Right now, all investors want to focus on are growth stocks, especially anything related to artificial intelligence (AI). This is turning attention away from opportunities in value stocks, which investors should take advantage of as the calendar turns to 2026.

One beaten-down stock that is trading at its lowest cash-flow multiple in five years is Crocs (CROX 0.72%). Here's why the eccentric shoe brand may be the best value stock you can buy before 2026.

NASDAQ: CROX

Key Data Points

Declining sales and a reset opportunity

Crocs experienced tremendous growth during the COVID-19 pandemic, spurred by the growing trend of casual wear around the globe. There's no denying that the brand has hit a bit of a rough patch, accelerated by the poor timing around the acquisition of the HeyDude shoe brand.

Revenue for Crocs declined 3% year over year last quarter to $836 million, with HeyDude down 22% to $160 million. Since the middle of 2023, Crocs trailing twelve month revenue -- revenue over the preceding four quarters -- has hovered around $4 billion and is now moving in the wrong direction.

This is the key reason why Crocs stock is in a 56% drawdown. While it would be better if the brand could produce steady growth year after year, investors looking at Crocs today should think of the last few years as a reset after its monstrous growth in the years prior.

What's more, Crocs is doing well outside of North America, which is driving more sales growth. International revenue increased 6% last quarter to $389 million. The Crocs brand is growing globally and has been a mainstay in casual and aquatic apparel in the United States for decades.

Image source: Getty Images.

Returning cash at a discounted valuation

With the stock in a massive drawdown, Crocs now trades at a discounted price, relative to its cash-flow generation. Free cash flow per share is now $12.77 and has been above $10 since 2023. With a stock price of $80, Crocs trades at a trailing price-to-free cash flow ratio (P/FCF) below 7.

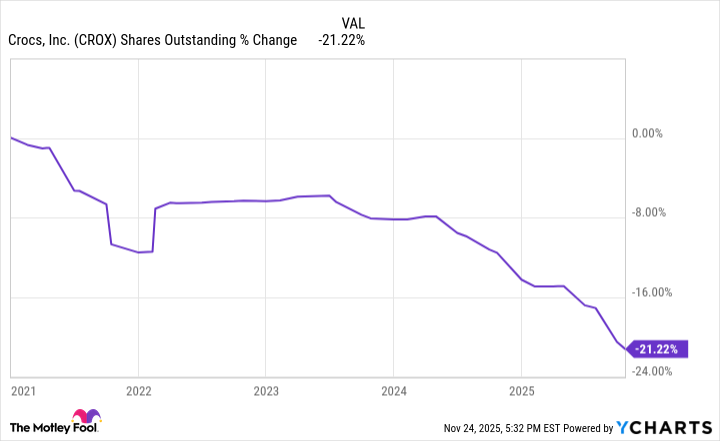

Management is accelerating its share repurchases at these discounted prices, which will benefit long-term growth in free cash flow per share and drive the stock price higher. Shares outstanding have fallen by 20% in the last five years at an accelerating rate. At current stock-price levels, Crocs will be able to further accelerate the pace of the decline of shares outstanding, which any shareholder should applaud.

CROX shares outstanding data by YCharts.

Why Crocs is a great value stock for 2026

Crocs is trading like the business is heading for the dustbin of history at just over 6x its trailing-cash-flow levels. Investors are pricing in many years of declining revenue ahead, similar to the last quarter.

This puts too much doubt on the business and gives no credence to a potential turnaround in fortunes for the eccentric maker of sandals. While the apparel business is never linear, Crocs has proven time and time again that it can stay relevant for consumers in the United States and is now growing across the world.

If Crocs can regain its mojo and begin to grow again, the business will start spitting out growing revenue and free cash flow, and the stock will likely begin to trade at a higher multiple of earnings. If it keeps struggling to grow, then the capital returns program and low starting valuation will provide downside protection.

This is a great opportunity with low downside risk but lots of upside potential for those looking to buy Crocs stock today. Therefore, it's the perfect value play for investors in 2026.