Now that Halliburton (HAL 1.11%) is buying Baker Hughes (BHI) in order to make a run at Schlumberger (SLB -2.14%), many investors are probably wondering which one of these two oil-field services companies is the better buy today. So we asked two of our energy contributors to lay out why one should be higher on your buy list than the other. Here's what they had to say.

Matt DiLallo: The case for Halliburton

There is a clear and compelling case to be made that Halliburton is a better stock to buy now, and that it is the better company to own for the long term. I'll start with value. As the following chart shows, Schlumberger has historically traded at a premium valuation over Halliburton:

There is a clear and compelling case to be made that Halliburton is a better stock to buy now, and that it is the better company to own for the long term. I'll start with value. As the following chart shows, Schlumberger has historically traded at a premium valuation over Halliburton:

HAL P/E Ratio (TTM) data by YCharts.

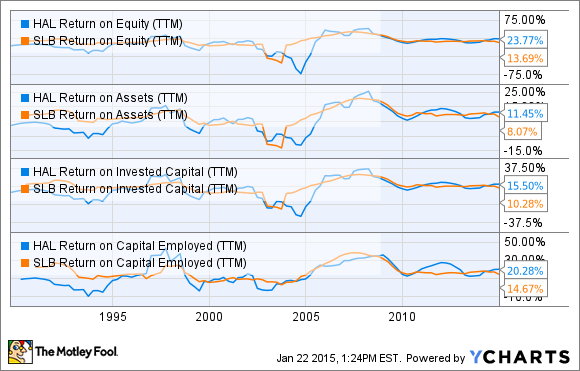

Because of Schlumberger's larger size and scale, investors have traditionally paid a premium to own its stock. This irks Halliburton's senior management because their company's operational returns have been better than its larger peer, particularly over the past few years, as we see in this next slide.

HAL Return on Equity (TTM) data by YCharts.

Halliburton, thus, believes it deserves the premium valuation from investors. But it realizes that won't happen until it can rival Schlumberger in size. This is a primary driver behind the company's desire to merge with Baker Hughes: It feels the combination will provide it with synergies and new opportunities, as well as the scale it needs to demand a higher valuation multiple.

It's my belief that once the deal closes Halliburton will indeed begin to close its valuation gap with Schlumberger. Which is why I think its stock has the potential to outperform Schlumberger over the long term -- investors are not only getting a better value now, but also a company that should enjoy a much higher valuation in the future once the energy market settles down a bit. So if I had to choose between the two, I believe Halliburton is unquestionably the better buy now.

Tyler Crowe: The case for Schlumberger

I'm not afraid to admit that Halliburton's stock might perform a little better than Schlumberger's over the next year or so. Over that sort of time period, though, it's too much of a crap shoot to pick a clear winner. If looking to buy one of these companies and hold on to it for a long time, on the other hand, the following chart makes it hard to argue Halliburton is a better investment than Schlumberger.

HAL Total Return Price data by YCharts.

BOOM!

It isn't sheer coincidence that Schlumberger's stock has outperformed Halliburton's by close to four times over this decades-long time horizon. It comes down to a few key things.

- Schlumberger runs a leaner operation. I'm going to act like a sports journalist and accuse Halliburton of juicing -- on debt, that is. Those higher return numbers from Halliburton (as seen in Matt's chart above) are in part because it has been running a higher debt leverage ratio, and it takes a higher level of working capital than Schlumberger for the company to generate earnings. This can help a company look better in the good times like these past few years, but it can also sink a company when the market goes south.

- Schlumberger's revenue is tied to longer-term, higher-margin projects, such as deepwater operations and international business, while Halliburton is much stronger in North America and in onshore shale drilling. While both of these sources of oil and gas are high cost and will likely decline, it takes far more time to wind down a deepwater project than to close a shale well, meaning the impacts of the production decline will be felt faster by Halliburton. Throw in Schlumberger's more technology-driven, less-commoditized services, and you get EBITDA margins 5 percentage points higher.

HAL Return on Equity (TTM) data by YCharts.

It's far too brazen to say Schlumberger's stock will continue to crush Halliburton's as it has over the past several decades, but that 2.4% dividend yield (compared to Halliburton's 1.8% and Baker Hughes' 1.2%) certainly has helped. Bottom line, Schlumberger has had a higher valuation for a reason: it's just the better company.