Cyber attacks are on the rise, but those powered by artificial intelligence (AI) pose an especially alarming risk to the corporate sector. In September, leading AI startup Anthropic revealed that its Claude Code tool was used to infiltrate and harvest sensitive data from several large organizations. Pulling off an attack of this magnitude used to require serious manpower, but AI agents are now doing the heavy lifting, turning even the most unsophisticated hackers into serious threats.

Zscaler (ZS 3.28%) is a top cybersecurity vendor, and it's taking a multipronged approach to thwarting cyber risks of all kinds. The company just released its operating results for its fiscal 2026 first quarter (ended Oct. 31), which revealed accelerating revenue growth on the back of soaring demand for its products.

Zscaler stock is still down 31% from its 2021 record high, when it reached an unsustainable valuation during a frenzy in the technology market. However, it could be poised for upside from here, because The Wall Street Journal tracks 50 analysts who cover the stock, and the overwhelming majority have given it a buy rating. Here's why their bullish consensus might be justified.

Image source: Getty Images.

It starts with zero trust

Zscaler continues to launch new cybersecurity products to help enterprises navigate the AI revolution. Its AI-SPM (security posture management) solution, for example, can detect activity from unauthorized AI applications, and it can also limit permissions for AI agents. But looking at the bigger picture, Zscaler's "Zero-Trust Everywhere" approach is what really stops cyberattacks of all kinds from dealing catastrophic consequences.

As the name implies, a zero-trust cybersecurity architecture treats every user as hostile. It starts at the identity layer, where Zscaler's Zero Trust Exchange analyzes not only the user's login credentials, but also their location and their device to determine if it's really them trying to access the corporate network, or if their details have been compromised. This is especially useful in the era of remote work, because not every employee can be physically supervised.

But the Zero Trust Exchange doesn't stop there. It only connects users to the applications they need to complete their jobs, so even if a malicious actor bypasses the identity security layer, they won't have access to the entire network, which minimizes potential damage.

But there is one final piece to Zscaler's Zero Trust Everywhere vision, and it's called Zero Trust Branch, which was launched last year. It runs every retail location, warehouse, factory, and device through the Zero Trust Exchange to isolate it from a cybersecurity perspective. It means even if one of those assets is breached, the attackers can't compromise the rest of the organization. This is critical in the AI era with attack speeds accelerating.

NASDAQ: ZS

Key Data Points

Zscaler's revenue growth just accelerated

Zscaler generated $788 million in total revenue during the fiscal 2026 first quarter, which comfortably exceeded management's forecasted range of $772 million to $774 million. It also represented a 26% year-over-year increase, which was an acceleration from the 21% growth the company produced in the previous quarter three months earlier. It was the fastest revenue jump in a year.

On the back of the strong result, management modestly increased its full-year guidance for fiscal 2026 from $3.275 billion to $3.292 billion, at the midpoint of the respective ranges.

Zscaler also had a strong first quarter at the bottom line. Although the company lost $11.6 million on a generally accepted accounting principles (GAAP) basis, it delivered an adjusted (non-GAAP) net income of $159.5 million after stripping out one-off and non-cash expenses like stock-based compensation. It was a solid 28% increase from its adjusted profit from the year-ago period.

Wall Street is bullish on Zscaler stock

The Wall Street Journal tracks 50 analysts who cover Zscaler stock, and 32 have given it a buy rating. Seven others are in the overweight (bullish) camp, while the remaining 11 recommend holding. None of the analysts recommend selling.

The analysts have a consensus price target of $330.69, implying Zscaler stock could climb by 31% over the next 12 to 18 months. However, the Street-high target of $400 suggests the stock could soar by 59% instead.

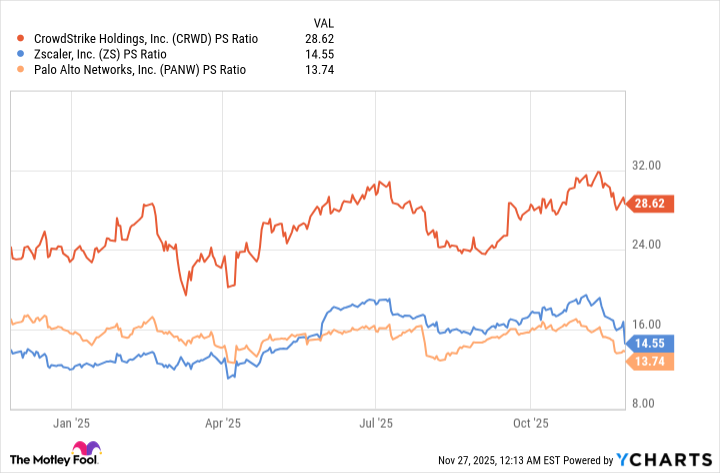

Zscaler stock isn't cheap right now, but it isn't necessarily expensive relative to its peers, either. It's trading at a price-to-sales (P/S) ratio of 14.5 as I write this, which is a slight premium to Palo Alto Networks (PANW 1.26%), but a steep discount to CrowdStrike (CRWD 1.03%). Those two vendors are Zscaler's biggest rivals in the cybersecurity space.

CRWD PS Ratio data by YCharts

If Zscaler continues to grow its revenue at the current pace of over 25% for the rest of fiscal 2026, I think Wall Street's consensus price target of $330.69 is achievable. However, investors who are willing to hold the stock for the long term could reap the biggest rewards, because management believes the company's annual recurring revenue could more than triple to $10 billion in the coming years.