Netflix (NFLX -9.09%) has been of the best growth stocks on the market over the last decade, but one question has dogged the company repeatedly in recent years: Will it succumb to the competition?

Netflix is the streaming pioneer and remains the clear leader in the industry, but the landscape has changed significantly in just the last year. Disney+ (DIS 0.16%) has grabbed more than 60 million subscribers around the world since its launch last November, and other services like Apple TV+, AT&T's HBO Max, and Comcast's Peacock are all now available as well.

Netflix's growth has accelerated during the pandemic as extra time at home and a lack of other entertainment options attracted 25.9 million net new subscribers to the platform in the first half of the year, nearly its total subscriber additions for all of 2019. The effect of the pandemic may have obscured the impact of the new wave of challengers -- but one data point should put any worries from Netflix investors to rest.

Image source: Netflix.

Churn, baby, churn

For subscription services like Netflix, churn, which measures the percentage of existing subscribers who leave the service, is a key metric to watch, as it helps show how sticky the service is.

You might expect Netflix's churn to have risen as new competition entices its existing subscriber base to switch, but that hasn't been the case. Netflix doesn't report its own churn rate, but according to Antenna Data, the company's churn rate in the U.S. has been significantly lower than those of its streaming peers in recent months.

Image source: Antenna Data.

From July 2018 to July 2020, Netflix's churn has hovered between 2% and 3% for nearly the entire period -- and for every month during those two years its churn rate was lower than those of its rivals, including Disney+, Hulu, Starz, Showtime, HBO Now, and CBS All Access. At rival streaming services, churn rates ranged from around 3% at Hulu between July 2018 and July 2019, to as high as 11% at Showtime in May 2020, following the series finale of Homeland. There was a similar spike in churn at HBO when Game of Thrones finished its run.

The data underscores a key strength of Netflix. Its broad base of content and the frequency with which new content arrives on the platform keep subscribers hooked and eliminate the risk of its subscriber base going off a cliff once it retires a hit show, as happened recently to Showtime and HBO.

That being said, Netflix has seen some elevated churn from its subscribers who signed up for Disney+. That group had a churn of about 5% in the first few months since Disney+ launched, though it's declined since then, and the impact wasn't enough to have a significant effect on Netflix's overall churn rate.

Image source: Antenna Data.

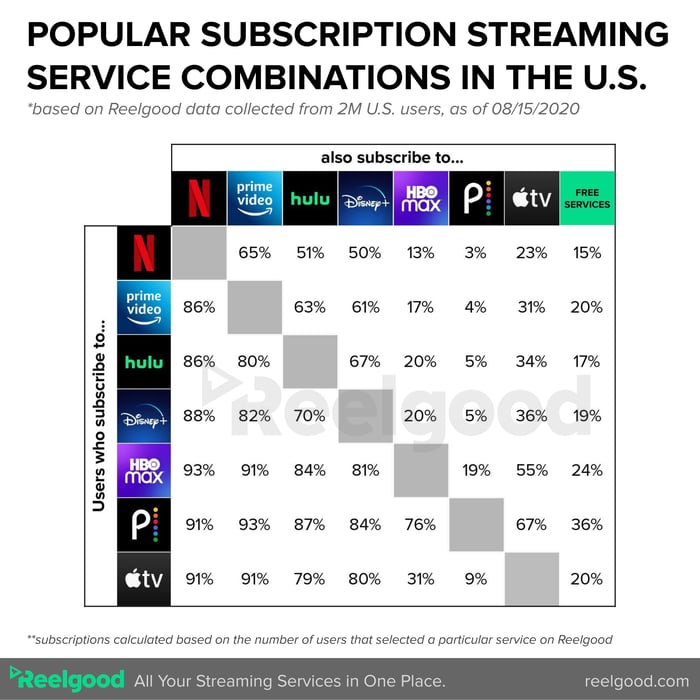

Data from Reelgood, an aggregator of streaming services used by 2 million viewers in the U.S., also confirms Netflix's leadership. According to the site, between 86% and 93% of subscribers to other popular streaming services like HBO Max and Amazon Prime Video also subscribe to Netflix, but no more than 65% of Netflix subscribers also pay for any of the alternatives, again showing that Netflix is the preferred choice of consumers.

Image source: Reelgood.

Still the best

While talk about Netflix's challengers isn't about to disappear, the simple fact is that the company has a massive head start in the streaming industry and a singular focus on streaming, which many of its competitors don't have. The company's base of nearly 200 million subscribers gives it a significant competitive advantage over services that are just starting out, and even ones like Disney+ that have rapidly built their own followings.

That advantage is important, because subscription businesses become exponentially stronger and more profitable as they add subscribers. The money from each additional paying member goes straight to the bottom line, as there are almost no incremental costs. That explains why Netflix is able to spend about $15 billion on content this year, much more than any of its rivals, and is becoming a profit machine, on track to generate a 16% operating margin this year and a 19% operating margin next year, with a goal of increasing it every year.

Netflix expects its subscriber growth to slow down in the second half of the year, as it believes many of the customers it would have added now were pulled forward by the pandemic. Netflix's current model means it doesn't really have a way of generating additional income from existing subscribers, but investors shouldn't be fooled by the expected deceleration in growth: Competition may have arrived, but it's still well behind. Netflix remains the undisputed streaming champ.