Artificial intelligence (AI) stocks as a group have been retreating of late, and that seems surprising, considering that the companies benefiting from this technology have been delivering impressive results this earnings season.

However, this is good news for savvy investors. AI adoption is expected to take off in the coming years, thanks to the productivity and efficiency gains that this technology is delivering. According to one estimate, the global AI market is expected to clock an annualized growth rate of 37% through 2031, generating a whopping $1.7 trillion in revenue at the end of that period.

As such, there's reason to believe the recent slump in AI stocks won't last. That's why now would be a good time to take a closer look at two AI names that have taken a beating lately but have been delivering solid results. Both serve fast-growing AI niches that should allow them to sustain their terrific growth in the long run, and that could help them become winning investments.

Image source: Getty Images.

1. SoundHound AI

Voice AI solutions provider SoundHound AI (SOUN +2.03%) is down 36% in the past month. However, analysts are upbeat about the stock's prospects. Among the 10 analysts covering the stock, the median 12-month share price target is $16, 43% above current levels. What's more, seven of those analysts recommend buying SoundHound.

It is easy to see why there is positive sentiment for the stock's prospects. The company has been delivering outstanding growth quarter after quarter, driven by the rapid expansion of the conversational AI market and SoundHound's solid clientele.

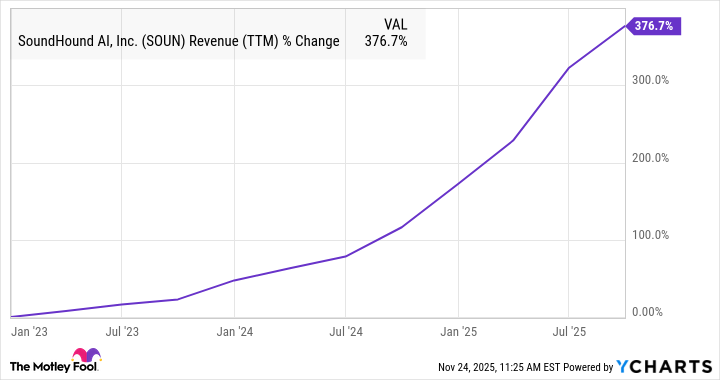

SOUN Revenue (TTM) data by YCharts.

In the third quarter, the company's revenue jumped by 68% from the year-ago period. It also raised its full-year guidance. The midpoint of its new guidance range of $165 million to $180 million would equate to revenue growth of more than 100%. SoundHound, however, is still just scratching the surface of a massive opportunity: It sees a total addressable market (TAM) worth over $140 billion for its voice AI solutions.

The company boasts a diversified base of clients across the automotive, hospitality, restaurant, finance, and insurance industries. As such, there is a good chance that it will be able to achieve faster growth rates than analysts are expecting for the next couple of years.

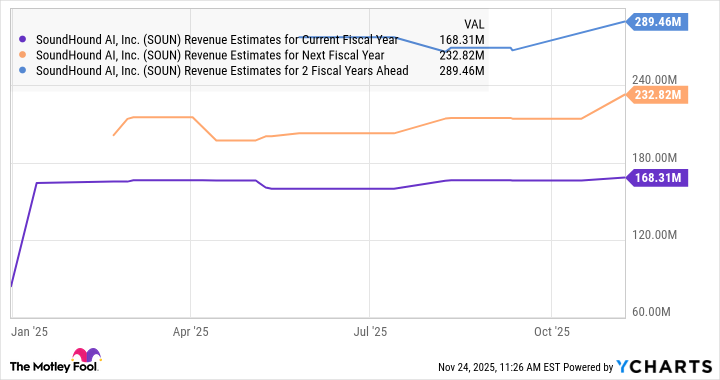

SOUN Revenue Estimates for Current Fiscal Year data by YCharts.

Even after its recent slide, SoundHound AI is trading at 30 times sales. While that's expensive when compared to the U.S. technology sector's average price-to-sales ratio of 8.4, the company's impressive growth rates justify that premium valuation. Moreover, SoundHound's massive revenue backlog of $1.2 billion as of the end of last year puts it in a position to accelerate its growth.

So, investors looking to buy a fast-growing AI stock right now would do well to buy SoundHound. It has the potential to become a much bigger company in the next five years.

2. Vertiv Holdings

While SoundHound AI gives investors an opportunity to capitalize on the growth of the AI software market, Vertiv Holdings (VRT +4.41%) is a play on the hardware side of this technology. The company is in the business of designing, manufacturing, and servicing key digital infrastructure for data centers and communication networks.

NYSE: VRT

Key Data Points

It offers power management solutions such as power distribution systems, uninterruptible power supply (UPS), and solar power systems, among others. Additionally, its thermal management offerings include liquid cooling solutions, heat rejection, and more. Vertiv also sells server racks and enclosures that go into data centers.

The boom in construction of AI data centers has boosted demand for Vertiv's offerings. The company witnessed a 60% year-over-year increase in orders in the third quarter. That was faster than the 29% growth in its top line to $2.7 billion. Vertiv exited the quarter with a backlog of $9.5 billion, up by 30% from a year prior.

The company's book-to-bill ratio of 1.4 last quarter makes it evident that it is receiving orders at a faster pace than it is fulfilling them. This trend is likely to continue in 2026, as Vertiv estimates that the deployment of AI infrastructure in the EMEA (Europe/Middle East/Africa) region will further accelerate next year.

Moreover, Nvidia forecasts that global data center capital expenditures will grow at an annualized pace of 40% through 2030. That gives Vertiv a lot of room to increase its sales, which helps explain why analysts are bullish about its prospects.

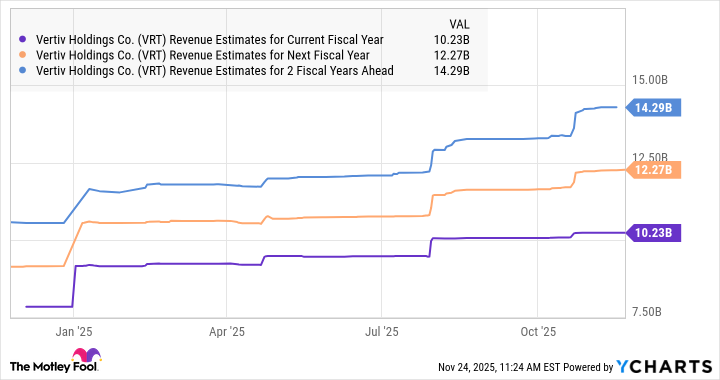

VRT Revenue Estimates for Current Fiscal Year data by YCharts.

Even better, Vertiv has a price/earnings-to-growth ratio (PEG ratio) of 0.83, based on its estimated annual earnings growth rate for the next five years, according to Yahoo! Finance. The standard view is that a company with a positive PEG ratio below 1 is undervalued, so by that measure, Vertiv is trading at a discount. That's why investors should consider buying this AI stock following its 13% pullback over the past month. Its fast-improving backlog and the long-term prospects of the AI data center market should set it up for healthy long-term gains.