Micron Technology (MU 3.06%) has turned out to be a terrific investment over the past decade, with shares of the memory specialist crushing the broader market's returns by a huge margin.

A $1,000 investment in Micron stock a decade ago would be currently worth just over $10,000.

Micron stock could repeat its outstanding run over the next decade, or do better, as the demand for memory chips that it sells will get stronger. Let's look at the reasons why Micron Technology stock could 10x once again in the next 10 years.

MU data by YCharts.

Micron will benefit from the memory market's secular growth

The dynamic random access memory (DRAM) market generated $24.6 billion in revenue back in 2012, according to memory market intelligence provider DRAMeXchange. By the end of 2022, global DRAM revenue is expected to hit nearly $92 billion. This substantial increase in DRAM industry revenue over the past decade has been driven by an increase in the need for computing power.

For instance, the average DRAM content in each smartphone was 666 megabytes (MB) back in 2012, a figure that increased eightfold by the end of 2021 to 5.3 gigabytes (GB). Additionally, the deployment of hyperscale data centers that require high data transfer speeds and the increase in the DRAM capacity of computers and laptops has been driving this industry's terrific growth.

The good news for Micron investors is that the DRAM market will keep expanding in the long run. Mordor Intelligence estimates that global DRAM revenue could exceed $100 billion by 2026, though it won't be surprising to see the market grow at a faster pace for a few simple reasons.

Image source: Getty Images.

First, the smartphone market is going to be a big catalyst for DRAM sales in the coming years. That's because 5G smartphones are using 50% more DRAM as compared to 4G devices. With the 5G smartphone market expected to clock a compound annual growth rate (CAGR) of nearly 125% through 2025, the need for mobile DRAM is going to increase rapidly.

Second, graphics cards that are now used in several applications ranging from personal computers to gaming consoles to data centers and even self-driving cars also use DRAM. Now, the global graphics card market is expected to grow at an annual rate of 33% through 2027, so this is another area that would create the need for more memory chips.

Meanwhile, there are emerging memory technologies on the horizon to support the need for faster computing. The market for such next-generation memory chips could exceed $30 billion in revenue by 2030, growing at an annual rate of nearly 28% through the forecast period. All of this indicates that Micron's addressable revenue opportunity in the DRAM market is set to increase in the long run. This bodes well for the company as it gets 73% of its revenue from this space.

On the other hand, the NAND flash market that supplies a quarter of Micron's revenue is also expanding rapidly thanks to the growing need for storage in data centers, smartphones, and computers. By 2027, the NAND flash market is expected to reach $94 billion in revenue as compared to $66 billion last year.

More importantly, Micron is in a nice position to generate incremental long-term revenue thanks to the expansion of its end markets. That's because the company held a 22% share of the DRAM market last year, and the good part is that it has been gaining ground over rivals. The company could steal a march over rivals in the NAND flash market as well thanks to its latest product development move. Micron has started the mass production of the industry's first 176-layer NAND data center solid-state drive that's currently being evaluated by several hyperscale and data center customers.

As such, it won't be surprising to see Micron corner a bigger share of the NAND flash market, compared to just over 10% last year.

Solid earnings growth could send the stock soaring

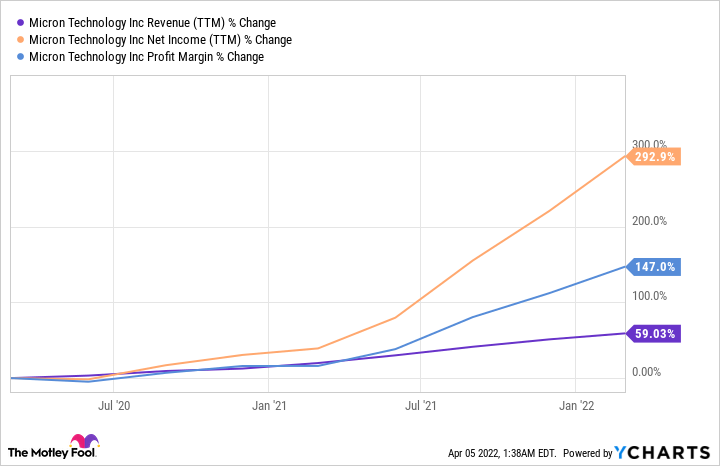

Micron Technology has been benefiting big time from the strength of the memory market in recent years, as evident from the chart below.

MU Revenue (TTM) data by YCharts

The chipmaker released its fiscal 2022 second-quarter results on March 29 and revealed a 25% year-over-year increase in revenue to $7.79 billion. Adjusted earnings shot up 118% over the prior-year period to $2.14 per share. The company easily crushed Wall Street's expectations and issued healthy guidance, which indicates that its momentum is here to stay.

The potential growth of Micron's end market could help it maintain its impressive pace of growth. Not surprisingly, analysts expect its earnings to increase at a 30% compound annual growth rate over the next five years, which is nearly identical to the annual growth it has seen in the past five years.

If Micron could sustain a 30% annual earnings growth rate for the next 10 years thanks to booming memory demand, its earnings could hit $83 per share after a decade as compared to $6.06 per share last year. Multiplying the estimated EPS figure with Micron's five-year average forward earnings multiple of 10 points toward a stock price of $830 after 10 years, indicating that Micron stock has the potential to grow 10 times over its closing price of $77 on April 4.

And, with Micron trading at just 9.5 times trailing earnings as compared to its five-year average multiple of 15, investors are getting a great deal on this growth stock right now that they may not want to miss.