What happened

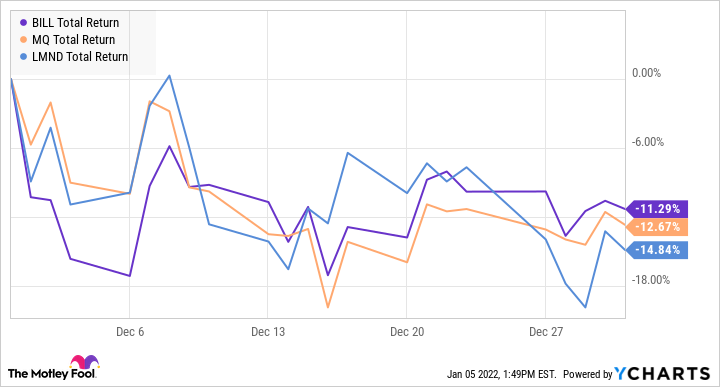

Shares of Bill.com Holdings (BILL -2.26%) dropped 11% in December by no fault of their own. The company didn't have any major news last month, but its stock was another victim of investors bailing out of high-valuation growth stocks. Bill.com's price chart is almost identical to those of disruptive fintech peers Lemonade (LMND 0.83%) and Marqeta (MQ -2.92%). The stock's performance was more about capital market dynamics than anything related to the company's fundamentals.

BILL, MQ, LMND total return level. Data by YCharts.

So what

Bill.com has had impressive operating performance. The company's revenue rose 150% in its most recent quarter, and it's forecasting a 130% sales increase for the next year.

It's still free-cash-flow negative, but the current $25 million quarterly outflow looks sustainable with nearly $3 billion in cash and short-term investments on the balance sheet. Since the company isn't in financial trouble, it's fine to burn cash to achieve this astounding growth rate. Bill.com's sales and marketing budget is 53% of its revenue; research spending is around 36% of sales. Those are both very high, and sales eventually have to outpace expenses over the long term for this business to become stable.

There's absolutely nothing wrong with growth stocks, but they're naturally more volatile. In Bill.com's case, its valuation is based on potential. It doesn't produce predictable net cash flows right now, so investors are forced to make predictions and wade into uncertainty.

High valuations and uncertainty are a dangerous mix when investors are cutting back on risk. The Fed recently announced plans to taper its expansionary monetary policy, and interest rate hikes look imminent. As rates rise, investors' risk appetite is likely to wane. Growth stocks with high valuations are likely to be among the hardest hit. There's no surprise that Bill.com stock struggled last month.

Image source: Getty Images.

Now what

Bill.com is up 515% since its December 2019 initial public offering, even after the recent drop. Its price-to-sales ratio is still high at 61. Capital market conditions and investor sentiment drove the stock to a level that would be difficult to sustain when circumstances shifted. We're in the middle of that shift now.

It's no surprise that investors are excited about Bill.com. It's a software-as-a-service platform that automates back-office financial operations for small and medium-size businesses. There's an obvious need for these services, which stamp out inefficiencies and reduce customers' expenses. The growth catalysts are clear.

The issues relate to uncertainty and valuation, though. Bill.com's stock price assumes several straight years of uninterrupted financial performance. That might come true, but there are operational challenges and a number of competitors that could interfere with the narrative. Fintech is an area of major disruption, and there are several innovators that could stand in one another's way.

If Bill.com shows any weakness, or indication that its superb growth will be interrupted, the stock has a lot of room to fall. Things will be especially dicey as interest rates rise.