While the idea of trying to find a stock that could triple over the next decade may sound overwhelming, it equals out to about 12% annualized growth over that time -- only slightly above the S&P 500's long-term average.

Furthermore, by keeping a truly long-term focus in mind when making investments, today's discounted valuations for many growth stocks may offer compelling prices to add to or dollar-cost average into a new position entirely.

Image source: Getty Images.

With this in mind, we will look at three supercharged companies that are still delivering high sales growth yet have been hammered over the last three months -- creating intriguing multibagger potential over the next decade.

Data by YCharts.

1. Sea Limited

Led by its mission "to better the lives of consumers and small businesses with technology," Sea Limited (SE 4.71%) offers investors a unique blend of diversification, optionality, and high growth across three wildly popular industries.

First, its digital entertainment division, Garena, saw bookings rise 29% year over year for the third quarter to $1.2 billion. With 729 million active quarterly users, this division excelled, thanks to its massively popular multiplayer game Free Fire. The game has become a profit center for Sea Limited.

Posting $715 million in earnings before interest, taxes, depreciation, and amortization (EBITDA), Garena cancels out the negative EBITDA stemming from its other two business units and essentially funds their growth. Recording nine consecutive quarters as the highest-grossing mobile game in Southeast Asia and Latin America, this strong EBITDA should continue to fuel the company's broader growth ambitions.

Meanwhile, its e-commerce unit, Shopee, continues to post incredible growth, seeing its gross merchandise volume jump by 81% to $16.8 billion during Q3. Better yet, the unit's revenue grew by 134% year over year, marking nine consecutive quarters of triple-digit growth for the department. On top of this, Shopee was Google Play's No. 1 shopping app globally, rated by the amount of time users spent with the app.

Finally, its digital financial services unit, SeaMoney, more than doubled its total payment volume year over year to $4.6 billion during Q3. Along with this mobile wallet payment volume, Sea Limited looks to add multiple financial services over time, adding yet another layer of promising growth potential.

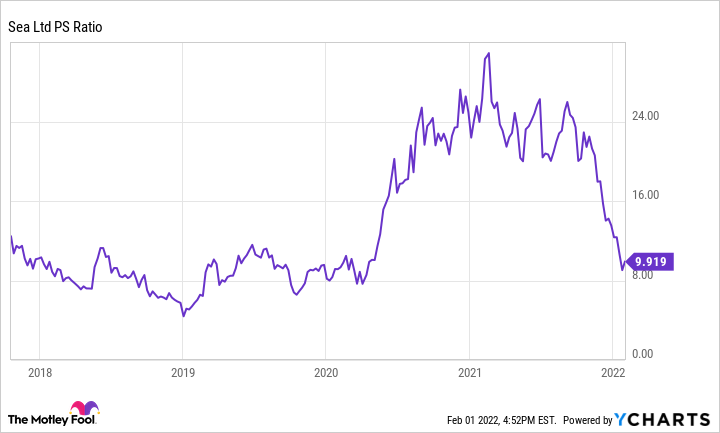

Overall, annual revenue grew by 131% year over year, making its nearly 60% drop in the last three months an intriguing entry point for new potential investors.

Data by YCharts.

Now trading at a price-to-sales (P/S) ratio of less than 10, Sea Limited is closer to historical lows despite generating immense sales growth, making it a prime candidate to triple over the next decade.

2. Veeva Systems

Founded in 2007, cloud solutions expert Veeva Systems (VEEV 1.50%) has rapidly become a leader in the life-sciences industry. Through its two segments, Research and Development (R&D) and Commercial, the company offers a wide array of cloud, data, and business consulting solutions.

Veeva's founder and CEO, Peter Gassner, received a 91% approval rating from his employees. according to Glassdoor. He led the company to become a public benefit corporation (PBC) in early 2021. While still for-profit, this change highlights Veeva's continued focus on conscious capitalism and places a legal requirement for equal accountability to all stakeholders.

Better yet, this strong company culture comes with robust growth metrics. Specifically, management estimates its calculated billings will be just shy of $2 billion for 2022, a 21% jump year over year.

Furthermore, the vast majority of the company's revenue comes from incredibly sticky subscription sales. Not only is this subscription revenue very consistent, but it also boasts a gross margin of 85% -- which goes a long way toward explaining Veeva's massive 44% free cash flow (FCF) margin over the last year.

All in all, Veeva's quarterly revenue growth of 26% year over year, paired with its cash-generating prowess, make it an up-and-coming prospect to watch. Having seen its share price drop 30% in the last three months, the company now trades at 44 times FCF and could quickly outgrow its valuation over the next decade.

3. Celsius Holdings

Despite growing annual revenue by 106% year over year, energy-drink specialist Celsius Holdings (CELH 2.88%) has watched its share price plummet by over 50% in the last three months. Thanks to its proprietary formula, Celsius seems to have merged the worlds of energy drinks and fitness -- a rare feat to accomplish, let alone sell to customers.

Through its unique blend of ingredients, studies have shown that one serving of Celsius burns just over 100 calories by providing a short-term boost to its consumer's resting metabolism. This boost makes it a great pre-workout drink that helps increase consumers' endurance while assisting them to nearly double their amount of fat loss compared to those who do not consume the drink.

On the investing front, the stock's recent decline in price has it trading at a P/S ratio it hasn't seen since 2020.

Data by YCharts.

Trading around 16 times sales, Celsius now trades much closer to its biggest competitor, Monster Beverage (MNST -0.22%), but grew its annual sales roughly five times faster than the latter's 20% mark over the last year. Should the companies post similar growth in the upcoming year, their P/S ratios would be virtually the same, potentially indicating that Celsius's growth may currently be undervalued.

Ultimately, Celsius offers investors a rare mashup of the fitness and energy drink industries. Moreover, since its sales growth over the last several years was meaningful, this is far from a short-term fad, making it an intriguing stock to consider for the next 10 years.