Amazon (AMZN -2.40%) shareholders will vote on carrying out a 20-for-1 stock split at its annual meeting later this month. It's highly likely that the move will be approved, paving the way for the split to be completed in June.

Splitting the stock into smaller, easier-to-purchase shares could make investing in the company significantly more attractive to a wider pool of investors and work to increase trading volume. These dynamics have previously helped power gains for other companies, and it's not unreasonable to think they could create bullish catalysts for Amazon. However, there are at least five better reasons to purchase the company's stock ahead of the upcoming split.

Image source: Getty Images.

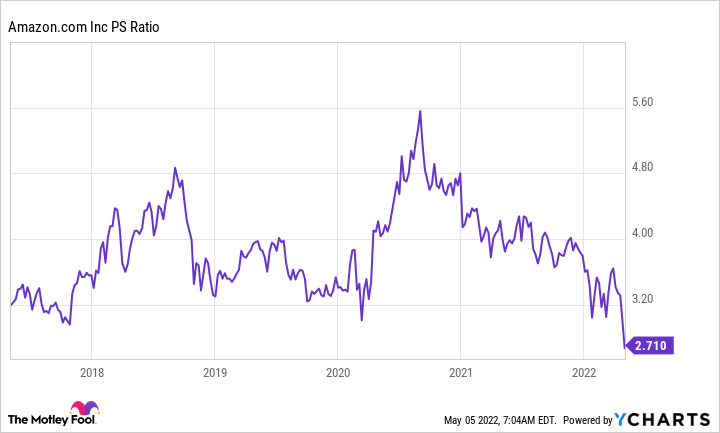

1. Amazon is cheaper than it has been in years

Amazon stock has been hit hard following the company's recent first-quarter earnings release. Due to Amazon's big investment in electric-vehicle company Rivian, the tech giant wound up posting a loss of $7.56 per share last quarter. Revenue in Q1 also fell slightly short of the average analyst target, and earnings per share would have fallen short of the market's expectations even if it weren't for the adverse impact from Rivian's sinking stock price.

AMZN PS Ratio data by YCharts.

While Amazon is facing headwinds and posted performance that underwhelmed the market in Q1, the upside for investors is that the stock hasn't looked this cheap in years. Recent top- and bottom-line performance, challenging backdrops for some key segments, and investment initiatives at the company have created a perfect storm to shake investor confidence.

In short, Amazon is spending big to help power its long-term expansion at a time when sales growth is slowing due to waning pandemic-driven tailwinds. That's also causing earnings to head in the wrong direction.

With risk factors including high inflation and interest rate hikes causing investors to move out of stocks, it's not hard to see why the market hated Amazon's Q1 results, and the stock is now down roughly 33% from the high it hit last year. On the other hand, this is a company that still looks remarkably well-positioned to win the future, and big sell-offs have created a great buying opportunity.

2. The cloud business looks incredibly strong

While the e-commerce business remains Amazon's largest sales driver, the company's cloud services segment plays a much bigger role in generating profits. Amazon Web Services (AWS) grew sales 36.5% year over year in the first quarter and posted a gross margin of 35.3% -- representing a substantial improvement from the roughly 30% gross margin it posted for all of last year.

Because of high infrastructure and operational costs, e-commerce tends to be a relatively low-margin business. Meanwhile, as AWS is showing, cloud-infrastructure services can be enormously profitable at scale. AWS provides the backbone for a huge cross-section of the modern internet, and Amazon should continue to benefit from more sites, services, and applications coming online.

AWS accounted for just 10% of overall revenue last quarter and contributed roughly $6.2 billion in operating income, pushing the company to an operating profit of roughly $3.67 billion despite substantial losses from other segments. Amazon's biggest earnings driver remains in great shape, and it would be a mistake to overlook the big picture because of near-term turbulence for other segments.

3. The e-commerce business still has room for big growth

Shelter-in-place and social-distancing conditions created a surging demand for Amazon's online retail business. With that tailwind now receding, the company is also facing rising costs due to inflation, high shipping expenses, and its own massive infrastructure and technology spending push. The combination of these factors is painting an undesirable picture: anemic growth and soaring expenses.

However, the near-term picture is masking the fact that Amazon's e-commerce business remains positioned to deliver strong performance over the long term. Even amid a pandemic-elevated backdrop, e-commerce accounted for just 13.2% of overall retail spending in the U.S. last year and has plenty of room for expansion. Amazon retains a leading position in the online retail market, and its massive investments to shore up dominance in the space will likely have huge long-term payoffs.

Image source: Getty Images.

4. Amazon is a fantastic innovator

Between e-commerce and cloud-computing services, Amazon has shaped two of the most influential industries in the world. The company has also used its strengths in online retail and data analytics to rapidly gain market share in the digital advertising space.

While the advertising business's sales of roughly $7.9 billion fell short of the average analyst estimate for sales of $8.2 billion, the unit still managed to grow sales 25% year over year. Given that U.S. gross domestic product unexpectedly contracted 1.4% in the quarter, that performance looks pretty good.

Digital ads is emerging as a new business pillar, but the company is hardly resting on its laurels. Amazon is continuing to pursue growth initiatives in categories including artificial intelligence, robotics, and autonomous vehicles, and it's likely the company will continue to shape influential tech and service trends through the next decade and beyond.

5. The company is betting its own shares are cheap

When Amazon announced plans to carry out a 20-for-1 stock split back in March, it also announced that its board had authorized $10 billion in stock buybacks. While share buybacks have the effect of boosting earnings per share by reducing the total number of shares outstanding, repurchases are sometimes viewed as an admission that a company can't come up with better ways to use funds to drive growth.

Given that Amazon is still making massive technology, infrastructure, and research and development investments, the concerns that sometimes accompany stock buybacks don't look applicable here. The company's management team saw a worthwhile opportunity to repurchase shares even before recent sell-offs made the stock even cheaper, and long-term investors should act on the chance to buy a piece of this great company at a great price.