2016 was a forgettable year for CVS Health (CVS -0.62%). Management stunned investors by announcing that Walgreens Boots Alliance (NASDAQ: WBA) had struck two huge deals that threaten to rob the company of more than 40 million retail prescriptions each year. Understandably, traders didn't take the news well.

However, while that update wasn't great, there are still plenty of reasons to believe CVS Health's stock will bounce back from here. Below, we'll take a closer look at three of them.

Image source: CVS Health.

1. Growth drivers are still in place

While CVS is best known as a retail pharmacy chain, the company actually pulls in revenue from several different sources. That diversity helps the company to continue to grow even when one of its divisions suffers a temporary setback.

The largest contributor to CVS Health's top line is its pharmacy benefits management (PBM) business. The company earns a small fee in exchange for helping other institutions that provide healthcare to their members -- think unions, employers, governments -- control their spending on pharmaceuticals. This business is all about scale, which is advantageous for CVS since it's currently the second largest player in the country. With a 97% customer retention rate, this business still looks primed to deliver for shareholders.

Investors should also benefit from the expansion of CVS's MinuteClinic empire. These in-store clinics provide patients with convenient and low-cost access to a variety of basic health services. The continued rollout of these clinics should help bring new customers into a CVS store.

Finally, shareholders should remember that CVS is still in the early stages of realizing the benefits of its massive acquisitions of Target's pharmacy business and Omnicare. As time passes, management should be able to wring out more cost savings and bring in new customers.

Given all of the above, perhaps it isn't all that surprising to see that CEO Larry Merlo still believes the company can deliver 10% EPS growth from here.

2. Taking care of shareholders

CVS Health has had a long and storied history of using its financial might to benefit shareholders. With the company poised for profitable growth in the years ahead, I think we can expect more of the same.

Image source: Getty Images.

Looking at the company's dividend, CVS recently announced that it would be bumping its payout by 18% in 2017. That brings its annual payment up to $2 per share, which, at current prices, gives the company a market-beating yield of 2.4%. That number should be quite attractive to income investors.

Turning to the company's share repurchase program, CVS Health has spent more than $13.5 billion buying back its shares over the past three years. That looks like money well spent, as it has helped to meaningfully lower the company's share count.

CVS Average Diluted Shares Outstanding (Quarterly) data by YCharts.

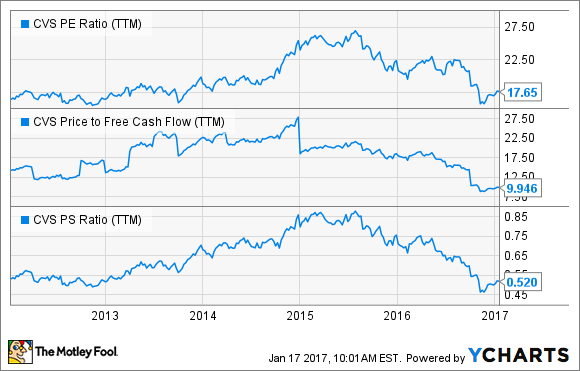

3. It's cheap!

While CVS's stock has recovered a bit from its 2016 lows, there's no denying that the company still trades at a historically low valuation. Take a look at this chart that shows CVS's price-to-earnings ratio, price to free-cash-flow ratio, and price-to-sales ratio over the past five years.

CVS PE Ratio (TTM) data by YCharts.

All three metrics clearly show that CVS is currently trading at a valuation it hasn't seen in years. While Walgreen's knack for making deals did cause CVS to lower its guidance, I can't help but feel that the selling is a bit overdone.

While 2016 wasn't the best year for shareholders, CVS Health continues to look poised for long-term prosperity. If management can continue to execute its plan, then I could easily see shares rising from here.