Two months ago, I wondered whether Express (EXPR) and Buckle (BKE -1.84%) deserved to be trading as cheaply as they were.

On the one hand, shares of Buckle were trading at only 13.6 times last year's earnings and just 12.7 times next year's estimates, despite the fact that it boasted plenty of cash with no debt, had turned in solid quarterly results a few weeks prior, and was continuing to open new stores at a steady pace while also boosting gross margin 60 basis points year over year to 48%.

Express, on the other hand, had worried investors by issuing cautious 2013 guidance following lower-than-expected foot traffic in February. However, its resulting 10% plunge that day seemed like a bit of an overreaction to me, especially considering that the company's balance sheet seemed solid, e-commerce sales growth remained healthy, and Express was only beginning to increase its focus on expanding internationally. Even so, shares of Express were trading hands at just 11 times last year's earnings and a mouthwatering 10.2 times next year's estimates.

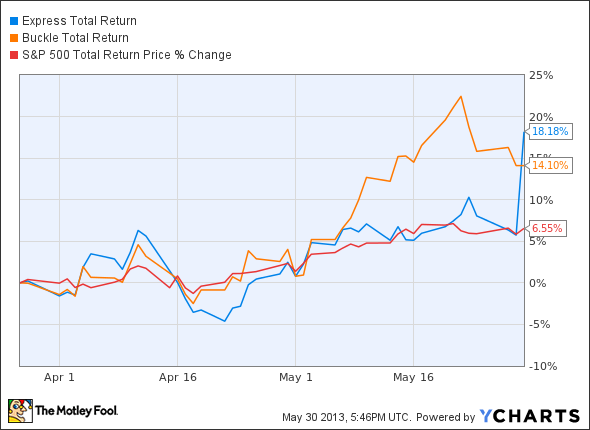

Since that article was published, Buckle has managed to outpace the S&P 500's total return by more than 7%. Meanwhile, until yesterday, shares of Express had simply kept pace with the index's respectable return. That was, at least, until Express popped 13% after the company reported earnings this morning:

EXPR Total Return Price data by YCharts.

So why all the optimism for Express today?

Sure enough, it turns out its previous guidance was indeed cautious, and the company managed to deliver strong results at the high end of its expected numbers.

More specifically, first-quarter net sales grew a modest 3% year over year to $508 million, beating analysts' expectations of $498 million and helped by steady comparable-store sales growth of 4%. Even better, Express' year-over-year e-commerce sales growth accelerated from 28% during last year's first quarter to 48% this quarter to $70.7 million.

On a more worrisome note, gross margin declined to 33.6% from 38.1% in the year-ago period, hurt by increased promotional activity and higher buying and occupancy expenses. Still, investors didn't seem to mind as those numbers remained in line with the company's expectations. What's more, Express managed to reduce selling, general, and administrative expenses this quarter 1.4% to $112.6 million.

In addition, while net income fell to $32.4 million, or $0.38 per diluted share, from net income last year of $42.1 million, or $0.47 per diluted share, that actually beat analysts' estimates, which called for net earnings of $0.36 per share.

Better yet, cash and equivalents rose more than 35% from this time last year to $244.2 million, while debt was relatively unchanged at just under $200 million.

Finally, management raised both its second-quarter guidance to a range from $0.17 to $0.21 per share and full-year 2013 guidance in a range from $1.48 to $1.58 per share. Going into the report, analysts expected the company to project second-quarter earnings of $0.14 per share and full-year earnings of $1.52 per share.

Foolish final thoughts

Even after today's pop, however, it's worth noting that shares of Express still trade at just 13.1 times trailing earnings and 12.2 times next year's estimates. I think the stock has plenty of room to run as the company executes its long-term plans.

In the end, Express serves as a great reminder that the stock market isn't always efficient, and knee-jerk reactions to "bad" news can provide fantastic opportunities for investors to buy stocks of otherwise solid businesses.