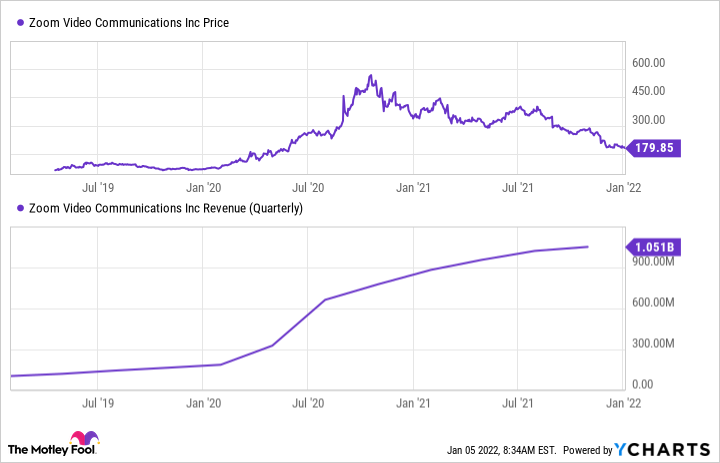

Shares of Zoom Video Communications (ZM -1.03%) have been on the skids since peaking in late 2020. Investors who have held on this long have seen the stock fall by more than two-thirds, and many may be eager to exit their positions.

But before you dump Zoom -- or any poorly performing stock -- it pays to understand why the bottom fell out in the first place.

Image source: Getty Images.

Why Zoom's down

In early 2020, the market went nuts for Zoom because its revenues were rocketing higher. However, many of the businesses that were scrambling for work-from-home solutions back then likely see their Zoom subscriptions as a little less important now.

The rapidly increasing demand that inspired the market to push Zoom's stock price through the roof has tapered off. Yet it's important for investors to note that Zoom continues to grow at an impressive pace.

For its fiscal 2022 (which will end Jan. 31), Zoom expects to report a total of $4.1 billion in revenue. That's 54% more than in the previous year, and a lot of its revenue flows down to the bottom line. Over the past 12 months, the company recorded $1.7 billion in free cash flow.

Why Zoom could rise again

It's been more than a year since Microsoft (MSFT 0.55%) dropped its 40-minute time limit on video chats for non-paying users of its Teams service. Teams' popularity has grown, but demand for videoconferencing appears high enough that Microsoft's offering probably isn't a major threat to Zoom. In its third quarter, Zoom reported an impressive 130% recurring revenue retention rate among customers with more than 10 employees.

Microsoft's videoconferencing service competes with Zoom for traditional enterprise customers. Luckily, Zoom is so easy to use that it's finding lots of new customers eager to host their own events. For example, its OnZoom service gives instructors, artists, and other types of event hosts a free place to bring their audiences together. By making it easy to monetize virtual events, it also gets the first shot at hobbyists hoping to take their talents to the next level.

Virtual events appeal to lots of artists who don't enjoy lugging their gear from gig to gig. Independent musicians, trainers, and motivational speakers also have a chance to sell tickets, music lessons, and merchandise directly to attendees worldwide.

Nothing beats a live show, but OnZoom event attendees never need to stand in a line, and won't need to leave early to beat the traffic.

Not time to sell

The consumer market for hosting virtual events is growing fast, and I believe we've only seen the tip of the iceberg. Competition for the enterprise market will make Zoom's growth in 2022 seem relatively underwhelming, but now isn't the time to let go of this stock.

I won't be surprised if Zoom keeps growing its top and bottom lines by more than 20% annually for at least another five years. Yet despite that, the stock has been trading at around 36.8 times forward earnings. Instead of thinking about selling Zoom stock, it's probably a good time to think about buying more.