New technology, such as hydraulic fracturing and horizontal drilling, has created a natural gas boom and seen prices of domestic gas fall by as much as 83% in just five years (from $12.60/MBtu to $1.95/MBtu).

Prices have recently recovered to around $6/MBtu but still trade for two to three times less than in Europe or Japan ($10.88 and $15.7 respectively). This large spread creates an arbitrage opportunity that energy companies are eager to exploit by exporting liquefied natural gas (LNG). In its liquid state, gas takes up 600 times less volume but must be cooled to -260 F.

Export facilities that can liquefy, store, and load specialized LNG tankers are immensely expensive to build, and regulatory approval can take years. This means that those companies that already have approval and financing to build such facilities have a large moat to defend their margins. In this article I want to focus on four investments that offer investors an opportunity to cash in on the coming LNG export boom.

Cheniere Energy Partners (CQP 0.54%) is in the process of converting the Sabine Pass import facility in Cameron Parish, LA. The conversion will cost $7.8 billion and consist of four trains with a potential expansion to six.

Each train will be capable of exporting 231 trillion btu per year (Tbtu/y). The first four trains are fully contracted out for 20 years and expected to bring in $2.9 billion annually in fixed revenue. To put into perspective how much this will move the needle for Cheniere -- its 2013 revenues were $268 million.

Trains five and six (regulatory approval pending) should come online in 2018 and 2019. All six trains would provide $3.9 billion in annual revenue, which is a 1,340% increase over current levels.

Please note that there is risk involved with this partnership. The current distribution of 5.6% is entirely funded by debt as the partnership is currently not profitable.

In addition, LNG exports won't begin until mid-2015 which is assuming construction is completed as scheduled. An investment in Cheniere Energy Partners should be considered a high-probability speculative play; one that pays handsomely to wait for a long-term thesis to play out.

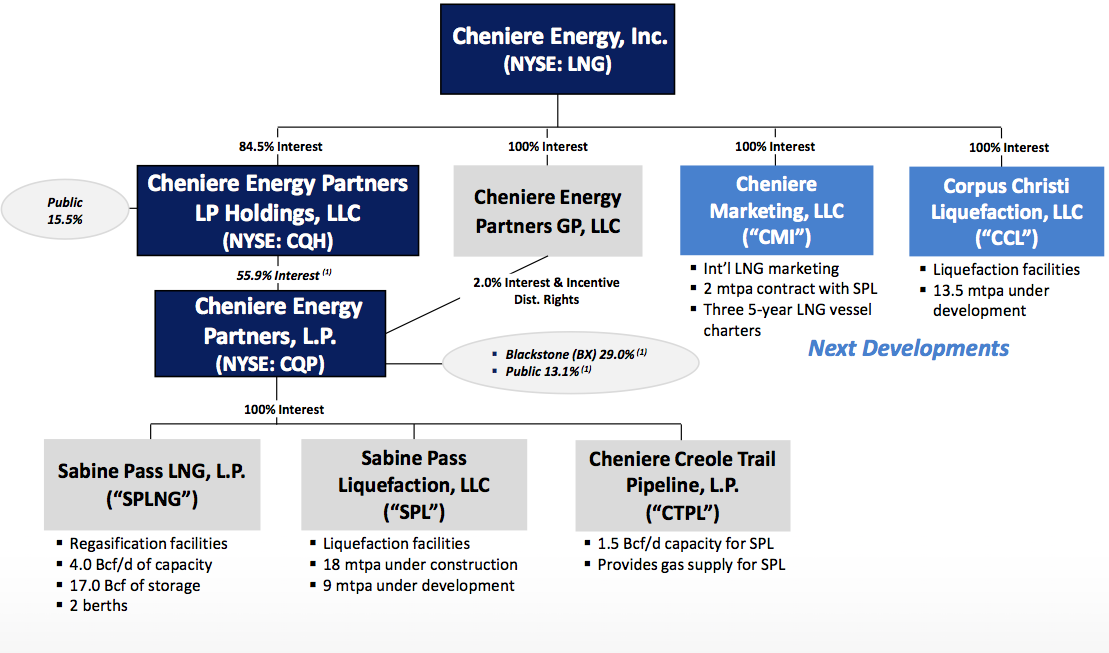

Cheniere Energy Inc (LNG 1.23%) is the parent company of Cheniere Energy Partners and there are several reasons that investors may want to consider owning both.

Source: Cheniere

The first reason is that Cheniere Energy Inc indirectly owns 48% of Cheniere Energy Partners as well as its general partner. This means that it collects distributions and incentive distribution rights (IDRs). IDRs mean that above a certain distribution the general partner receives 50% of all additional income. This would create a massive boost to the parent company's profit.

The second major reason to consider this investment is the Corpus Christi LNG terminal the company is building in Texas. This three-train facility will be capable of exporting 57% as much LNG as Sabine Pass (2.1 Bcf/d versus 3.86 Bcf/d including expansion). This facility is still undergoing regulatory approval and would cost $9.7 billion to construct. The first LNG exports would begin in 2018.

Finally, Cheniere Energy Inc is the owner of Cheniere Marketing (CMI), which has the rights to 45% of Sabine Pass's export capacity for trains one through four. The first 35% of this capacity CMI will pay Cheniere Energy Partners $3/Mbtu of gas. The remainder of its capacity it will split profits with Cheniere Energy Partners 80/20.

The only downside to owning Cheniere Energy Inc versus its limited partner is the lack of a distribution. The Corpus Christi facility is still four years away from exports beginning, so investors are asked to wait without the benefit of a high yield. This investment thesis is based purely on capital gains.

Sempra Energy (SRE -0.08%) is a large utility that yields 2.7% and who owns a 50.2% stake in Cameron LNG Holdings. This subsidiary is building a terminal in Hackberry, LA capable of exporting 1.7 Bcf/d of LNG. The project will be complete in 2018 and will cost Sempra $4.5 billion-$5 billion.

Sempra is estimating that it will receive $300 million-$400 million in added annual earnings during the first decade of operation. Based on the company's $1.09 billion in profits in 2013 this represents a 30%-40% increase in earnings and should help the company accelerate its dividend growth rate from its five-year average of 13.4%.

Dominion Resources (D -0.51%) is a diversified utility that is investing $3.4 billion-$3.8 billion in an LNG export terminal at Cove Point, MD. Production is scheduled to last from 2014-2018. When complete the terminal will be able to export 1.8 Bcf/d and store 14.6 Bcf of natural gas.

The export capacity of 270 Tbtu/y means that Cove Point will be able to export $1.6 billion worth of natural gas annually (at current prices). With 2013 net income of $1.7 billion, this facility should provide enough of an earnings boost to accelerate the company's dividend growth rate from its five-year average of 7.6%. With a yield of 3.4% and dividend growth rate of 8+%, long-term investors will profit handsomely.

Bottom line

The coming LNG export boom is going to make certain companies fabulously rich. Patient long-term investors can cash in as well. The above companies (and partnership) offer yield, potential for substantial distribution/dividend growth, and capital appreciation.