PepsiCo (PEP +0.51%) does a brisk business selling not only its namesake cola, but also a formidable collection of drink brands, snacks, and other food items. Its lineup includes such longtime favorites as Lay's, Cheetos, Doritos, and even Quaker Oats.

As stock investors, we are, of course, more concerned with how well the company's equity has performed over time. So grab a Pepsi and let's see how it's done on the market.

Image source: Getty Images.

PepsiCo is a market laggard of late

Well, PepsiCo's run hasn't been that satisfying.

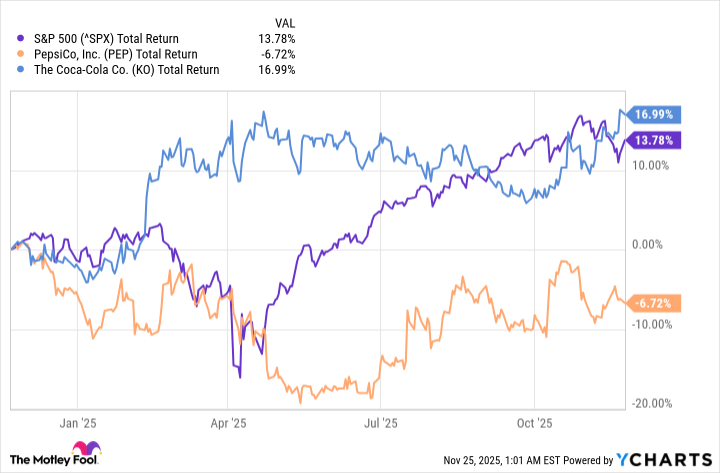

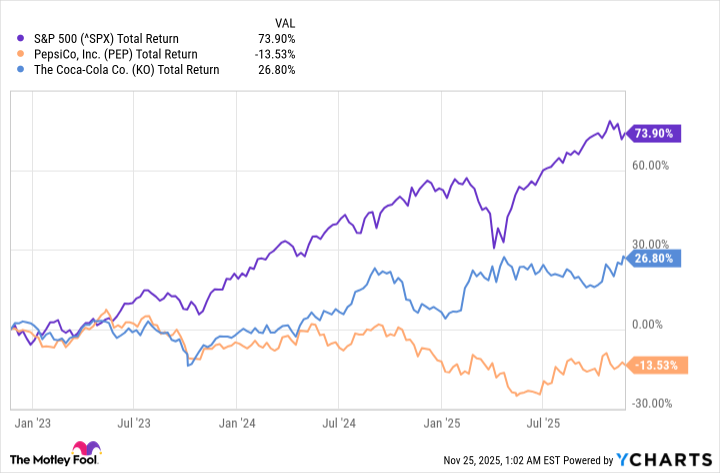

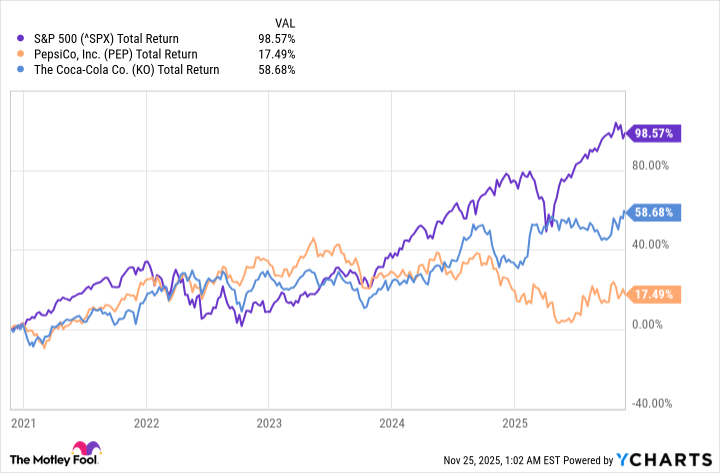

Over the trailing one-year, three-year, and five-year periods, the company's total return has lagged significantly behind the broader stock market, as represented by the S&P 500 index. In all three frames, PepsiCo's return has also been well behind that of Coca-Cola (KO +0.33%), the stock it's often (somewhat inappropriately) compared to.

Data by YCharts.

Why this lack of popularity? Lately, I feel that unimpressive growth in key fundamentals has been a major factor.

After sales jumped during the early stages of the COVID pandemic in 2020, neither sales nor profitability has risen vastly of late. For full-year 2024, the top line crept up by a mere 0.4% over the 2023 figure (to almost $91.9 billion). Net income according to generally accepted accounting principles (GAAP) improved by 6% to nearly $9.6 billion, but this was not enough to wow a large number of investors.

NASDAQ: PEP

Key Data Points

The eternal No. 2?

PepsiCo also suffers from two big top-down negatives, in my view. First, despite the ubiquity of many of its beverage and food brands, it's selling to a world that has become more health-conscious over the years. Doritos, Pepsi, and Lay's potato chips are considered "cheats" even among the least dedicated dieters, and the company hasn't sufficiently expanded its portfolio of healthier alternatives.

Second, it's considered something of a perennial runner-up to Coca-Cola, due to the two companies' ever-battling namesake colas. As mentioned, this isn't entirely accurate, since the latter only concentrates on beverages as opposed to PepsiCo's drinks-and-snacks product mix.

Regardless, Coca-Cola is the better buy on simple share price ($72.59 versus $145.50), certain key valuations (such as its five-year PEG ratio of 2.3 compared to its rival's 5.4), and near-future growth potential.

On average, analysts are modeling a revenue increase of 1.7% for the PepsiCo purveyor this year over 2024, and a slide in per-share GAAP profitability from $8.16 this year to $8.11 in the next. For Coca-Cola, they believe its top-line rise will be 2.9% this year, with earnings per share (EPS) bumping from $2.88 to $2.99.

I've actually been bullish on both companies for some time, so I'll point out here that PepsiCo is consistently profitable at good margins. Plus, its payout is not only very generous at a current yield of 3.9%, but it's also a Dividend King (one of the rare stocks that has raised its dividend annually for at least fifty years straight).

However, that's not sufficient to drive investors into this untrendy title, which, in many respects, compares unfavorably to the monster business considered its top rival. I continue to like PepsiCo as a company, but management needs to find more fizz to move sentiment on the stock.