Last year, marijuana investors still would have likely considered cannabis companies Aurora Cannabis (ACB -6.25%) and Canopy Growth (CGC -1.23%) to be the industry leaders in the Canadian pot market. But with both companies now struggling to stay out of the red and finding it difficult at times to grow their top lines, another cannabis producer, Aphria (APHA), has had an opportunity to establish itself.

Although Aphria was a big name in the cannabis industry a year ago, investors weren't considering it in the same breath as Aurora or Canopy Growth. A year ago, Aphria's market cap was about $1.6 billion, nowhere near Aurora's $8 billion valuation or Canopy Growth's astronomical market cap of over $10 billion. Since then, Aphria's market cap has declined somewhat, but at $1.3 billion it's now slightly more than Aurora's $1.1 billion. Meanwhile, Canopy Growth currently sits at a market cap of about $6.3 billion.

Let's take a look at why Aphria has become a relatively bigger name in the industry and why it's likely to continue rising in value in relation to its peers.

Aphria has normally been profitable, unlike many cannabis companies

When Aphria released its fourth-quarter results on July 29, investors were shocked to see that the company had incurred a net loss of 98.8 million Canadian dollars. The share price reflected this disappointment, declining from $6 before earnings to about $4.50 today. It was just the second time in five quarters the Ontario-based cannabis producer incurred a loss, and it was much larger than the CA$7.9 million loss it incurred two periods earlier.

Image source: Getty Images.

In contrast, Canopy Growth's been in the red in each of its five most recent reporting periods, and in four of those quarters, its losses were much deeper than CA$98.8 million. It's a similar story for Aurora, whose investors have also come to expect losses. The company has only posted one profitable quarter in its past five reporting periods.

Profits aren't all that common in the cannabis industry, and to stay in the black with any sort of consistency, as Aphria has done, is rare. And it's one of the reasons the company stands out among its peers in Canada.

It's also leading in market share

Aphria reported sales of CA$152.2 million in its most recent quarterly results. That was up 5.4% from its third-quarter results and an 18.4% improvement from the prior-year period.

First-quarter 2021 results, released Aug. 10, showed Canopy Growth's revenue for the quarter at just CA$110.4 million. Although that was a 22% increase from the prior-year period, it's still well short of Aphria's tally.

Aurora's most recent quarterly results, which the company released on May 14, showed even lower net sales numbers of CA$78.4 million. Aphria's lowest sales number over the past five reporting periods was CA$120.6 million, still higher than either of its two Canadian rivals' most recent results.

Is Aphria a buy today?

Here's a quick look at how all three stocks have done over the past 12 months:

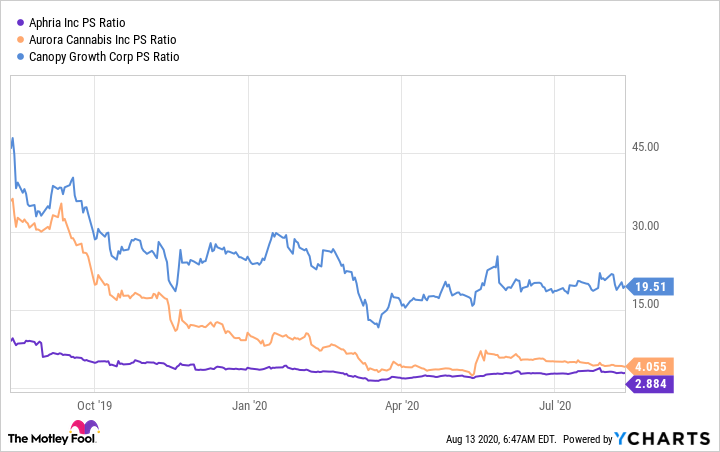

Although it's been declining, Aphria's stock is doing better than the other companies listed here, and even the Horizons Marijuana Life Sciences ETF (HMLSF 3.22%) as a whole. And this is a trend that's likely to continue, given that Aphria's still a cheaper buy when looking at the price-to-sales ratio of all three of these stocks:

APHA PS Ratio data by YCharts

With Aphria's stock tumbling in recent weeks, now could be an attractive time to buy shares of this top Canadian cannabis company. It's definitely made a name for itself as the best Canadian pot stock out there, and it's hard to find a better buy in Canada right now, especially when factoring in its strong sales numbers and impressive bottom line.