U.S. refiners have had a tough year, and Calumet Specialty Products Partners (CLMT 0.58%) is no different. The specialty refiner MLP plunged 37.5% from its peak in early 2013 to recent lows in the first quarter of 2014 and, despite a recent 20% recovery, the partnership is still 25% off its highs.

Major industry headwinds

The main reason for this weakness has been the compression of the WTI/Brent spread, which is the difference between West Texas Intermediate crude and Brent crude, the global benchmark. Refined goods are priced based on Brent oil prices, and America's recent shale oil boom has, until recently, resulted in a glut of WTI oil that's suppressed the price of refiners' main input cost and inflated margins to record levels.

Brent WTI Spread data by YCharts

The main cause of the compressed WTI/Brent spread has been new pipelines coming online in Cushing Oklahoma's oil terminal (where WTI is priced); however, additional new headwinds have recently arisen that threaten to compress the spread below the $9/barrel-$11/barrel that the Energy Information Administration (EIA) recently projected through 2015.

This added risk factor is the U.S. government's recent decision to allow two companies to export ultra-light sweet crude oil (in the form of minimally processed condensates), which could further decrease the difference between WTI and Brent oil prices.

This is because 27% of Eagle Ford shale production is condensate, and analysts believe that exports could reach 1.7 million barrels/day by 2018. That could result in permanently reduced profit margins for refiners.

In addition to this recent decision to relax the ban on crude oil exports, a glut of global refining supply is also hurting U.S. refining margins, according to Credit Suisse analysts Edward Westlake and Bryan Baritot.

Calumet's terrible quarter

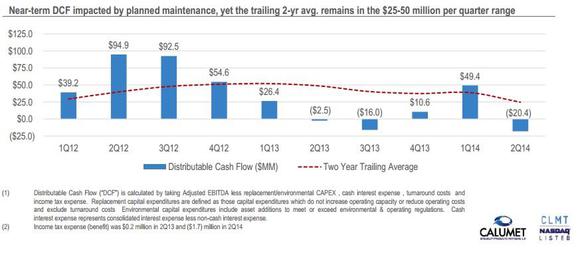

On August 6, Calumet reported a 43% decline in adjusted EBITDA (earnings before interest, taxes, depreciation, and amortization), and substantial negative distributable cash flow (DCF) -- which is used to pay the partnership's 8.7% yield.

Source: Calumet Specialty Products Partners Q2 Earnings Presentation

Given that Calumet's quarterly payout is $52.6 million, this means that Calumet hasn't covered its distribution for seven consecutive quarters and should have investors concerned about the long-term sustainability of the distribution.

Why Calumet's distribution might be safer than you'd think

Management pointed to two main reasons for the terrible results this quarter -- compressed specialty product margins and planned 30-day maintenance at its Shreveport refinery.

However, Calumet continues to believe the distribution is not only safe, but likely to grow in the long term, with management guiding for a long-term coverage ratio of 1.6x. Calumet has a two-pronged approach to achieving this long-term guidance: aggressive organic expansion and accretive acquisitions.

Growing itself out of a tough spot

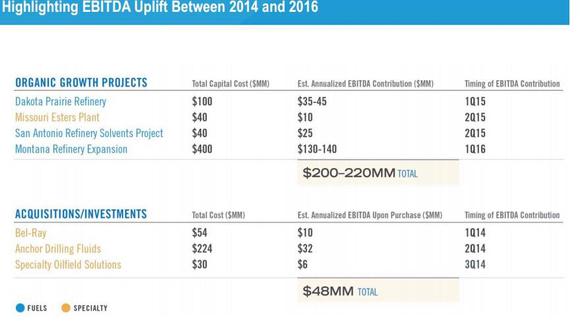

Source: Calumet Specialty Products Partners August 2014 Investor Presentation

As seen above, Calumet has plans to invest $580 million into four major growth projects, including the first new refinery built in the U.S. since 1976.

The summation of Calumet's activities will be an estimated $248 million-$268 million increase in EBITDA by 2016, which represents a 121% increase compared to the last 12 months.

Plenty of liquidity

Given Calumet's ambitious growth plans, one might wonder whether the partnership has the necessary cash to execute on its plans while continuing to pay its generous distributions. Luckily Calumet has been very successful at raising funds, having expanded its liquidity by 20% since the beginning of 2014. Part of this was the partnership's ability to increase its revolving credit by $150 million to $1 billion. It also has $300 million in equity that it's been authorized to sell "at the market."

This means that should Calumet management deem it necessary (and accretive to existing unit holders), it can sell additional units, a little at a time, at advantageous prices. This prevents the kind of sharp drop associated with large secondary equity offerings.

Thus, Calumet has a total of $1 billion available to achieve its growth objectives and from which it can pay out its distributions, until its growth projects come online and make the distribution self-sustaining in the long run. In case investors are concerned at the prospect of 14% dilution, you can rest easy knowing that 100% of Calumet's general partner and 26% of its units are owned by insiders and members of the partnership's founding families. Such high insider ownership goes a long way to aligning your interests with those of management.

Diversification to protect against the new normal of lower margin refining

Another cause for long-term optimism for Calumet investors is the partnership's diversification into the fast growing oil and gas services industry. Specifically its acquisition of Anchor Drilling, which provides fracking fluids to 250 companies in 13 states, and Specialty Oil Field Solutions gives it prime exposure to the Eagle Ford, Marcellus, and Utica shales -- three of the fastest growing sources of domestic oil and gas production in the country.

Foolish takeaway

Despite quarterly earnings that at first appear horrendous, Calumet Specialty Products Partners' distribution is in no immediate danger, and its long-term prospects remain bright. The partnership's diversification into the oil and gas services business grants Calumet investors exposure to America's booming shale oil and gas industry and should help grow the distribution in years to come.