Falling oil prices have taken a bite out of companies that service the oil industry, with the Dow Jones U.S. Oil Equipment & Services index falling 30% over the last six months. One big headline grabber recently was the drill rig space, where Seadrill Ltd (SDRL) announced a complete dividend suspension because "the near term offshore market is becoming increasingly challenging." Not all drillers, however, are in the same boat, and long-term industry survivor Helmerich & Payne (HP 1.92%), which has increased its dividend for 40 years, is looking like a bargain right now.

Offshore versus onshore

To be fair, Seadrill and Helmerich operate in two difference sub-sectors: offshore and onshore, respectively. There are different dynamics and technologies involved in each. For example, Seadrill's specialty is renting out highly advanced, and expensive, rigs that can survive in incredibly difficult environments like the arctic waters off of Russia. Helmerich & Payne generally doesn't have to contend with such extreme conditions, and its rigs are smaller and much less costly.

For example, Seadrill has 16 rigs under construction worth around $6 billion. It took delivery of three new rigs in the third quarter. Helmerich, meanwhile, is at a run rate of building four new rigs per month. It plans to keep building at four rigs per month through the end of fiscal year 2015 next October, with 46 of the 48 potential builds already under multi-year contracts. Essentially, it looks like customers still want Helmerich's rigs. Meanwhile, Seadrill is actively working to delay taking delivery on some rigs because falling oil prices are changing the dynamics in the offshore market, with CEO Per Wullf noting during the third quarter conference call that it could cancel at least one new build if it can't get a contract for it.

Source: ENERGY.GOV, via Wikimedia Commons.

Moreover, roughly 90% of Helmerich's rigs are located in the United States. Thus, it doesn't have to contend with geopolitical issues. Seadrill's business is more global. Its offshore Russian exploits, for example, have become increasingly uncertain since Western sanctions have grown to be more stringent throughout the year.

One big similarity between the onshore and offshore market, however, is the impact of the price of oil on drilling demand. And that's a big one, with Reuters reporting that new drilling permits in the onshore U.S. space fell 15% in October. Slower drilling could mean fewer contracts for a company like Helmerich, which is why its shares have fallen along with oil prices, despite its strong and well-contracted backlog. And Seadrill was so concerned about the offshore outlook because of lower oil prices that it eliminated its dividend. Lower oil prices should have conscientious investors concerned about the future for rig owners.

What's the risk?

There are other factors at play here, however. For example, Seadrill's capital structure is comprised of around 50% debt. On the other hand, debt makes up less than 1% of Helmerich's capital structure. This gives Helmerich a lot more flexibility. In fact, during Seadrill's third quarter conference call, CFO Rune Magnus Lundetrae noted that, "Seadrill utilizes the capital market to bring forward future earnings and pay dividends, amortize debt and fund capital expenditure for our growth."

I added the emphasis on pay dividends because he's basically saying that Seadrill needs to issue debt to pay its dividend. How does that play out? Through the first nine months of the year (before the dividend was eliminated), operating activities provided cash of roughly $1.3 billion. It paid dividends of just over $1.4 billion. To be fair, Seadrill has a lot of costly rigs being built, but the board's decision in light of weakening oil prices looks like a good one since renting out drill ships wasn't covering the dividend and a changing market environment could make the shortfall even worse.

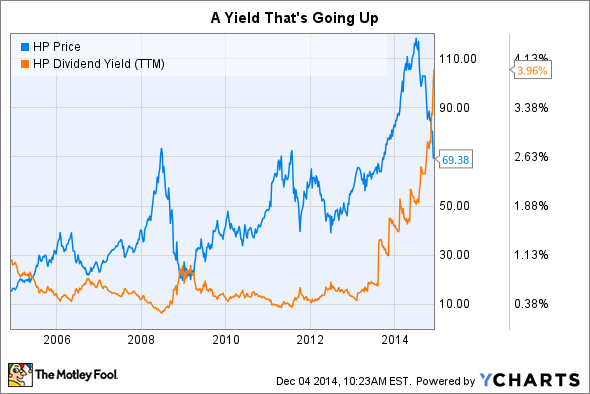

Helmerich & Payne's cash flow from operating activities in fiscal 2014, meanwhile, was roughly $1.1 billion, and it paid dividends to the tune of $265 million. The company has a lot more leeway than its offshore cousin. Add to this the fact that the company's June dividend hike was its 40th consecutive annual increase, and there's clearly a board-level commitment for Helmerich to protect its dividend. And that's an opportunity for income investors since the shares currently yield around 4% -- relatively high for this company.

Looking for a bargain

Oil is a commodity that has a history of wild price swings. The current downdraft took out Seadrill's dividend as it braces to weather what will be an unpredictable oil price storm. Helmerich & Payne, meanwhile, is getting buffeted by similar headwinds, only it's in a better financial position to handle the gale. And 40 years of dividend hikes suggests it knows how to deal with the oil industry's ups and downs. If you're looking for an oil industry bargain, don't get spooked by Seadrill's dividend elimination; Helmerich & Payne should still be on your short list.