Home Depot (HD -0.92%) thrived in a challenging operating environment in 2020. While shopping behavior was reshaped through the pandemic, the home improvement leader added over $15 billion to its sales base and booked soaring profits through the first three quarters of the year.

Those successes contributed to another market-beating year for shareholders, and Home Depot stock has more than doubled since early 2016. But the best might still be ahead for investors.

Let's look at a few reasons the chain could be setting new records in another year.

Image source: Getty Images.

Stronger growth

Home Depot's 2020 sales gains might not seem impressive given that consumer spending shifted dramatically toward home improvement projects because of COVID-19 containment efforts. Rival Lowe's (LOW -0.72%) grew faster, in fact, with comparable-store sales soaring 30% in the third quarter compared to Home Depot's 24% increase.

There are good reasons to expect the industry leader to regain its top growth spot in the coming quarters, though. Management said it made progress getting inventory levels back near normal in late November following several months of unusually high demand. Shoppers have never been happier with the business' service levels, either. That success showed up in Home Depot's double-digit growth in both customer traffic and average spending last quarter, and should lift the business well into 2021.

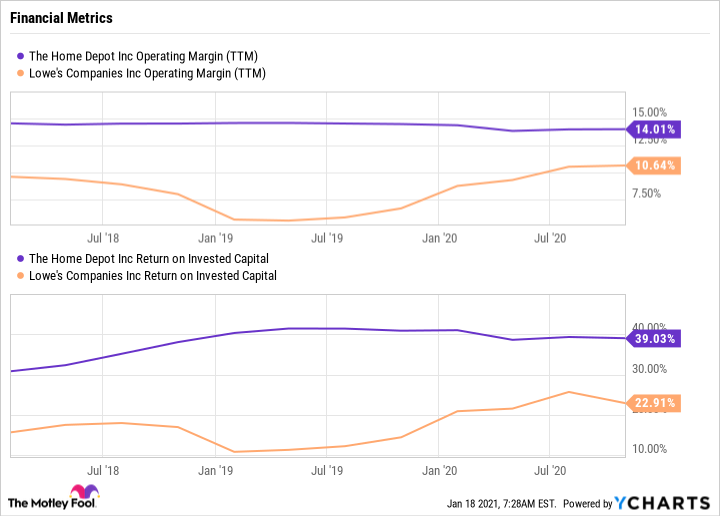

Higher profits

Even if Home Depot manages to just keep pace with the broader industry, investors can bank on outsize returns from the business. The chain's operating margin still sits well ahead of Lowe's and is over 14% in 2020 despite extra labor, safety, and supply chain costs due to COVID-19.

Meanwhile, Home Depot's executive team continues to show off its capital allocation skills. Lifted by a mix of stock buybacks and cheap bond sales, return on invested capital is sitting near 40% today.

HD operating margin (TTM) data by YCharts. TTM = trailing 12 months.

The chain shifted its strategy in recent weeks by announcing the acquisition of HD Supply for $8 billion. That buyout is likely to boost the overall value of the business by adding new growth opportunities and pushing profit margins even higher. Investors should be watching for management's detailed forecast about this buyout when Home Depot announces fourth-quarter results in late February.

Risks and volatility

The biggest threat to Home Depot's success in 2021 is an industry downturn, and that's no small risk. Economic growth could easily disappoint if the recession doesn't end quickly, and it's also possible that some of the chain's blockbuster sales gains last year simply pulled forward projects from future quarters. Today, most investors who follow the stock are predicting growth to slow to about 1% from the expected 17% Home Depot will log for the full 2020.

Investors who don't mind a little volatility might still be happy buying this stock now even though the short run looks cloudy. But if you're a bit more risk averse, you might prefer to make a move after seeing Home Depot's final 2020 report, which is set for Feb. 23. Either way, you'll probably be happy to own this high-performing business over the long term.