Can the party last?

So far, 2017 has been a fertile year for payout hikes -- income investors have plenty of reason to be optimistic going forward. Yet there's no telling whether the next 10 months or so will be similarly rich, so we should enjoy the soiree while it lasts. Here's a trio of stocks that are about to make their shareholders incrementally richer.

IMAGE SOURCE: GETTY IMAGES.

The Finish Line

Shoe and accessories retailer The Finish Line (FINL) is taking another step forward with its quarterly dividend, lifting it by $0.01 -- an even 10% -- to $0.11 per share.

The company is a fairly steady and reliable dividend payer and raiser. It has hiked its payout once every year, at that same $0.01 amount, since 2010.

This should help provide some comfort to shareholders, a group that hasn't been too cheerful lately. Their company closed 2016 on a down note, with the release of dispiriting Q3 results just before Christmas. For the period, its same-store growth rate came in under 1%, while revenue crawled up by only 3% to just under $372 million, and net loss nearly doubled to over $40 million.

The situation is a little better when we turn to the company's cash flow statements. Operating cash flow has held up pretty well over the past few years despite the red ink on the bottom line, and free cash flow remains more than sufficient to fund the dividend payouts. So for now, I wouldn't worry about the viability of the new distribution, but it would be nice if the company started to improve those uninspiring fundamentals.

FINL Net Income (TTM) data by YCharts.

The Finish Line's enhanced dividend is to be paid on March 13 to stockholders of record as of Feb. 24. At the most recent closing share price, it would yield 2.5%, which is comfortably above the nearly 2% of dividend-paying stocks on the S&P 500 index.

BlackRock

When you're the world's largest asset manager, you've got plenty of cash swirling around. Luckily for BlackRock's (BLK 0.55%) stockholders, their company is willing to share some of it. BlackRock has declared that its upcoming quarterly dividend will be $2.50 per share -- 9% higher than the preceding payout.

Additionally, the company's board has authorized an expansion of its stock repurchase program, by 6 million shares. This lifts the total authorization to 9 million at present.

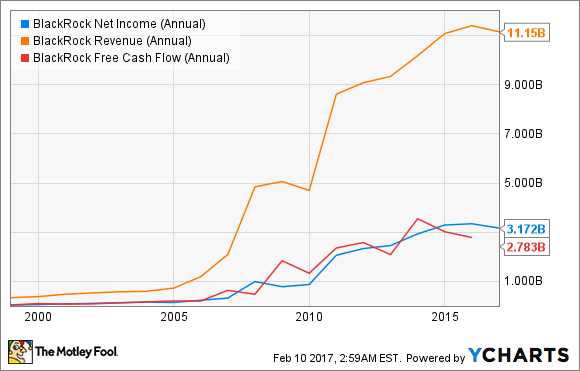

BlackRock has more than enough money to support these moves. Last year, it set a new annual company record for total assets under management, a pile that grew by 11% on a year-over-year basis to hit nearly $5.15 trillion. Much of that was due to the increasing popularity of index funds, a company specialty.

Although revenue and net income both slumped, by a respective 2% and 3% to $11.15 billion and $3.2 billion, the company remains a powerful money-making machine. Its four most recently available cash flow statements indicate that free cash flow is well outpacing the company's dividend payouts, with enough left over to keep that stock repurchase program humming.

BLK Net Income (Annual) data by YCharts.

The new BlackRock dividend will be dispensed on March 23 to stockholders of record as of March 6. At the current share price, it would yield 2.6%.

The company did not specify a time limit for the newly expanded share buyback initiative.

Omega Healthcare Investors

Yet again, Omega Healthcare Inevstors (OHI -0.50%) is boosting its quarterly dividend. The specialty real estate investment trust is a habitual and constant raiser, lifting its distribution every quarter since initiating the payout in mid-2013. The company has declared a $0.62 per share dividend, a 2% bump over its predecessor.

This raise is the 17th in a row, a streak that reaches back to 2012. Over that time, the payout has risen steadily from $0.47 per share to the present level.

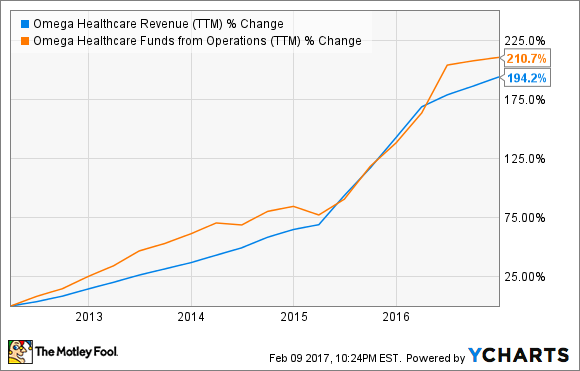

In terms of fundamentals, Omega's fiscal 2016 was a good year. Thanks in no small part to a spate of recent acquisitions, revenue saw a 21% rise over the 2015 figure, to nearly $901 million. Meanwhile, adjusted funds from operations -- the critical measure of profitability for REITs -- zoomed ahead by 22% to almost $689 million, or $3.42 per share.

OHI Revenue (TTM) data by YCharts.

It doesn't look like the party will continue, though, as Omega is only guiding for adjusted funds from operation of $3.40 to $3.44 for this fiscal year. These decreased figures are mostly due to planned capital renovations, but they don't take into account new investments or other line items regarding sales and acquisitions. Another concern is that the REIT's payout ratio (i.e., the percentage of net income paid as dividends) has been scarily high of late, ranging from 117% to 165% over the past four years.

However, if we look at the cash dividend payout ratio (substituting funds from operation for net income), those numbers fall steeply -- 80% to 88%. Those are still fairly tall figures, though, so current and potential Omega investors should beware.

Omega Healthcare Investors' upcoming dividend is to be handed out on Feb. 15 to shareholders of record as of Jan. 31. It would boast a very attractive yield of just over 8% on the current share price.