One of the best-proven ways to profit from stock investing is to buy growth stocks. There's risk, of course, since growth stocks can be more volatile than bigger, more stable companies. This is especially true if you're not willing or able to buy and hold. But if you're able to take a long-term approach and buy and hold those growth stocks for multiple years, history has proven that growth stocks -- as a group -- tend to outperform the market.

In order to help you get started, we asked three real-world investors who also write for The Motley Fool to put forth their best "buy now" growth stock ideas, and they came up with high-growth home builder LGI Homes Inc (LGIH 0.87%), return-to-growth restaurant chain Chipotle Mexican Grill, Inc. (CMG -0.60%), and upstart immunotherapy developer Atara BioTherapeutics Inc (ATRA 1.20%).

Image source: Getty Images.

Not only are these growing companies with great long-term prospects, but three real-world investors also say they're worth buying right now. Read on to find out why.

Back in bargain territory

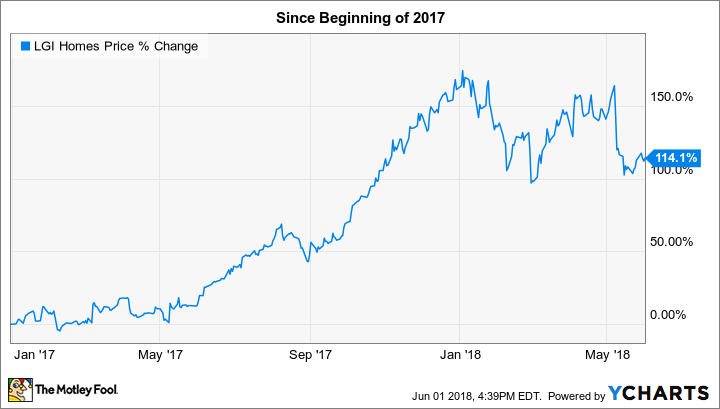

Jason Hall (LGI Homes): After reaching an all-time high at the start of the year, high-growth home builder LGI Homes has seen its stock price behave like a roller coaster. That is, it's moved both up and down, but mostly down. As of this writing, the share price is down 22% from the high and down 19% since announcing its first-quarter results about three weeks ago.

Here's the thing: LGI's beat-down share price isn't because it had a bad quarter. To the contrary, it was another sparkling period, with home closings and earnings up 64% and 132%, respectively. The home builder also increased the number of active communities by 14% and reaffirmed its guidance for the full year.

So why the sell-off? Fear of higher interest rates keeping millennials out of the housing market, primarily, along with a likely dash of "profit taking" from investors who've enjoyed the big run-up of its share price. Since the start of 2017, LGI Homes' stock price was up more than 150% at the peak, and it is still up 114% even after the recent sell-off.

And that sell-off has created a wonderful opportunity for investors. The stock trades for 11.6 times trailing-12-month earnings and between 8.8 and 10.3 times the company's own guidance for full-year 2018 earnings per share. That's a veritable bargain for a company delivering this kind of growth and with prospects to keep it up over the next decade.

The fast-casual chain that's getting past its quality issues

Chuck Saletta (Chipotle Mexican Grill): The market hates uncertainty and bad news, and it usually punishes companies that don't live up to its expectations. Shareholders of fast-casual food chain Chipotle Mexican Grill have certainly felt that pain as it has suffered through a series of food safety issues that knocked it off its rapid growth trajectory.

Chipotle Mexican Grill's shares are still well below the highs they set in 2015, but the company is certainly showing signs that its recovery is under way. For one key sign, it feels confident enough in its prospects that it actually has been raising prices -- something companies in crisis rarely are able to do. Those price hikes have helped the company increase same store sales and earnings, which showcases that its consumers are getting past the company's problems and are willing to pay for its food.

Additionally, rising prices, same store sales, and profits enable the company to fund more new store openings, which it is doing in 2018 and planning to continue throughout 2019. Adding new stores on top of same store sales growth should drive even more top-line and eventually bottom-line growth for the company.

Today, Chipotle Mexican Grill is operating smarter than it did before it faced those food safety problems, and its consumers have clearly shown a willingness to come back and pay a premium for its food. Despite those enhancements and other signs of its return to growth, its shares still trade at a discount to where they were before the crisis emerged. If its growth truly does continue to materialize, that discount to its past glory won't last. That makes it a growth stock worth considering to buy right now.

The trend is your friend

George Budwell (Atara BioTherapeutics): Shares of Atara BioTherapeutics, a leading off-the-shelf allogeneic T-cell immunotherapy company developing novel treatments for patients with cancer, have nearly quadrupled in value this year. Even so, the biotech's stock should only continue to trend upwards for the foreseeable future.

What's the backstory? Atara is racing to become the first company with a scalable adoptive cell therapy for cancer. As things stand now, the leaders in the field are limited by the extensive manufacturing processes involved in the current generation of cell-based cancer therapies.

So, despite their awe-inspiring levels of efficacy for some patients with various forms of hard-to-treat blood cancers, this first generation of adoptive cell therapies hasn't quite gotten off to the blistering commercial start their developers originally hoped for from the outset.

Atara's tab-cel (tabelecleucel) platform, however, is showing strong signs that it could solve this underlying problem, potentially unleashing the latent value of this multi-billion-dollar market.

Where do things stand now? Atara is presently in late-stage testing for tab-cel, with the therapy's top-line results, along with a possible regulatory filing in the EU, on track for the first half of 2019. If this timeline holds, there's little doubt that Atara will end up as a top buyout target next year.

There are multiple companies vying to become the leader in adoptive cell therapy. And several companies have shown a willingness to pay top dollar for well-differentiated platforms that can produce best-in-class or first-in-class products. As such, this top growth stock comes across as a great buy and hold right now.