Everybody needs healthcare -- or will, at some point. And, when there’s something everyone needs, there’s a huge opportunity for investors.

About $8.3 trillion is spent on healthcare globally. Almost half -- roughly $3.8 trillion -- is spent in the U.S. With the healthcare sector growing significantly faster than the overall global economy, the numbers will almost certainly be much larger by the end of the decade.

How can investors profit from this growth? Here’s what you need to know about investing in healthcare stocks.

Types of healthcare stocks

Different types of healthcare stocks

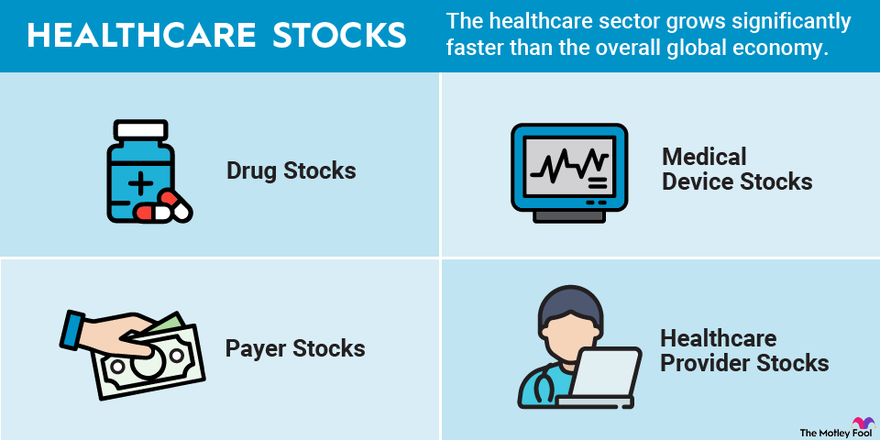

The healthcare sector is so broad that there are several different kinds of healthcare stocks. Four of the most important types are:

- Drug stocks: Drugmakers focus on developing drugs that treat or prevent diseases. Biotech companies use live organisms such as bacteria or enzymes to develop drugs, while pharmaceutical companies use chemicals. Drug stocks range from huge companies with billions of dollars in sales each year to small biotech firms with no products on the market yet.

- Medical device stocks: Medical device companies make devices used to care for patients. The devices range from disposable gloves and thermometers to artificial heart valves and robotic surgical systems. Medical device stocks include many health tech stocks, as well as medical equipment stocks.

- Payer stocks: Payers, including health insurers and pharmacy benefit managers (PBMs), play an especially important role in the U.S. healthcare system. Insurers charge premiums to individuals and employers to pay for healthcare costs, while PBMs administer prescription drug benefits for employers and health plans.

- Healthcare provider stocks: Healthcare providers stand at the front lines, delivering healthcare services to patients. They include hospitals, physician practices, home health companies, and long-term care facilities.

Top healthcare stocks to buy in 2024

Top healthcare stocks to buy in 2024

Strong companies can be found within each type of healthcare stock. We’ll break down at least one example of each with a look at Vertex Pharmaceuticals (VRTX 0.2%), Intuitive Surgical (ISRG -1.69%), Novocure (NVCR 0.33%), UnitedHealth Group (UNH 1.61%), and Teladoc Health (TDOC -1.52%).

- Vertex Pharmaceuticals stands out as one of the top biotech stocks on the market. The company primarily focuses on developing drugs that treat the underlying cause of cystic fibrosis (CF), a rare genetic disease that damages lungs and other organs. Vertex’s newest CF drug, Trikafta, could boost the number of patients its drugs can treat by more than 50%. The company is also developing drugs targeting other rare genetic diseases, as well as more common diseases, including type 1 diabetes.

- Intuitive Surgical is a great example of a medical device stock that also falls into the category of surgical stocks. The company’s Da Vinci robotic surgical system has been used in more than 10 million procedures since its 1999 introduction. The COVID-19 pandemic hurt the company’s business since many elective surgeries were postponed. It also caused a challenging supply chain environment for Intuitive and its customers. Over the long run, the company looks to have tremendous growth opportunities ahead with an aging population requiring the types of surgical procedures for which Da Vinci is frequently used.

- Novocure markets a novel therapy for treating cancer called Tumor Treating Fields (or TTFields). The therapy uses electrical fields to disrupt cancer cell division. TTFields has already been approved for treating glioblastoma (a type of brain cancer) and mesothelioma (a cancer caused by exposure to asbestos). Novocure is evaluating the therapy in clinical studies targeting non-small cell lung cancer, ovarian cancer, brain metastases, and pancreatic cancer. Combined, these additional indications represent a potential market that’s 14 times greater than Novocure’s current market opportunity.

- UnitedHealth Group ranks as the largest health insurer in the world. It also operates one of the biggest PBMs and is a leader in healthcare delivery services. The company’s size, stability, and dividend make UnitedHealth Group one of the most attractive payer stocks on the market. UnitedHealth Group has also expanded its presence in the healthcare provider market with its 2023 acquisition of home health services provider LHC Group.

- Teladoc Health stands out as one of the top telemedicine stocks. The company provides telehealth services by delivering healthcare through the internet and over the phone. Teladoc’s acquisition of Livongo Health in 2020 gave the company a digital health platform to help people manage chronic conditions such as diabetes. The pandemic increased the adoption of virtual care services. Teladoc’s growth slowed as life returned to normal when COVID-19 cases declined. Its stock has also fallen significantly from its highs. However, the company’s post-pandemic prospects should still be very good. Individuals, employers, governments, and health insurers are seeking to control healthcare costs, which telehealth and chronic disease management help to achieve.

What to look for

What to look for in healthcare stocks

How do you find the absolute best healthcare stocks to buy? There are four key things to look for:

1. Growth prospects

The most important thing you’ll want to check out with any healthcare stock is the company’s growth prospects. Determine how quickly revenue has grown in recent years. The future doesn’t always mirror the past. However, if a company hasn’t been able to deliver strong revenue growth so far, it probably won’t in the future.

Read the investor presentations on companies’ websites to learn their strategies for growth and the size of their potential markets. Check out the companies’ rivals to see if their strategies seem to be as good or better. Note that companies will often mention specific competitors by name in their 10-K annual regulatory filings to the U.S. Securities and Exchange Commission (SEC).

Don’t overlook the possibility that mergers and acquisitions (M&A) could boost a company’s growth prospects. Companies that have grown through M&A in the past could be looking for new deals to make in the future.

Keep in mind that deals don't necessarily include an outright purchase of another company. Larger companies sometimes collaborate with smaller players instead of buying them. For example, Vertex Pharmaceuticals teamed up with small biotech CRISPR Therapeutics (CRSP -1.98%). The two companies are awaiting regulatory approvals for gene-editing therapy exa-cel (also known as CTX001) to treat beta-thalassemia and sickle cell disease, two rare blood disorders. They're also working together to develop therapies targeting type 1 diabetes.

2. Financial strength

The SEC filings also include statements that can help evaluate the financial strength of a company. Ideally, a company will already be profitable. If it isn’t, make sure you learn how it plans to achieve profitability and how quickly it expects to do so.

A company’s cash position includes cash, cash equivalents, and short-term investments. It can be found on the balance sheet (a financial statement that lists all the company’s assets, liabilities, and shareholder equity) in the company's annual and quarterly regulatory filings. Think about cash position the same way you’d think about the amount of money in your checking, savings, and retirement accounts: The more, the better.

Another important gauge of financial strength is the free cash flow (FCF) generated by a company. FCF is the cash left over after operating expenses and capital expenditures (which includes money spent on buildings, equipment, and land). As with the cash position, the higher a company’s FCF, the stronger its financial position.

Your dollars and mine, our capital, is helping shape the world.David Gardner, co-founder, The Motley Fool

3. Valuation

You’d want to know how much a new car is worth before buying it. Determining the value of a healthcare stock before buying it is also important so you can make sure you’re paying a fair price.

There are quite a few valuation metrics. The price-to-earnings (P/E) ratio is the most popular and measures the price of a stock in relation to its earnings per share, or what you get in earnings for every dollar you invest.

Some P/E ratios are backward-looking, or reflecting earnings from a previous period (typically the past 12 months). Forward P/E ratios, which use earnings estimates for one year into the future, can be more helpful in assessing the valuation of fast-growing healthcare stocks. Comparing P/E ratios with other stocks in the same industry will help you determine if the stock is relatively cheap or relatively expensive.

Just because a stock’s P/E ratio is higher than those of its peers doesn’t mean it’s a good or bad buy. It could indicate that the company’s growth prospects are much better than those of its rivals. Be sure to also check out the stock’s price-to-earnings-to-growth (PEG) ratio, which incorporates projected earnings growth rates (typically over five years). Stocks with lower PEG ratios (especially when the ratios are less than 1) are more attractively valued than those with higher PEG ratios.

4. Dividends

Some of the best healthcare stocks pay dividends -- a portion of earnings that the company returns to shareholders. Dividends can boost the overall return you receive from owning a stock.

The dividend yield tells you how large a stock’s annual dividend payments are as a percentage of the current share price. Consider the stock’s payout ratio, which measures dividends as a percentage of earnings and indicates how much of the company’s cash is being used to cover the dividend. The lower the payout ratio, the greater the likelihood that the company will be able to keep paying dividends in the future.

Risks

What are the risks of investing in healthcare stocks?

Investing in any kind of stock comes with risks, including the possibility that competitors will develop more successful products and services. Healthcare stocks face these risks, as well as others that are more unique to the sector.

Healthcare is highly regulated. Drugmakers and medical device makers can fail to secure the necessary regulatory approvals to market new products. Regulatory changes can drastically alter a healthcare stock’s growth prospects. In the U.S., the Food and Drug Administration (FDA) oversees the regulation of drugs and medical devices. It’s smart to pay attention to any FDA action related to medical stocks you’re watching.

Many healthcare stocks also face significant litigation risk. For example, biopharmaceutical companies, medical device makers, and healthcare providers can be sued if patients think the companies’ products and services have caused them harm.

In addition, drugmakers and medical device makers must convince payers, including health insurers, PBMs, and government agencies, to buy their products. If companies aren’t successful in obtaining reimbursement approvals, their growth prospects can be reduced.

Many healthcare companies are also highly dependent on Medicare reimbursement levels. Changes will soon be implemented for Medicare that will allow the program to negotiate prices with drugmakers. Some drugmakers’ revenues and profits could be negatively affected as Medicare pays less for some drugs.

Related investing topics

Healthcare stocks should have healthy returns

Despite these risks, the overall outlook for healthcare stocks appears very good over the long term. Aging demographic trends across the world, combined with advances in technology, should open up tremendous opportunities for healthcare stocks -- and provide healthy returns for patient investors.