The last two years have been much different than the decades that preceded them. One industry where the pandemic has made the most impact is life sciences. That's the study of living things, and it includes the instruments, devices, and biological material used to research and develop treatments.

One of the largest companies in the space is Thermo Fisher Scientific (TMO 0.60%). At a market capitalization of $200 billion, it's not accurate to say the company is under the radar. But its steady execution of a tried-and-true strategy has rewarded investors for decades while garnering little fanfare. Even after a 27,000% return (16.5% per year) over the last 40 years, there are still good arguments for buying shares. There is also a reason to be cautious.

Image source: Getty Images.

A life sciences portfolio full of growth

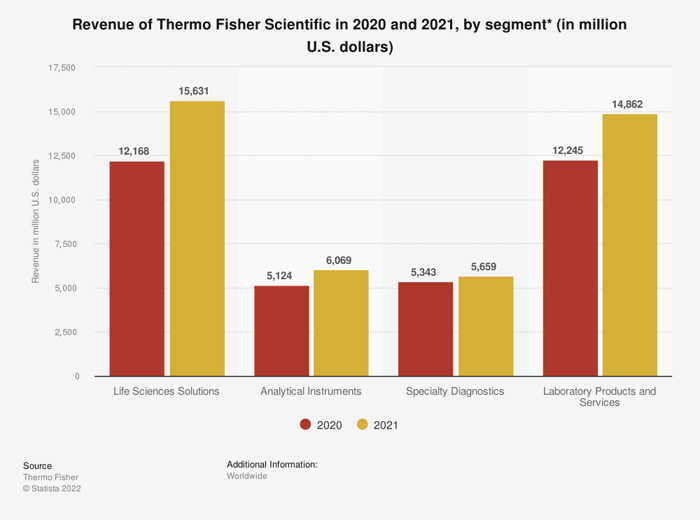

The company has amassed a portfolio of products that span the entire industry. Its life-sciences solutions business includes bioreactors and gene sequencers. The analytical instruments segment contains products like electron microscopes and equipment for chemical analysis, mass spectrometry, and chromatography. Its specialty diagnostics business focuses on testing. And the laboratory and biopharma division offers consumables, as well clinical research and services to biotech and pharmaceutical companies.

That portfolio puts it up against industry heavyweights like Danaher (DHR -0.36%), Illumina (ILMN 0.63%), and Agilent Technologies (A 0.22%). Despite the stiff competition, it has grown revenue faster than the others over the last five years. Every segment of its business grew in 2021. A lot of that has to do with its strategy.

Gaining scale by rolling up the industry

Thermo Fisher has been making larger acquisitions over the past decade to build up that portfolio. The list of deals is long, and the dollar amounts of the biggest are significant. In 2011, it bought Swedish blood-testing company Phadia for $3.5 billion. It also grabbed chromatography business Dionex for a mere $2.1 billion that year.

In 2013, it purchased Life Tech for $13.6 billion. Life Tech was the home of a fast-growing genetic testing business that the industry still points to as the key to personalized medicine. In 2016, management snapped up electron microscopy company FEI for $4.2 billion. The following year brought the acquisition of pharmaceutical contract manufacturer Patheon for $7.2 billion.

But the largest deal was last year's $17.4 billion acquisition of contract research business PPD. That deal opened the door to supporting drug developers. With it, the company added a services arm for its biotech and pharmaceutical customers. At the time, CEO Marc Casper called it the company's fastest growing end market.

Adding it up and smoothing the expenditures over time, Thermo Fisher has spent about 20% of sales on acquisitions over the past decade. Although Casper has acknowledged the environment for mergers and acquisitions is getting more restrictive, he also said it is still very fragmented, with plenty of potential targets if the returns look favorable.

Data source: Thermo Fisher Scientific. Chart by author.

Shares may have to grow into the valuation

It's obvious Wall Street loves the strategy and how well Casper and his team are executing it. Over the last decade, the price-to-sales (P/S) ratio climbed from about 2 to over 5. That seems more expensive.

TMO P/S ratio. Data by YCharts.

But the price-to-earnings ratio has hovered between 20 and 40 over the same span. That's a testament to management's keen eye for businesses with higher profit margins. Despite what Casper implied, acquisitions might not be so easy in the future. And that could leave the stock stuck in neutral. Analysts aren't expecting earnings per share to get back to 2021 levels until 2024.

As for new deals, the Biden administration has said it would not negotiate with companies to close deals if they reduce competition. Instead, it will sue to block them. That's probably doubly true given where inflation is.

But removing that tool from Thermo Fisher's toolbox could make growth for the company hard to come by. And that could make investors much less willing to pay the premium valuation the stock now enjoys.