Earlier this year, the now-former Federal Reserve governor in charge of regulatory matters, Daniel Tarullo, made a subtle but significant announcement that could free Bank of America (BAC 1.70%) and other big banks up to return more than 100% of their earnings to shareholders.

Since the financial crisis, the nation's biggest banks have had to ask for the Fed's permission to increase their dividends and stock buybacks. The regulator's newfound veto power over bank capital plans came as part of the Dodd-Frank Act of 2010, which significantly scaled up banks' compliance burdens.

The U.S. Federal Reserve Building at sunset. Image source: Getty Images.

The Fed could reject a bank for one of two reasons. First, on quantitative grounds, if the bank wasn't projected to have enough capital to remain well-capitalized through the most extreme version of the annual stress test. And second, on qualitative grounds, if the Fed concluded that a bank didn't have an adequately sophisticated capital planning process in place.

Few banks have problems with the quantitative aspect, as they can forecast relatively accurately the impact on their capital given the underlying stress test assumptions. It's the qualitative grounds that banks take issue with, as they're fuzzier and more subjective.

Wells Fargo's new CEO Tim Sloan made this point at an industry conference last year:

When you step back and think, should large financial institutions be stressing their balance sheet and their business model before they decide how much capital to pay out to shareholders? Of course, they should. I mean, it makes all the sense in the world. But we've moved from an objective standard to now maybe subjective [standards] are more important than objective. That would be something that you look at.

Bank of America's Chairman and CEO Brian Moynihan echoed these remarks at the same conference:

For us as a company, just because of where we are, it's about capital return. ... It's about getting certainly around the ability to have access to your capital return once you've met all the hurdles. And whether those hurdles move up or down because of various peoples' points of view, the issue is the industry's above them, and now we need to be able to get the capital out.

The good news for banks, in turn, is that this aspect of the test could soon go away. Former Fed governor Tarullo made this point on his way out the door earlier this year, suggesting that it may be time to end the qualitative part of the annual stress test.

And it seems safe to say that the people most likely to be selected by President Trump to fill the three open seats on the Fed's governing committee will agree, given his vow on the campaign trail to reduce regulations on banks and other financial service providers.

Of all the banks that would benefit from this change, few would welcome it as much as Bank of America. Its efforts to meaningfully increase the amount of capital it returns to shareholders have been throttled since the crisis in large part because of the qualitative portion of the stress tests.

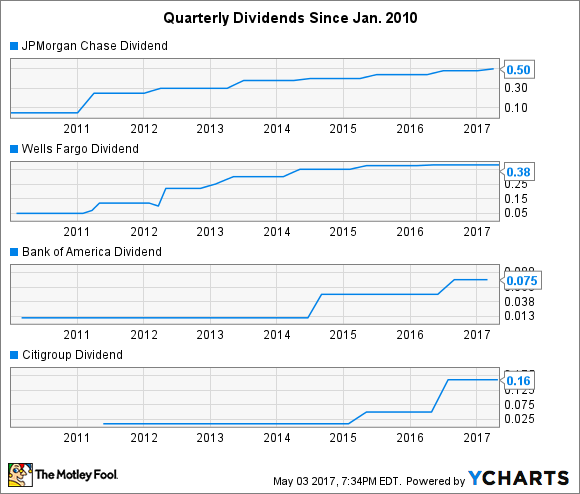

Bank of America has increased its dividend only twice since the financial crisis, compared to annual raises at JPMorgan Chase and Wells Fargo. Image source: YCharts.com.

If that were to go away, it would enable the North Carolina-based bank to purge its balance sheet of an enormous surplus of pent-up capital, easily translating into a total payout ratio in excess of 100% beginning as early as next year.