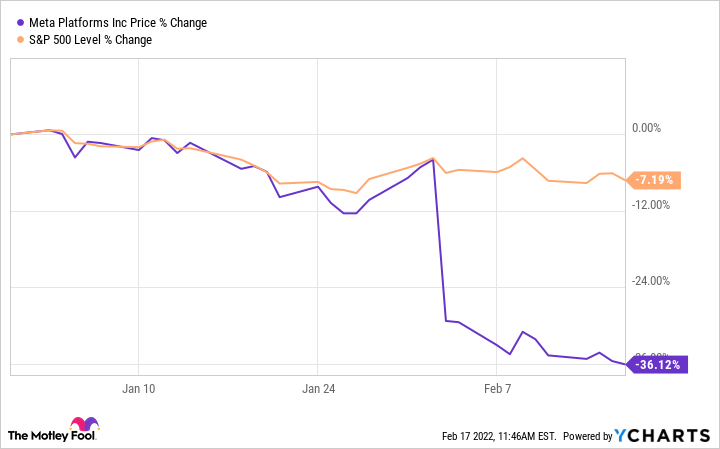

Facebook parent Meta Platforms (META 0.14%) has gotten off to a rough start in 2022 -- its stock price is down by more than 35% so far this year. That huge decline was largely triggered by a fourth-quarter earnings report that left investors unimpressed with both the social media giant's recent performance and its guidance.

There is no doubt that Meta Platforms faces several issues -- notable among them, competition from other social media websites and apps such as TikTok, and the impact of Apple's moves to improve privacy protection and reduce the ability of apps to track users, which is taking a significant toll on digital advertising revenues. Still, Meta Platforms remains an excellent long-term bet for investors.

1. Competitive advantages

Meta Platforms has faced severe issues before, including numerous privacy scandals and regulators seeking to break up the business. None of these headwinds have stopped its progress -- and that's in large part because its user base has generally kept growing despite all the negative publicity.

The business is solid and resilient, arguably because it benefits from at least two related competitive edges: switching costs and the network effect. People looking to connect with family and friends via a social platform can still hardly do better than to seek them out among Facebook's 1.93 billion daily active users. And the number of daily active users across its entire family of apps -- which includes Instagram, WhatsApp, and Messenger -- was 2.82 billion as of Dec. 31.

Image source: Getty Images.

This vast network provides a solid incentive to its users to stay put, as few of its rivals can compete with it in terms of reach. Further, the value of Meta Platforms' services increases for each user as more people use them. That's the network effect.

Thanks to that competitive moat, the company has at least one of the tools it will need if it's to remain a leader in its space.

2. The metaverse

Meta Platforms' rich ecosystem also ensures that advertisers and marketers looking to reach a broad audience -- or specific slices of that audience -- will continue to flock to its websites and apps. Spending on online advertising is expected to keep growing rapidly in the coming years. Even with the privacy-related changes Apple is making to its operating systems, investors can expect Meta Platforms to be a major beneficiary of the growth of online advertising.

But the tech giant is pursuing other revenue opportunities, and arguably the most-discussed right now is the metaverse -- which tech pundits describe as an immersive, persistent 3D virtual world that people will be able to access largely via virtual reality (VR) and augmented reality (AR) devices, and in which they can interact with one another and their surroundings.

Meta Platforms has already invested billions of dollars into making the metaverse a reality. In October, CEO Mark Zuckerberg said that spending related to the Facebook Reality Labs segment -- the company's AR and VR unit -- would reduce its 2021 operating profits by about $10 billion and that its annual investments in the metaverse would only increase in the coming years.

It will be a while before the metaverse takes shape and it becomes clear whether these investments will prove profitable. Still, the opportunity could be enormous. For instance, Goldman Sachs analyst Eric Sheridan thinks the metaverse could be an $8 trillion opportunity. Meta Platforms is arguably one of the leaders of this trend, and that gives it a substantial opportunity for long-term growth.

3. A great time to buy

Meta Platforms' shares have gotten a lot more affordable lately. It is worth comparing the tech giant's forward price-to-earnings ratio to those of several other social media giants, namely Pinterest, Twitter, Snap, as well as Google and YouTube parent Alphabet.

FB PE Ratio (Forward) data by YCharts.

By that metric, Meta Platforms' shares look cheap compared to those of its peers. True, most of these competing platforms are smaller, and the market may therefore perceive them as having more growth potential. Still, the tech giant's growth opportunities are nothing to sneeze at.

The company's forward price-to-earnings ratio is near its lowest level in over a year, and its price-to-free-cash-flow ratio of 15.9 is about as low as it has been for more than five years. At current levels, Meta Platforms looks like an excellent bargain -- and given the tech giant's growth opportunities and its wide moat, investors should consider holding onto its shares for the long haul.