

So here's what you shouldn't be investing:

- Your emergency fund

- Money you'll need to make your child's next few tuition payments

- Next year's vacation fund

- Money you're socking away for a down payment, even if you will not be prepared to buy for a few years

Asset allocation

Now let's talk about what to do with your investable money -- that is, the money you won't likely need within the next five years. How you distribute it is a concept known as asset allocation, and a few factors come into play here. Your age is a major consideration, and so are your particular risk tolerance and investment goals.

Let's start with your age. The general idea is that as you get older, stocks gradually become a less desirable place to keep your money. If you're young, you have decades ahead of you to ride out any ups and downs in the market, but this isn't the case if you're retired and rely on your investment income.

Here's a quick rule of thumb that can help you establish a ballpark asset allocation. Subtract your age from 110. This is the approximate percentage of your investable money that should be in stocks (including mutual funds and exchange-traded funds, or ETFs, that are stock-based). The remainder should be in fixed-income investments like bonds or high-yield certificates of deposit (CDs). You can then adjust this ratio up or down depending on your particular risk tolerance.

Bonds

For example, let's say that you are 40 years old. This rule suggests that 70% of your investable money should be in stocks, with the other 30% in fixed-income investments like bonds or high-yield CDs. If you're more of a risk taker or are planning to work past a typical retirement age, you may want to shift this ratio in favor of stocks. On the other hand, if you don't like big fluctuations in your portfolio, you might want to modify it in the other direction.

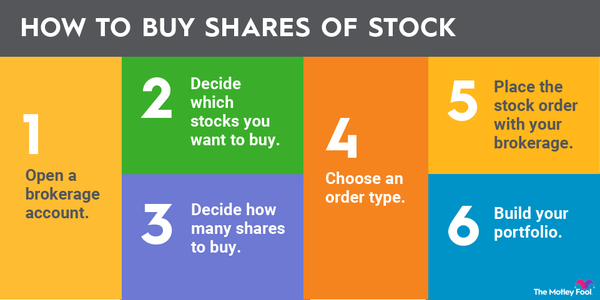

3. Open an investment account

3. Open an investment account

All the advice about investing in stocks for beginners doesn't do you much good if you don't have any way to actually buy stocks. To do this, you'll need a specialized type of account called a brokerage account.

These accounts are offered by companies such as E*Trade, Charles Schwab, and many others, as well as by newer app-based platforms like Robinhood and SoFi. Opening a brokerage account is typically a quick and painless process that takes only minutes. You can easily fund your brokerage account via an electronic funds transfer, by mailing a check, or by wiring money. Or, if you have an existing brokerage account or a 401(k) or similar retirement account from an old employer, you may be able to transfer these into your new brokerage account.

Opening a brokerage account is generally easy, but you should consider a few things before choosing a particular broker:

Type of account

First, determine the type of brokerage account you need. For most people who are just trying to learn stock market investing, this means choosing between a standard brokerage account and an individual retirement account (IRA).

Both account types will allow you to buy stocks, mutual funds, and ETFs. The main considerations here are why you're investing in stocks and how easily you want to be able to access your money.

If you want easy access to your money, are just investing for a rainy day, or want to invest more than the annual IRA contribution limit, you'll probably want a standard brokerage account.

On the other hand, if your goal is to build up a retirement nest egg, an IRA is a great way to go. These accounts come in two main varieties -- traditional and Roth IRAs -- and there are some specialized types of IRAs for self-employed people and small business owners, including the SEP-IRA and SIMPLE IRA. IRAs are very tax-advantaged places to buy stocks, but the downside is that it can be difficult to withdraw your money until you get older.

One interesting feature of Roth IRAs that can be appealing is the ability to withdraw your contributions (but not your investment profits) at any time and for any reason. This can be a big positive feature for people who might not want their money tied up until retirement.

Compare costs and features

The majority of online stockbrokers have eliminated trading commissions for online stock trades. So most (but not all) are on a level playing field as far as costs are concerned, unless you're trading options or cryptocurrencies, both of which still have trading fees with most brokers who offer them.

However, there are several other big differences. For example, some brokers offer customers a variety of educational tools, access to investment research, and other features that are especially useful for newer investors. Others offer the ability to trade on foreign stock exchanges. And some have physical branch networks, which can be nice if you want face-to-face investment guidance.

There's also the user-friendliness and functionality of the broker's trading platform to consider. I've used quite a few of them and can tell you firsthand that some are far more clunky than others. Many will let you try a demo version before committing any money, and if that's the case, I highly recommend it.

4. Choose your stocks

4. Choose your stocks

Now that we've answered the question of how you buy stocks, if you're looking for some great beginner-friendly investment ideas, here is a list of our top stocks to buy and hold this year to help get you started.

Of course, in just a few paragraphs, we can't go over everything you should consider when selecting and analyzing stocks, but here are the important concepts to master before you get started:

- Diversify your portfolio.

- Invest only in businesses you understand.

- Avoid high-volatility stocks until you get the hang of investing.

- Always avoid penny stocks.

- Learn the basic metrics and concepts for evaluating stocks.

It's a good idea to learn the concept of diversification, meaning that you should have a variety of different types of companies in your portfolio. However, I'd caution against too much diversification. Stick with businesses you understand -- and if it turns out that you're good at (or comfortable with) evaluating a particular type of stock, there's nothing wrong with one industry making up a relatively large segment of your portfolio.

Buying flashy, high-growth stocks may seem like a great way to build wealth (and it certainly can be), but I'd caution you to hold off on these until you're a little more experienced. It's wiser to create a "base" for your portfolio with rock-solid, established businesses or even with mutual funds or ETFs.

If you want to invest in individual stocks, you should familiarize yourself with some of the basic ways to evaluate them. Our guide to value investing is a great place to start. There we help you find stocks trading for attractive valuations. If you want to add some exciting long-term growth prospects to your portfolio, our guide to growth investing is a great place to begin.

5. Continue investing

5. Continue investing

Here's one of the biggest secrets of investing, courtesy of the Oracle of Omaha himself, Warren Buffett. You do not need to do extraordinary things to get extraordinary results. (Note: Warren Buffett is not only the most successful long-term investor of all time, but he is also one of the best sources of wisdom for your investment strategy.)

The most surefire way to make money in the stock market is to buy shares of great businesses at reasonable prices and hold on to the shares for as long as the businesses remain great (or until you need the money). If you do this, you'll experience some volatility along the way, but over time, you'll enjoy excellent investment returns.

Investing FAQs

How do I start investing in stocks?

There are a few things you need to do before you start investing. First, you need to determine your risk tolerance, and then you need to decide if you want to invest in individual stocks or more passive investments like ETFs. Then determine how much money you can invest for the long term and figure out which brokerage or robo-advisor is best for you. And, perhaps most importantly, when you’re just getting started, take advantage of the educational resources at your disposal and learn all you can.

How should beginners buy stocks?

The first step in buying stock is to open a brokerage account, which is a specialized financial account designed to buy, hold, and sell investments. There are many different brokers, but beginners should generally choose one that is easy to use and doesn't have a minimum initial deposit requirement. However, the best broker for you depends on your particular risk tolerance and your specific investment strategy.

Can I invest $100 in stocks?

You can get started investing with a relatively small amount of money, and thanks to the emergence of fractional share trading, you can build a diverse portfolio with just $100. If you have $100 to invest, here are our best suggestions for what to do with it:

- Use a micro-investing app or robo-advisor.

- Invest in a stock index mutual fund or exchange-traded fund.

- Open a brokerage account that offers fractional share investing and invest in your favorite companies.

- Open an IRA.

- Put it in your 401(k).

How much should I invest in stocks as a beginner?

There’s no one-size-fits-all answer to this question, since we all have different financial situations. But a general rule is that you shouldn’t invest any of your savings that you’re going to need within the next few years. It’s not uncommon for the market to decline by 20% or more in any given year. And once you start investing, it’s a great strategy to regularly add money to your investment account over time.

How do I open a brokerage account?

Here's your step-by-step guide to opening a brokerage account:

- Determine the type of brokerage account you need.

- Compare costs and incentives.

- Consider the services and conveniences offered.

- Decide on a brokerage firm.

- Fill out the application for a new account.

- Fund the account.

- Start researching investments.

What is the S&P 500?

The S&P 500 (also known as the Standard & Poor's 500) is a stock index that consists of the 500 largest companies in the U.S. Its performance is generally considered the best indicator of how U.S. stocks are performing overall.

How much money do I need to invest to make $1,000 a month?

If you're investing in stocks, your returns will not be consistent from month to month, so it's impossible to say for sure. If you're investing in fixed-income instruments like bonds or CDs, you can divide $12,000 ($1,000 per month, expressed yearly) by your expected annual percentage yield (APY) to figure out how much you need to invest.