Over the last three years, growth investors have flocked to virtually anything that touches the mere idea of artificial intelligence (AI). Some of the biggest beneficiaries to date of the AI revolution can be found in such sectors as semiconductors, enterprise software, and sustainable energy.

In the past year, however, a new pillar fueling the AI movement has steadily come into focus: quantum computing. Unlike classical computing -- which relies on binary bits -- quantum systems use qubits, which are capable of existing in multiple states at the same time through a property known as superposition. In theory, quantum AI can evaluate sophisticated computations with faster speed and efficiency compared to today's computing standards.

One company that's emerged as a perceived leader in the space is IonQ (IONQ 6.85%), which uses trapped-ion technology to power its quantum architecture. With shares surging nearly 300% over the last 12 months, IonQ is fast approaching a share price of $60.

Could IonQ stock climb even higher, or is it on a dire collision course with history? Let's find out.

Image source: Getty Images.

IonQ's growth looks impressive, but there is a major catch

IonQ's website and investor presentations are packed with blue chip logos and headline-grabbing market size figures. For instance, the company eagerly shows investors that its system integrates with the three largest cloud hyperscalers -- Amazon Web Services (AWS), Microsoft Azure, and Google Cloud Platform (GCP).

While affiliations with some of the largest AI hyperscalers might help create a compelling narrative, the graph below tells a different story.

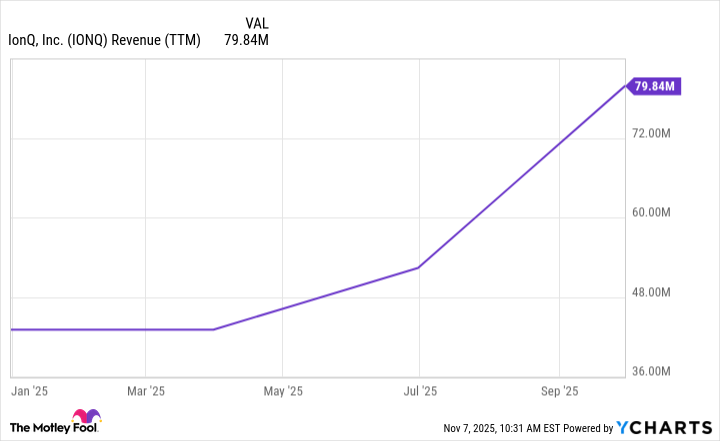

IONQ Revenue (TTM) data by YCharts

Over the last year, IonQ has generated $80 million in sales. While this figure appears to be accelerating, there is a major nuance to point out. Namely, much of this growth is coming from acquisitions -- hence, the slope of the revenue line above is steepening at unprecedented levels.

In other words, IonQ's true organic growth is far less than what is pictured above. These dynamics make it difficult to discern what demand from large enterprises truly looks like for IonQ's quantum technology. In my eyes, IonQ is not building the quantum computing frontier -- it's trying to buy it.

Thorough diligence pays off

Considering IonQ's revenue base primarily relies on growth from acquired assets, you might be wondering how the company is actually funding these transactions. By taking a look at IonQ's balance sheet, you'll notice that the company has $3.5 billion in cash and equivalents. Right off the bat, savvy investors should notice that this figure looks out of place. This is where the cash flow statement becomes our friend.

NYSE: IONQ

Key Data Points

The statement of cash flows begins with net income and subsequently itemizes how a company allocates its capital across operating, investing, and financing activities. Through the nine months ended Sept. 30, IonQ's net loss was $1.3 billion.

How can a company generating less than $100 million in revenue and burning billions of dollars manage to have so much cash at its disposal? The answer is simple: IonQ is performing equity issuances to raise funds. In other words, management is taking advantage of IonQ's rising share price and issuing stock at these elevated levels in order to pad liquidity.

In October, IonQ completed a $2 billion equity issuance. Without these proceeds, IonQ would only have about $346 million in cash and equivalents. This is important to understand because it underscores the idea that IonQ remains unprofitable, and its equity offerings signal that management has not outlined a path to positive unit economics anytime soon. As a result, the company continues to issue stock to raise capital.

Image source: Getty Images.

Are quantum computing stocks in a bubble?

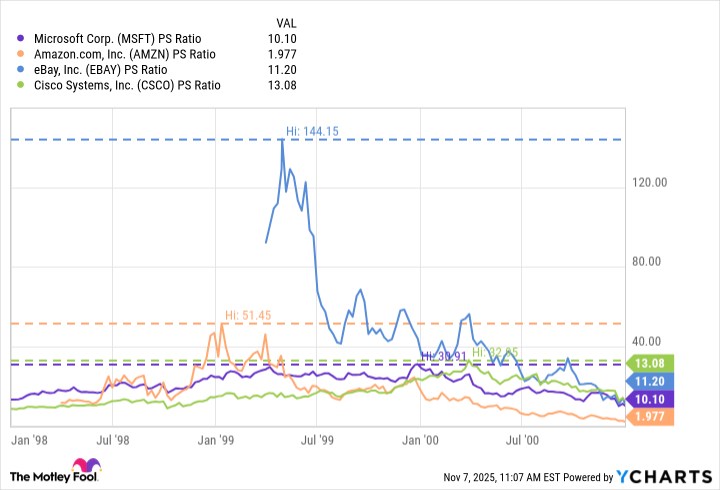

Given that IonQ is unprofitable, a good metric to analyze its valuation is the price-to-sales (P/S) ratio. As of this writing (Nov. 7), IonQ trades at a P/S multiple of 303.

This is more than double what eBay witnessed during the period of dot-com euphoria. Moreover, other early darlings of the Internet -- such as Microsoft, Cisco Systems, and Amazon -- reached peak P/S ratio levels in the range of 30 to 50. In my eyes, quantum computing stocks are a bubble floating next to the broader AI ecosystem -- and IonQ is chief among the most overvalued companies.

Although IonQ stock may climb to $60, the analysis explored here underscores that such a movement will only exaggerate the company's valuation even further. As history shows, valuation multiples eventually normalize as businesses mature. Given IonQ's reliance on the capital markets to fund its operation, I have some doubts about the company's long-term sustainability.

Ultimately, I see IonQ as an instrument for day traders and not a stock worthy of a position in a long-term portfolio looking to build durable wealth.