Do These 20 Things Before Applying for a Mortgage

Do These 20 Things Before Applying for a Mortgage

Scratching that new home itch

You've got the itch to buy a home. Maybe it will be your first. Maybe it's one you saw a "for sale" sign in front of and instantly fell in love with. Maybe you've been saving for this big purchase for many years. No matter the circumstance, it's a big deal -- because the homes we buy are typically the biggest purchases we'll ever make.

Here are 20 things to know about and ways to prepare before applying for a mortgage.

1. Assess your financial big picture

First things first. Take a moment to assess your big picture. Are you burdened with a lot of debt? If so, is it wise or even possible to add a lot more? Do you have ample cash -- for the down payment and to spend on home-buying expenses such as inspections? What about the home you live in now -- do you own it, and if so, will you be selling it?

Don't rush into buying a home and taking on a mortgage until you're sure that you have all your ducks in a row. The following additional items for your pre-mortgage to-do list can help straighten those ducks out.

2. Think twice before changing jobs

If you've been thinking of changing jobs, know that it's not a great thing to do right before you buy a home. That's because mortgage lenders are going to be handing over a big gob of money for your purchase, and they want to feel comfortable that you're a good risk, that you'll be able to make the monthly repayments on your debt.

One thing they like to see is that you're well employed, with ample income to cover your mortgage payments (and all of life's other obligations) and some years at your job, which suggests stability. Lenders like stability.

3. Think twice before taking out other loans

Just as lenders like to see stable employment, they also like to see that you don't already have a significant debt burden, which you're looking to add to, significantly. Thus, if you're planning to buy a home with a mortgage and you also want to take out a car loan or some other loans -- or you plan to charge a major purchase onto a credit card and not pay it off pronto -- it would be smart to get the mortgage first. (Of course, it's always best to pay off all credit card bills in full and on time, lest costly debt start accumulating.)

4. Check your credit score

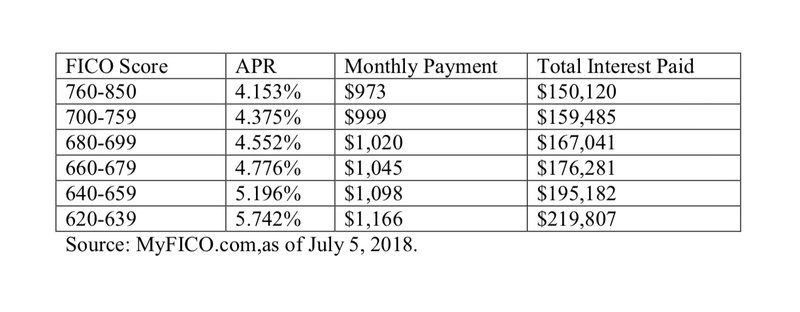

It's also smart, before getting a mortgage or even shopping for one, to check your credit score. That's because those with the highest scores get offered the lowest interest rates. Here, for example, are some recent sample interest rates for various score ranges for someone borrowing $200,000 via a 30-year fixed-rate mortgage:

The difference between the highest and lowest interest-rate range in the table above is $193 per month (which is $2,316 per year) in mortgage payments -- and nearly $70,000 in total interest paid! You may be able to find your credit score printed on your credit card's monthly statements. If not, you can buy access to your score -- or get it for free. Consider going right to the source, too. At myFICO.com, you can get a one-time copy of your FICO credit score and a credit report from one of the three credit reporting agencies for $20 or scores and reports from all three agencies for about $60.

5. Understand the components of your credit score

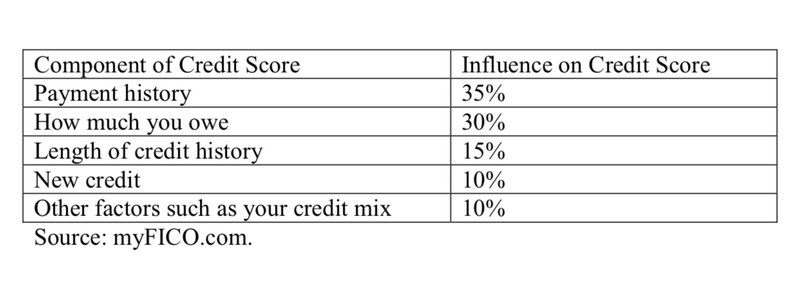

If your credit score has room for improvement, know that you can improve your credit score. Knowing the components of a typical FICO credit score (which is the score most widely used by mortgage lenders) and the influence that each has on the score can help you see how to boost your score:

Clearly, some components are far more influential and important than others.

6. Increase your credit score -- by paying bills on time

The most important factor that contributes to your credit score is your payment history -- how good you are at making your payments in a timely manner. (It makes up about 35% of your score.) If paying bills on time hasn't been a core strength of yours, that's likely reflected in your score, and you can beef up your score by changing your ways. Start paying all bills on time, and pay any late bills pronto -- because having a bill that's overdue by two months counts against you more than a bill that's overdue by one month.

Changing your ways won't cause your score to spike immediately, but every on-time payment will help offset a late one. Better still, the worse your score is, the faster you can see improvements in it.

7. Increase your credit score -- by paying down debts

Remember that how much you owe is a factor with a 30% influence on your credit score -- thus, paying down debts can help boost the score. A good way to measure this is by calculating your "credit utilization" ratio, which reflects the percentage of the total of your credit card credit limits that you owe. For example, if you have three credit cards, with credit limits of $5,000, $3,000, and $10,000, that's a total of $18,000 that you could owe on them. If the actual credit card debt that you're carrying on your cards totals $12,000, your credit utilization ratio is 0.67 or 67% -- the result of $12,000 divided by $18,000.

The lower the ratio, the happier your would-be lenders will be, as they aren't eager to let you borrow a hefty sum when you're already straining against your credit card limits. A high credit utilization ratio can suggest that you're not in great control of your finances. A good rule of thumb is to aim for a ratio of about 10% to 30%. (One trick to shrink your ratio is to ask for increases in your credit limits.)

While you're paying down your credit card debts, take care of any collections against you, too, as they will not be helpful to your credit score and lenders don't like to see outstanding collection accounts. You may be able to offer the collection company a portion of what you owe in order to have the account closed.

8. Protect your credit score -- by not closing accounts

The length of your credit history counts for about 15% of your credit score. You can make use of that information by not closing accounts -- especially old ones -- just before you apply for a mortgage. Lenders like to see that you have some active and long-lived credit accounts, and closing out an old account or two could ding your credit score, even though it doesn't reflect you managing your money poorly.

Note, too, that if you close out some credit card accounts, you'll lose some of your total credit limit, and can thereby cause your credit utilization ratio to increase. (Remember that the ratio, of total credit card debt to total credit limits, should be between about 10% and 30%, ideally.) Doing so can deliver another blow to your credit score.

9. Increase your credit score -- by correcting errors in your credit report

You should check not only your credit score, which is a single number, but also your credit report, which can be multiple pages of details on just about all the debt accounts you've had and your payment histories for each, among other things. It will show, for example, your various credit card accounts, car loans, and previous mortgages, and will note when payments were made late.

Each of the three major credit reporting agencies should have a credit report on you, and it's important to review them (ideally, all of them), looking for any errors. After all, false negative information can depress your credit score needlessly. You can get free copies of your credit reports once a year from each of the main credit reporting agencies at www.annualcreditreport.com -- and it's smart to do so, no matter what your score is. If you spot errors (such as payments incorrectly listed as having been made late or incorrect sums of debts, each agency has ways for you to go about getting them fixed.

10. Think about how big a down payment to make

Next, think about how much money you want to put down when you take on a mortgage to buy a home. It's tempting to aim to pay as little down as possible, but if you have done so and real estate values suddenly head south, it could wipe out whatever equity you've built in your home and could leave you "underwater" -- owing more on your home loan than the home is worth. That can complicate matters if you need to sell the home.

Another concern is this: If you make a down payment of less than 20%, you'll probably be required to take on an extra loan in the form of private mortgage insurance (PMI), which will increase your monthly payment. A low down payment might also result in a higher interest rate, too. On the plus side, though, if you start with less than 20%, once your home equity passes 20%, you should be able to have your lender cancel the PMI.

So should you aim really high and try to make a down payment of, say, 30% or more? Well, you could -- and doing so will shrink how much you have to borrow and thereby make your monthly payments smaller. That will put less pressure on you from month to month. But it will also mean that you have parked even more money into an asset that isn't likely to increase in value as quickly as, say, the stock market.

11. Look into any low-down-payment programs of interest

While there are good reasons to aim for a down payment of 20%, there are options for those who don't have that much money at the ready. Indeed, you may actually be able to get a mortgage paying little to nothing down. For example, VA loans or USDA Rural Development loans (which apply to lots of not-so-rural areas near cities) offer mortgages with $0 down payments. Conventional mortgages backed by Fannie Mae or Freddie Mac may allow you down payments of as little as 3% to 5%, while Federal Housing Administration (FHA) loans are available with only 3.5% down. These can mean the difference between buying a home and not being able to, but understand that if the home's value falls, you can end up owing more than it's worth, with no equity.

12. Determine how much house you can afford

A key question to answer for yourself is how much home you can really afford to buy. If you don't have a definite answer, you can end up borrowing more than you should for a home you really shouldn't buy -- one that leaves you with little wiggle room, financially, if you encounter unexpected expenses or if your household income drops.

One rule of thumb is to spend no more than 25% to 30% of your gross monthly income on housing (including property taxes and insurance), but it can be smarter to take the time to figure out exactly what you can afford. For many people, it's smarter and safer to spend no more than 20% on housing. Buying less home than you can afford will give you a margin of safety and help you be able to meet other financial goals, such as saving for retirement or college. Remember that some lenders may encourage you to borrow more -- resist that temptation if you know that the mortgage payments will be onerous or risky for you.

13. Decide whether a fixed-rate or adjustable-rate mortgage is best for you

Remember that when it comes to mortgages, there are lots of different kinds to choose between. For example, you'll need to decide whether you want a fixed-rate mortgage or an adjustable-rate mortgage (ARM). If you're not planning to be in the home long, an ARM can make a lot of sense in today's low-interest-rate environment, as it will lock in low rates for a few years. ARMs typically give you a few years at an interest rate that's more attractive than those for fixed-rate loans, but then the rate starts being adjusted regularly, to reflect prevailing rates. So with a 5-1 ARM, for example, the initial rate will hold for five years before being adjusted annually. If interest rates are rising, your mortgage rate will rise, too.

If you think you'll be in the home for many years or decades, it can be better to lock in a fixed interest rate for the entire long life of the loan -- especially these days, as interest rates are still quite low, historically speaking, and they seem to be on the rise.

14. Decide whether a 15-year or 30-year mortgage is best for you

You should also decide whether you want a 15-year loan or a 30-year loan. (There are other terms available, too, but these are the most common terms.) You'll often be offered a lower rate for a shorter-term loan, which can make a 15-year loan seem well worth it, as you'll pay off your home faster and you'll pay far less in interest, too. But 15-year loans have significantly higher monthly payments. If you think that will stretch you too thin, consider buying a less costly home -- or opting for the 30-year loan.

Here's a clever strategy to consider: Get a 30-year loan that lets you make extra payments on principal without any penalties. Then you can send in bigger payments each month -- ones that are like what you'd be paying with a 15-year loan -- and you'll pay off the loan sooner. Plus, if life throws you a curve ball, you can always revert to paying just the lower minimum amount. You'll essentially be making the larger monthly payment optional, not required.

Shorter-term loans might be better for those who are closer to retirement and who don't want to enter retirement with a decade more of mortgage payments to make. Longer-term loans are good for those who want their monthly payments to be low and who don't mind that they'll be paying much more in interest.

15. Gather documents

Before you start the process of applying for a mortgage, you would do well to start collecting some documents that you'll have to provide. Here are some that are commonly required:

- Recent

pay check stubs

- Recent

bank statements

- Recent

brokerage account statements

- Your

tax return from the last year(s)

- Your

most recent W2 form(s) from your employer(s)

- Proof

of timely rent payments if you're a renter

- The

home sale agreement

- An

accounting of your income from all sources

- A

list of all your assets -- such as current balances in various accounts

- A

list of all your debts

- Your

employment history

- Your

divorce decree, if you're divorced

- Bankruptcy

discharge papers, if you've declared bankruptcy

Note that if you're self-employed, you may have to jump through additional hoops and provide more information, such as profit-and-loss statements. Those borrowing particularly large sums (via "jumbo" loans) often have to provide extra information, too. If you're buying the home with a spouse or partner, the information above will be needed for both of you.

16. Comparison shop for the best deals

Once you're ready to get a mortgage, don't just apply for one with the bank you use the most or the bank you used for your last mortgage. Instead, shop around. Lenders use different formulas and criteria when evaluating you as a would-be-borrower, and each is likely to offer you a somewhat different interest rate.

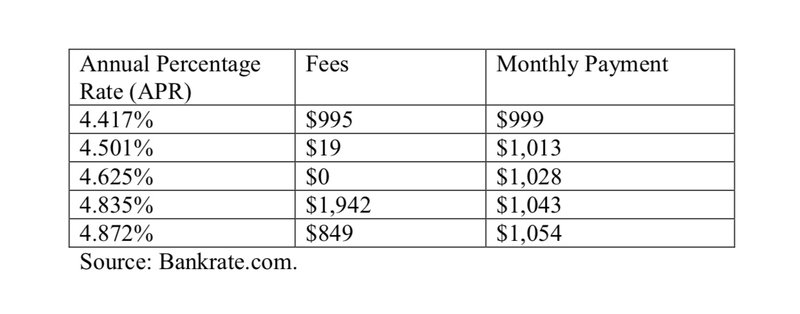

You can find some rate quotes online, at sites such as bankrate.com. Bankrate.com recently offered the following rates (among many) for someone in Rhode Island with a credit score of 740 buying a $250,000 house and paying 20%, or $50,000, down for a 30-year fixed-rate mortgage:

ALSO READ: Interest Rates Are on the Rise. Here's How to Prepare

17. Get pre-approved for your mortgage

Once you're ready to make offers on homes and you know what loan you want and from which lender, it's a good idea to get pre-approved for the loan before you go shopping. Why? Well, there are several reasons. For starters, the process of working with a loan officer can help you pin down just how much home you can afford to buy. Second, being preapproved will make you a more credible buyer, should you end up bidding against any other buyers for a home.

Pre-approval means that the lender will have looked at your credit score, your employment, your financial health, and perhaps some tax returns -- and found you credit-worthy. Don't confuse being pre-approved with being pre-qualified. Being pre-qualified means a lender has taken a less close look at you and your finances and has determined that you're qualified to borrow money from it. Being pre-approved is a stronger endorsement and means you're further along in the financing process.

18. Ensure that your mortgage has no prepayment penalty

This may seem like a minor detail, but it's not. Be sure that you will not face any penalty if you pay more than you have to when sending in your monthly mortgage payments -- either occasionally or often. Paying more is a great way to lop years off your loan and letting you turn a 30-year mortgage into, say, a 19-year one or a 24-year one.

If your mortgage rate is 6%, every extra sum you send in is essentially earning a guaranteed 6% return -- because you'll be avoiding having to pay 6% on it. These extra payments will help your balance owed to drop faster, because in the early years of a loan, much of your required monthly payment goes toward interest and not toward reducing your balance.

While you're at it, be sure to read all the rules related to the mortgage you're signing up for. It's a big contract you're entering into, so you don't want any unpleasant surprises down the road.

19. Be sure that your home purchase is a smart one

It's also smart to be sure that the home you're buying is a smart purchase. For example, it's not ideal to buy the fanciest house in the neighborhood or on a street, as the houses around it will be valued lower and might depress your own home's value. Think about how resellable a home will be, whenever you want to sell. You might buy it knowing that it's weird and that not many people would like it as you do, but that can work against you whenever you do want to sell. Think, too, about how much work the home will require. How much will it cost? How will you pay for it? Fixer-uppers can be bargains -- but they can also end up costing you much more than you expected.

20. Consider delaying buying a home

Finally, once you've considered all the guidelines above and have taken an honest look at your financial situation, think hard about whether this is really a good time for you to buy. It certainly may be. But if you don't yet have much of a down payment ready, or if you think that interest rates will be falling, or if you're not sure you'll be staying in your current region for much longer, you may want to put off buying a home. Think, too, about your credit score, as it might be smart to delay buying a home for a year or so, while you work to increase it in order to secure a better interest rate.

There's not as much downside to renting, after all, as you might think. Rent amounts tend to be lower than mortgage payments, and you could invest the difference each month, thereby building wealth in stocks instead of through home equity. Renters don't have to face property taxes or the cost of maintenance and repairs, either.

Buying a home can be very rewarding -- just be sure to approach the process with your eyes open and with lots of information. The extra time spent doing your research and planning ahead can end up saving you tens or hundreds of thousands of dollars.

The Motley Fool has a disclosure policy.

HOW THE MOTLEY FOOL CAN HELP YOU

-

Premium Investing Guidance

Market beating stocks from our award-winning service

-

The Daily Upside Newsletter

Investment news and high-quality insights delivered straight to your inbox

-

Get Started Investing

You can do it. Successful investing in just a few steps

-

Win at Retirement

Secrets and strategies for the post-work life you want.

-

Find a Broker

Find the right brokerage account for you.

-

Listen to our Podcasts

Hear our experts take on stocks, the market, and how to invest.

Premium Investing Services

Invest better with The Motley Fool. Get stock recommendations, portfolio guidance, and more from The Motley Fool's premium services.