Investors had some concerns heading into the third-quarter earnings report by Levi Strauss (LEVI 3.65%). Peers in the apparel industry have been complaining all summer about inflation and supply chain challenges, after all. And the jeans specialist faced new consumer traffic restrictions over the summer due to resurging COVID-19 cases.

Yet the apparel chain calmed those fears in its announcement this week. Not only did Levi beat growth expectations, but it was also able to boost profitability by raising prices.

Let's dive right in and take a closer look at three takeaways from the report.

Image source: Getty Images.

1. Sales trends point upward

Sales rose 41% year over year to outpace Wall Street's targets. Most of that spike was due to unusually low sales a year earlier because of the pandemic. But Levi Strauss has improved on its results from two years earlier as well, with sales up 3% compared to Q3 of 2019.

Executives said they were pleased with the performance, especially given that about 10% of stores, primarily in Asia, were closed at some point during the quarter due to local COVID-19 restrictions. "We delivered a strong quarter," CEO Chip Bergh said in a press release, "with revenue growth versus pre-pandemic 2019 levels, despite a more difficult macro-environment than we expected."

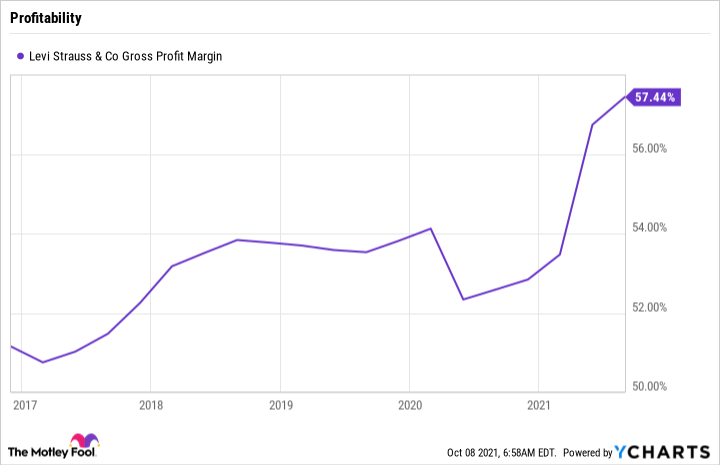

2. Raising prices helped manage rising production costs

That difficult environment included rising costs on everything from raw materials to shipping. However, Levi's bottom line showed no stress from these pressures.

Instead, gross profit margin increased for a third straight quarter, jumping to 57.6% of sales. After adjusting for one-time charges, that profitability figure was up 3.9 percentage points thanks to the combination of higher prices and a tilt in demand toward direct-to-consumer sales.

LEVI Gross Profit Margin data by YCharts.

Levi Strauss generates more profits from these e-commerce sales than it does in its wholesale business. That helps explain why management is moving so aggressively to establish a strong online presence.

There was other good financial news in the period, too, including the fact that Levi's paid down all the new debt it took on during the pandemic crisis. Management was also free to make bold capital moves, including the $400 million acquisition of Beyond Yoga. "Our third quarter performance combined with our confidence in our outlook," CFO Harmit Singh said, "enables us to allocate capital across all of our core priorities."

Looking out to the holidays

Levi Strauss executives hiked their 2021 outlook following the strong third quarter. Sales are projected to rise by 20% to 21% in Q4, which would mark accelerating growth as compared to the 2019 period. The forecast implies that management sees no significant supply chain, inventory, or cost challenges that might threaten to slow its momentum.

Further out, investors can look forward to Levi's business continuing to shift toward e-commerce even as the portfolio grows to include more apparel brands. Shoppers still have a strong appetite for premium products, and all of these factors should help lift the chain's profit margin up toward that 60% mark.

At the same time, Levi Strauss is approaching the 2022 fiscal year with solid finances and plenty of cash. This should allow management to continue to aggressively invest in growth priorities and return cash to shareholders through dividends and stock buybacks.