It may be an imperfect measure of a stock's value, but the price-to-earnings ratio, or P/E, remains a useful tool for investors. The current or trailing P/E is calculated by dividing the current stock price by the combined EPS of the last four quarterly periods, while the forward P/E is calculated by instead using the projected EPS of the next four quarterly periods. Both can serve as a quick test that allow you to decide if a company warrants further research.

But tools are only useful if you know how to use them. Both trailing and forward metrics can be used to assess the relative value of a stock compared to the broader market, peers in the same industry, or even against a company's own historical values. That can make it a confusing or tricky metric to use reliably, which makes it important not to rely too heavily on the P/E ratio alone. That said, investors looking for the best low-P/E stocks to buy in February may want to consider General Motors (GM 4.37%) and Braskem (BAK 1.48%).

Image source: Getty Images.

No love for automakers

The auto industry has stormed back from the depths of the Great Recession and performed exceptionally well in the last several years. However, automakers trade well below the P/E ratio of the S&P 500, which currently sits at about 26. Ford Motor Company and Toyota trade at a P/E ratio of about 11, while General Motors trades near an unbelievably low P/E of 6.

What gives? Mr. Market seems to be pricing in the possibility of an downward trend in the cyclical industry and slow sales in certain global regions, but that doesn't mean investors should head for the exits. General Motors in particular is an intriguing low-P/E stock for several reasons.

First, the company continues to cut costs to boost profitability, which was doubly aided by 9% growth in revenue last year. General Motors achieved earnings of $6.00 per share in 2016, which bested EPS of $5.91 in 2015 and $1.66 in 2014. The automaker expects for full-year 2017 EPS to settle somewhere between $6.00 and $6.50 -- and that was before it announced its intention to find a buyer for its money-losing European operations, which trimmed about $0.17 off last year's EPS.

Second, General Motors roared to $16.5 billion in operating cash flow in 2016. That was well ahead of the $11.7 billion and $10.1 billion achieved in the prior two years, respectively. Healthier cash flow means a reduced burden for borrowing and an increased ability to invest back into the business, including novel technologies. Speaking of, the automaker has gotten off to strong start with its all-electric Chevy Bolt, which promises to play an important role in General Motors' future.

And third, if improving operations aren't appeasing enough to investors looking at the stock, then an oversized dividend that yields over 4% may serve as added persuasion.

Betting on Brazil

Braskem hasn't been spared from its home country's misery in recent years. A historic recession that began in early 2014 has cooled the once high-octane emerging market. Zika virus continues to sap productivity and put a damper on promising demographics. And last but not least, the political scandal that led to the impeachment of Brazil's last elected president just so happened to center on Braskem's two parent companies, Petrobras and Odebrecht.

The good news is that things appear to be getting better for Brazil -- and Braskem. The stock surged to 60% gains in 2016 -- all of which came after August -- as investors began to focus once again on scrutinizing operations rather than reading political tea leaves. There are reasons to be excited about the direction of the company.

Management used the recession as a catalyst to improve the balance sheet and the efficiency of operations. Net income rose to $869 million in 2015, up from just $308 million and $234 million in the prior two years, respectively.. In the first nine months of 2016, the company's cash position swelled 14% and EBITDA soared to $2.5 billion during the period, which was 15% higher than the year-ago period.

Better yet, the company is far from done growing. Braskem is currently the largest producer of biopolymers in the world and has invested heavily in new ethylene cracking facilities, which should make it the lowest-cost provider of several high-demand petrochemicals for years to come. Existing operations have also benefited from efficiency-minded investments: The company set a record for cracker facility utilization in Brazil at 96% during the third quarter of last year.

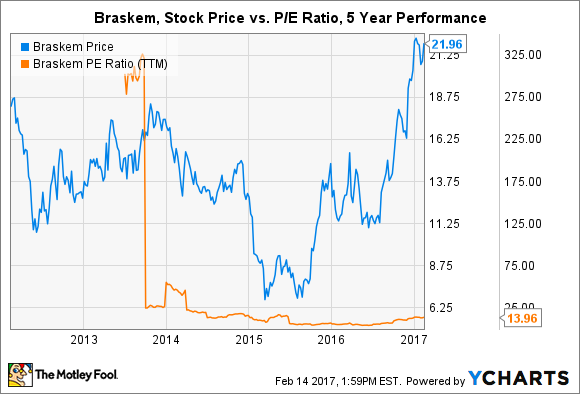

Successful execution against its goals has led to results for investors. However, the company still trades at a historically low P/E ratio of 12. One reason: Braskem carries an unhealthy amount of debt. At the end of September it boasted a debt-to-assets ratio of 66% -- which was actually down markedly from just a few quarters prior. The good news is that non-core asset sales and healthy operating cash flow should allow the company to continue improving its balance sheet over time. Throw in an admittedly infrequent dividend that yields over 7%, and investors have more than enough reasons to consider buying the stock.

What does it mean for investors?

It can be easy for investors to rely too heavily on P/E ratios when researching stocks, but it's an imperfect metric. Sometimes stocks that appear cheap are full of problems, while stocks that appear expensive could be relative bargains based on growth. For General Motors and Braskem, I think Mr. Market is failing to fully appreciate what each stock has to offer, which is why they're among the best low-P/E stocks to buy in February.