The market is supposed to be a hyper-efficient weighing machine in the long run, but that's not always the case. Those mismatches between market value and business performance often create outsize investing opportunities.

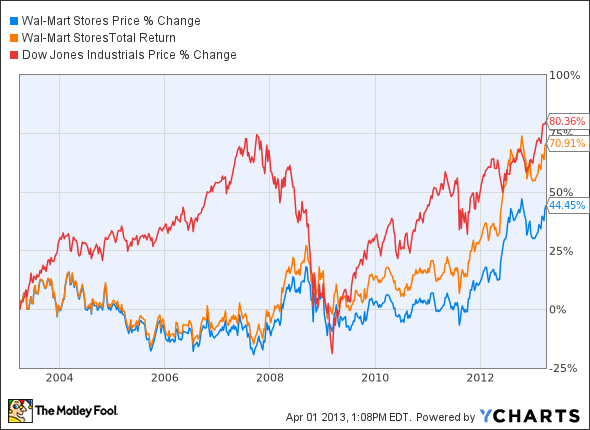

For an example of this, take a look at retail giant Wal-Mart Stores (WMT -0.49%). The stock price is struggling to keep up with Wal-Mart's peers on the Dow Jones Industrial Average (^DJI -0.01%) over the last decade, even if you reinvested every dividend check along the way:

But you can't blame Wal-Mart's business for any of this market lag. Over this period, the store chain has doubled revenue while nearly tripling cash flow and earnings. Keep in mind that the Waltons have been battling the law of large numbers throughout this decade. It's not easy to double a $230 billion top line, you know. Investors should expect more than a 56% total return for this fantastic performance.

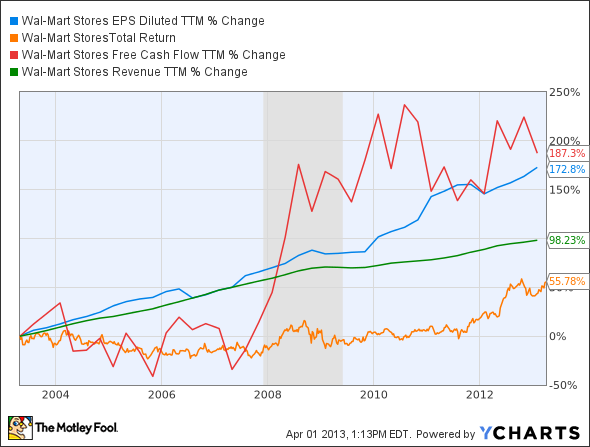

WMT EPS Diluted TTM data by YCharts.

The master of low costs and high efficiency thrives in challenging markets, as you can see in the cash flow spike during the 2008 recession. Free cash flow keeps growing at a double-digit clip every year, so you can't even claim that Wal-Mart shares should be cheap due to dying growth.

WMT P/E Ratio TTM data by YCharts.

All things considered, Wal-Mart shares look spring-loaded at current prices.