Growth stocks have been hammered in 2022 amid sky-high inflation and interest rates. The Federal Reserve, in fact, just raised interest rates by 0.75 percentage points, the largest such increase since 1994, after inflation hit 40-year highs.

How do interest rates affect growth stocks? There are lots of moving parts, but without getting into the technicalities, higher interest rates compel consumers to spend less and makes debt costlier for corporates. That hurts sales and profits, which drives stock prices lower.

A sell-off in growth stocks, however, is also one of the best times to invest. Top growth stocks can help long-term investors build life-changing wealth, and since growth stocks typically trade at a premium, there's nothing better than if you can buy them during a market sell-off. Here are three growth stocks down more than 70% from their all-time highs to buy now.

This stock is about to split, but that's not why you should buy

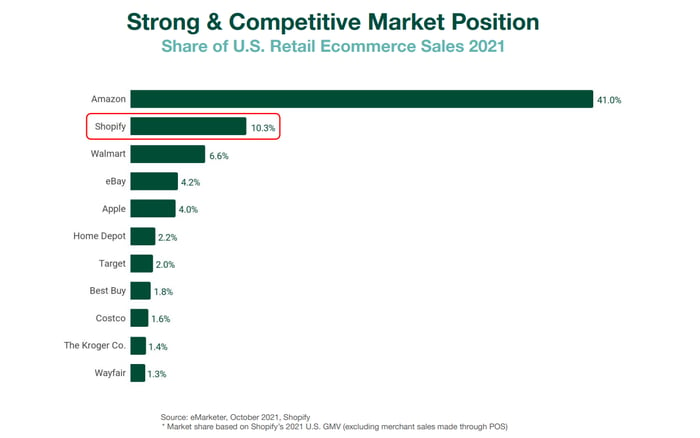

Shopify (SHOP 0.23%) stock has been one of the biggest victims of the tech sell-off -- it has plunged 77% in 2022, as of this writing. Shopify helps anyone from small entrepreneurs to big brands build an online storefront and manage the entire chain of sales from one platform.

Investors fear an economic slowdown amid intensifying competition will hit the e-commerce company hard. Yet for a stock that's already more than 80% off all-time highs and trading at prices last seen in 2019, the fears are more than baked into the stock price.

In fact, Shopify itself expects growth to decelerate. That shouldn't be surprising, as it saw gangbusters growth during the peak of the COVID-19 pandemic, and nearly every company that was in the same boat sees a slowdown now.

What matters is that Shopify is still growing -- its sales grew 22% year over year in the first quarter, backed by a growing merchant base and gross merchandise volumes. In fact, you'd be surprised to know how big some brands have become after tapping e-commerce through Shopify.

Shopify is also investing to not just survive but thrive. For instance, it's acquiring logistics company Deliverr to offer Amazon prime-like next-day and two-day delivery. The move could significantly help Shopify gain market share.

Image source: Shopify's Q4 2021 presentation.

Shopify's revenue shot up to $4.6 billion in 2021 from $1.6 billion in 2019, and it still expects growth this year. Should the stock trade at 2019 price levels for long? I don't think so. Shopify's 10-for-1 stock split is coming up on June 28, but you'll want to invest in the stock for more than just the stock split.

The pessimism in this stock is overdone

Zoom Video Communications (ZM -0.82%) stock has been in a freefall in the past year. Like Shopify, Zoom witnessed supercharged growth during the pandemic. But with workplaces reopening and in-person meetings back in vogue, investors suddenly aren't convinced about Zoom's growth prospects anymore.

Truth is, videoconferencing is a trend that's here to stay, with the global market even expected to grow by double-digit compound annual growth rates in the coming years. Guess who should benefit from all that growth? Zoom, the leader that dominates a whopping 74% of the market, according to Datanyze.

Zoom's showing in the first quarter provides further evidence that videoconferencing is here to stay. Zoom's enterprise customer count rose 24% year over year in Q1, and the number of customers contributing more than $100,000 to the company's revenue in the trailing 12 months jumped 46% year over year.

For the second quarter, Zoom expects revenue to grow 9% at the midpoint, while for the full year, it foresees 10.7% growth in revenue at the midpoint of its guidance range. That may look abysmal compared with Zoom's triple-digit growth rates every quarter through last year, but Zoom's business had to normalize after the hypergrowth over two years, and it's only fair to give the company time and a chance to prove it can still sustain double-digit growth even in a normalized business environment.

For that matter, Zoom expects to grow sales by around 10% this year, but the stock is trading at a price-to-sales ratio of just around 8. Most important, Zoom is a cash-rich business and continues to generate hefty amounts of free cash flow.

ZM Net Income (TTM) data by YCharts

The worst could be over for this red-hot growth stock

Nio (NIO -5.00%) stock launched on the New York Stock Exchange in 2018, but it wasn't until 2020 when the electric vehicle (EV) manufacturer caught Wall Street's attention amid the epic EV stock bull run. Nio shares hit an all-time high of $66.99 a share in January 2021. The stock is 71% off that high as of this writing, despite a solid rebound in recent weeks.

Multiple factors have hit shares of the Chinese EV maker over the past year and a half. While 2021 was governed by the COVID-19 pandemic, fears of a looming financial crisis in China, and tighter U.S. scrutiny on foreign companies, 2022 has mostly been about supply constraints, particularly a severe shortage of semiconductor chips, and surging raw material prices. Rising coronavirus cases in China in recent months delivered another big blow.

Nio, though, remains focused on its growth plans. By 2020, Nio already had three EVs in the market, all SUVs. This year, it started selling its flagship sedan, the ET7. It has also launched a midsize sedan, the ET5, and a mid- to large-size SUV, the ES7, both of which are expected to go on sale in the coming months.

Nio also entered the European market last year and is reportedly also planning to build a plant in the United States. Above all, Nio is working hard to achieve its biggest goal yet -- launching affordable EVs. Nio is already targeting 2024 to start selling a mass-market EV brand, to be priced between $30,000 and $45,000 per car.

Industry experts expect ET5 and ET7 to rule the premium car market in China even as Nio strives to corner a larger part of the Chinese EV market with affordable EVs in the near future. China is the world's largest EV market, and it's pegged to grow by a 25% compound annual growth rate, or more, in the coming years. Nio stock could be a multibagger over the next decade or so, which is why this dip in the stock is a buying opportunity.