The Dow Jones Industrial Average has retreated 16% this year and contains some powerhouse blue-chip stocks that now yield mouthwatering valuations. Some Dow Jones stocks have performed worse than others, but today's worst performers could be tomorrow's best investments. Here are three cheap stocks on the Dow Jones that you should consider seriously.

Apple gets more profitable each year

Warren Buffett started accumulating shares of Apple (AAPL 1.00%) in 2016 and bought more in the first and second quarters of this year as the shares slumped. He regards the company as "probably the best business ... in the world."

Apple commands roughly 50% of the smartphone market in the U.S. and a healthy share of the global market. But it might be the services that iPhone customers add on that keep making the company more profitable every year. For a small fee, iPhone users can download music from the Apple Music app, make contactless payments with Apple Pay, and store their pictures in their iCloud storage.

Image source: Getty Images.

All these add-on services are digital, which means every new customer costs Apple very little. Therefore, every dollar of additional revenue from a new service customer is more profitable than the last. In 2017, when Apple first disclosed the data, its gross margin from services was 55%. That's more than the 35.7% gross margin from products like iPhones, Macs, and iPads. By 2021, the gross margin from Apple's services had vaulted to nearly 70%.

Services gross margin has had a noticeable impact on the overall company. Over the same time frame, Apple's gross margin expanded from 38.5% to 41.8%.

American Express' new customers may surprise you

Buffett's relationship with American Express (AXP 0.25%) goes back even further than his history with Apple. He bought 5% of the company in 1962 for about $20 million when the company was entangled in what would come to be known as "the Salad Oil Scandal." After a few additional purchases and sales throughout the years, the stake is now worth over $23 billion.

These days, American Express is best known as the go-to credit card for folks who like to travel. Its cardholder services include perks like discounts on streaming services, frequent flyer miles, and free-of-charge luxury airport suites for those long layovers. American Express cardholders gush over the company's customer service.

The stock has a couple of things going for it. First, business travel is picking up significantly. Spending is on pace to grow 34% year over year in 2022 to $933 billion. That number is still below 2019's pre-pandemic mark of $1.4 trillion. So, growth potential remains as the world starts to normalize again.

Further, American Express is not your parents' credit card company anymore. Its fastest-growing cohort is millennials, Gen Z, and Gen X. Those customers are at a point in their careers where income and ability to spend will increase for many years.

Nike has a sustainable advantage

Buffett loves the powerful brands that Apple and American Express possess. Although Buffett no longer owns shares of Nike (NKE 0.77%), the company's brand awareness is still right up there with those two Buffett stocks. Nike started building its brand in 1984 when the company signed then NBA rookie Michael Jordan to an endorsement deal. The popularity of the legendary Hall of Famer vaulted Nike into the upper echelon of athletic shoes and apparel.

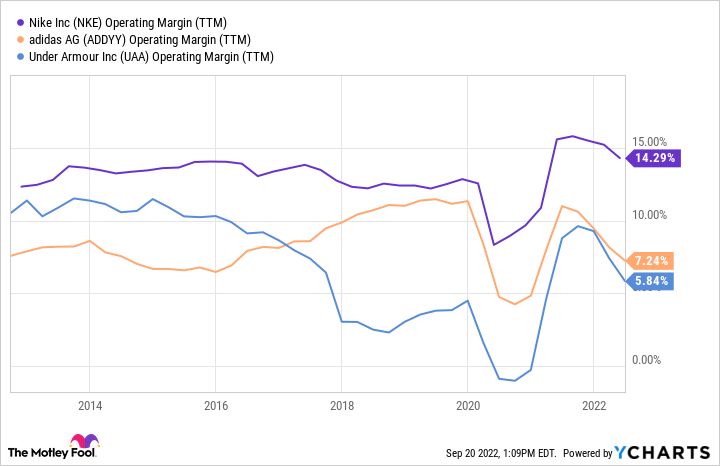

Since then, Nike has repeated the formula for decades by signing other superstars like LeBron James, Kevin Durant, and Cristiano Ronaldo. Nike has grown its empire to a level where competitors like Adidas and Under Armour don't have the resources to sign high-profile stars like Nike can.

The dollars Nike pays for its suite of superstar athletes affords it the luxury of charging extra for its shoes and athletic gear. That extra pricing power makes Nike about twice as profitable as its competitors.

NKE Operating Margin (TTM) data by YCharts

Nike's industry position should allow it to sustain an industry-leading operating margin (revenue minus things like raw materials, advertising, and wages) as long as sports remain one of the world's most popular events. Yet Nike's stock is down 38% this year. Don't be surprised if the Oracle of Omaha scoops up shares of beaten-down Nike stock in the coming quarters.

But are the stocks cheap?

Apple's stock is down about 13% this year and trades at a price-to-earnings ratio of under 26 times. Buffett was a buyer in the first two quarters of the year, and investors have a similar price to Buffett's. If the valuation was good enough for the Oracle of Omaha, it should be good enough for anyone.

American Express stock is also down and now trades at a price-to-earnings ratio of 16 times. That's a 25% discount to its five-year average. With multiple growth levers, in the long run, the shares look cheap.

Nike stock has been the worst performer of the three this year, down 38%. But it might have one of the most sustainable competitive advantages. The stock now trades at a price-to-earnings ratio of 28 times, which is a 40% discount from its five-year average.

If you're a blue chip investor looking for bargains, the Dow Jones is an excellent place to start looking right now. These three stocks offer significant upside for long-term investors. As such, if you're investing for the long haul, you should consider buying these Dow Jones stocks while they're still cheap.