You might have heard that a top analyst who covers the cannabis industry picked Aurora Cannabis (ACB -3.17%) as the best marijuana stock on the market right now. You also perhaps have noticed that Aurora's share price has soared more than 90% so far in 2019.

With the analyst's accolades and the powerhouse performance, you might be wondering if now is the time to buy Aurora Cannabis stock. The answer is... maybe. Here are five things you need to know first, though, before buying the hot marijuana stock.

Image source: Getty Images.

1. It's on track to have the highest capacity in the industry

Here's a key fact about the marijuana industry: A company can only sell what it can produce. Of course, that's true for pretty much any industry. But here's another fact about the marijuana industry that doesn't apply to most industries: Companies can sell everything they can produce. That's what happens when demand is greater than supply.

If you put these two facts together, it makes sense that the most successful companies in the marijuana industry will have the most capacity. The good news for Aurora Cannabis is that it's on track to have the highest capacity in the industry.

Aurora expects to have an annualized production run rate of 150,000 kilograms by the end of this month. But its funded annual capacity targeted for mid-2020 tops 500,000 kilograms. And that figure doesn't include the boost to capacity that Aurora's acquisition of ICC Labs will bring.

Check out the latest earnings call transcripts for the companies we cover.

2. It's No. 2 in the Canadian recreational pot market

The Canadian adult-use recreational marijuana market is still in its early days. We know already, though, that two companies have emerged as the clear leaders based on their latest quarterly updates.

Canopy Growth (CGC -0.54%) claims the highest market share in the Canadian recreational pot market. However, Aurora Cannabis isn't too far behind with a 20% market share in the quarter ending Dec. 31, 2018. There could be some jockeying in position down the road, but it seems likely that Aurora will stay near the top over the long run.

3. It's arguably the leader in international markets

This one's a close call. Aurora reported international sales of 2.9 million in Canadian dollars (around US$2.2 million) in the last quarter compared to Canopy Growth's total international sales of CA$2.7 million (around US$2 million). That's a tiny difference, especially considering how early it still is for global medical marijuana markets.

But Aurora recently began shipping cannabis oils to Germany, which will almost certainly spark its international sales growth. The company also is active in 24 countries spanning five continents. That's even more than Canopy Growth, which has operations in 16 countries.

The biggest drawback for Aurora from an international perspective is in the U.S. Aurora can't enter the U.S. marijuana market and retain its listing on major stock exchanges as long as marijuana remains illegal at the federal level. Canopy has already announced plans to jump into the U.S. hemp market, but Aurora hasn't done so yet.

4. It's angling for strategic partnership deals

Another area where Aurora is indisputably behind Canopy Growth is in strategic partnerships. Big alcoholic beverage maker Constellation Brands has poured over $4 billion into Canopy and owns a 38% stake in the company. So far for Aurora, there have only been rumors of potential deals with major companies outside of the cannabis industry.

That could soon change, though. Aurora recently brought billionaire investors Nelson Peltz on board as a strategic advisor. Peltz's role will be to help the company find partners in what he called "mature players in consumer and other market segments." If these efforts are successful, Aurora could have some significant catalysts ahead.

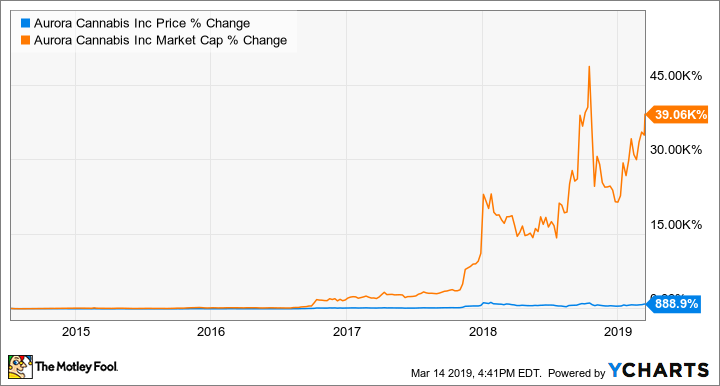

5. It's diluted the value of existing shares like crazy

You might think that I've painted too rosy of a picture for Aurora Cannabis thus far. Well, here's the thorn in the rose: Aurora has diluted the value of its existing shares like crazy by issuing new shares as part of bought-deal financing transactions. As the following chart shows, these transactions have taken a big toll on the stock's performance.

The growth in market cap reflects what Aurora's stock performance would have been if it were not for dilution. However, Aurora's executives would tell you that this dilution from issuing new shares was a necessary evil to expand rapidly in order to position the company for the long term.

This could continue to be an issue for investors, though. Although Aurora is tracking toward profitability, it could still have to raise additional capital for expansion through bought-deal financing in the future. Also, the company has nearly $500 million in convertible notes outstanding that could be converted into shares over the next few years, causing even more dilution.

One other thing to know

There's one other thing that investors considering buying Aurora Cannabis should know: how big the global marijuana market could be. Some point to a global market of $150 billion. This number comes from a United Nations estimate, but it includes illegal marijuana sales as well as legal sales.

Others highlight the potential for cannabis to disrupt several multibillion-dollar industries. Canopy Growth co-CEO Bruce Linton even said that cannabis could disrupt a combined global market of $500 billion, including the impact on alcoholic beverages, tobacco, and pharmaceuticals.

The truth is that some of what you hear is hype. However, the reality is that the global legal marijuana market will undoubtedly be much larger in the future. I think that a market size of more than $100 billion within the next 15 years is quite possible.

Aurora Cannabis' market cap currently stands around $9 billion. All the company has to do it capture a small share of the global market to have a lot of room to run.