In a market teeming with negative sentiment, Costco (COST -0.12%) continues to rally. The retail juggernaut has climbed 54% in the past year, strikingly higher than the S&P 500's 5% gain in the same time frame. The company's long-term performance has been stellar as well -- Costco has returned a walloping 272% to shareholders over a five-year span, implying an average annualized return of 54%.

Given the ambiguity surrounding the stock market today, Costco may appear to be a worthy investment opportunity. After all, the company is as consistent as they come and boasts a superb financial track record. Although I don't know if Costco shares will continue in their upward trend moving forward, I am certain that the company isn't flawless.

With that in mind, let's explore three potential downsides all investors should be aware of before buying Costco stock today.

Image source: Getty Images.

1. Growth is decelerating

Costco had a tremendous outing in 2021. The membership-only retailer expanded both its top and bottom line by 20% year over year, up to $195.9 billion and $11.09 per share, respectively. The positive momentum has carried over into 2022: Wall Street analysts are modeling sales and earnings of $221.8 billion and $13.11 per share, respectively, this upcoming year, representing annual increases of 13% and 18%.

Considering Costco's behemoth size, investors can't expect high levels of growth forever. Wall Street analysts forecast the company will generate $276.2 billion in revenue and $17.81 in earnings per share by 2025, indicating annualized growth rates of only 7% and 10% from 2021 levels, respectively. This isn't awful growth, but it surely doesn't seem ideal when taking into account the company's all-time high valuation.

2. Unattractive valuation

Historically, Costco has traded at a premium relative to its industry peers. The company's membership model, top-notch private label, and unique ability to sell items at unbeatable prices have compelled investors to feel comfortable paying a steeper price for the stock in the past.

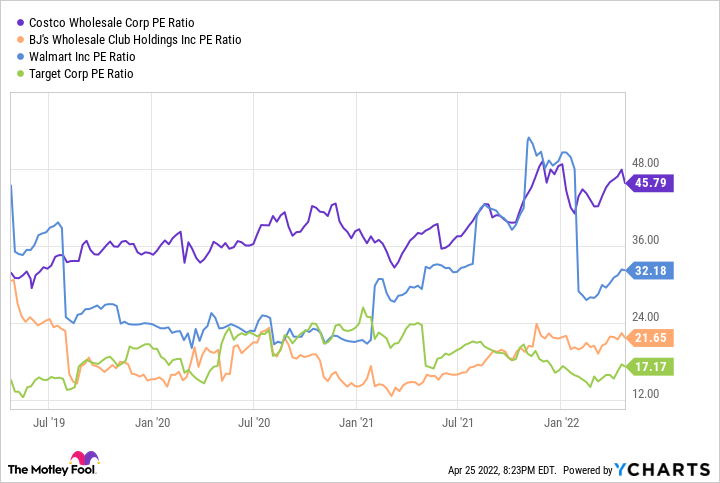

Today, Costco is trading at 46 times earnings. This is well above competitors BJ's Wholesale, Walmart, and Target, which currently carry price-to-earnings multiples of 22, 32, and 17, respectively. In fact, the median price-to-earnings (P/E) ratio of the four retailers is 27, meaning Costco is trading above a 50% premium to its close industry peers.

COST PE Ratio data by YCharts.

Even if Costco has historically enjoyed a steeper valuation than its competition, the company's latest P/E multiple appears dreadfully high. Costco's five-year average P/E ratio is 36, or 25% below today's levels. So even if you're willing to pay a loftier price for the retail titan, the company's current valuation looks too expensive to justify at this time.

3. The threat of e-commerce

It's soundly understood by now that we're witnessing a paradigm shift toward e-commerce in the retail sector. Costco is well-known for its in-store shopping experience, so it's possible that e-commerce alternatives could eat away at the company's sales in the long run. In 2021, e-commerce revenue made up only 7% of Costco's total top line. Although it's important to preserve its core business, Costco must work to continuously improve its e-commerce sales in the coming years.

E-commerce revenue also serves as a way to spark growth as store openings unwind over time. Inevitably, Costco will reach a point where it can no longer resort to new locations to drive additional growth. And given that the company's e-commerce segment currently represents less than 10% of total sales, Costco's untapped potential in this arena is absolutely massive.

I'd wait to buy Costco

Costco is a world-beater in the retail space, but I wouldn't suggest buying the stock today. With growth projected to unwind in the future and a valuation at record highs, investors aren't presented an optimal buying opportunity at the moment. The company's unwillingness to adopt e-commerce as rapidly as the remainder of the industry is also something to closely keep an eye on moving forward. I think Costco will continue to perform well over the long run, but it wouldn't be unwise to hold off on buying the stock until it experiences a pullback.

In short, Costco is a great company, but it's not a great investment in today's market.