ETFs and mutual funds have a lot in common. However, there are several key differences that could make one a better option for you than the other. In this article, we'll go over the similarities and differences and how to determine which of the two instruments is best for you.

What is an ETF?

What is an ETF?

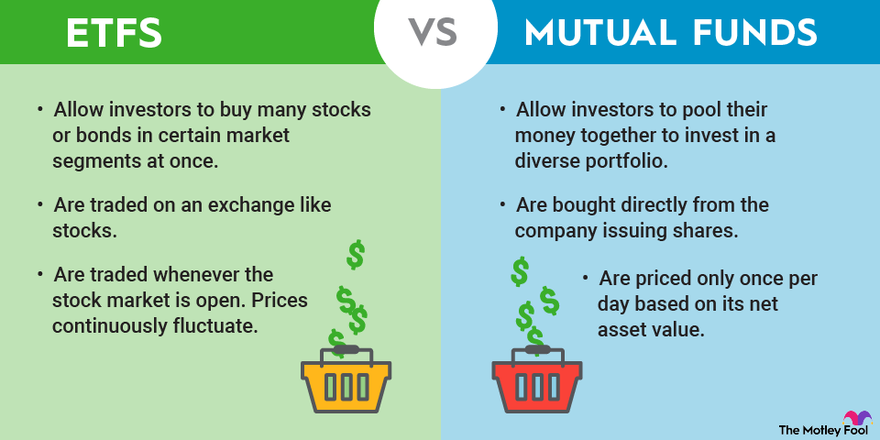

An ETF, or exchange-traded fund, is an investment vehicle that pools money from investors and uses the funds to buy a basket of stocks, bonds, and other securities. Investors can buy and sell shares of an ETF just like they would buy shares of a stock from a stock exchange such as the Nasdaq or the New York Stock Exchange, hence the name exchange-traded fund.

ETFs commonly track a market index or commodity. Those tracking an index are called index funds. However, there is a growing number of actively managed ETFs. An active fund manager tries to outperform a benchmark index by being more selective with their stock picks.

In exchange for the convenience of an ETF, investors pay a fee to the fund company in the form of an expense ratio, or a percentage of assets under management. For heavily traded broad market index funds, where the fund manager's job is relatively simple, the expense ratio can be very low. For actively managed funds, where investors are paying for expert research and allocation management, the expense ratio climbs much higher.

What is a mutual fund?

What is a mutual fund?

A mutual fund is an investment vehicle that pools money from investors to buy a basket of stocks, bonds, and other securities. Investors buy shares of a mutual fund directly from the company issuing shares, such as Vanguard or Fidelity.

Mutual funds are more often actively managed compared to ETFs, but you can also buy mutual funds that track a market index. Again, index funds will generally have lower expense ratios than actively managed mutual funds, and the expense ratios are often identical to their ETF counterparts.

Since you must buy and hold shares of a mutual fund with the fund company issuing the shares, you won't be able to move the assets to another financial institution without selling.

Differences

Differences between an ETF and a mutual fund

The differences between ETFs and mutual funds can have significant implications for investors.

One big difference to consider is how shares of the funds are priced. Since ETFs are bought and sold on a stock exchange, market forces dictate the value of the fund itself. If there's a sizable demand for the fund, it could be priced higher than its net asset value, which is the underlying value of the securities held by the fund.

The opposite is also true. If there's a sudden rush to sell shares of that specific fund, it could be priced below the net asset value. That's usually not an issue for most ETFs with high liquidity.

By comparison, mutual funds are always priced at their net asset value at the close of every trading day.

Another important consideration is tax efficiency. ETFs are usually more tax-efficient than mutual funds because ETF shares are traded on an exchange instead of redeemed with the mutual fund company, so there's a buyer for every seller. That might not be the case with a mutual fund, and a lot of sellers will cause the mutual fund company to sell shares of the underlying securities. That will have capital gains tax implications for all shareholders regardless of whether they sell.

Other differences -- such as the ability to buy fractional shares, commission fees, and minimum investments -- will vary based on the funds and brokers you're considering. Some mutual funds have very low minimums, and they'll go down further if you agree to invest on a regular schedule. Many online brokers have reduced their standard commission to $0 and allow investors to purchase fractional shares, so you're not leaving cash on the sidelines.

You can easily reinvest dividends from mutual funds just by checking a box, but the ability to reinvest dividends from an ETF will depend on whether your broker offers a dividend reinvestment plan for your preferred fund.

Related investing Topics

Which is right for you?

Which is right for you?

Understanding the differences between ETFs and mutual funds can help you decide which is best for you.

Use ETFs if:

- Tax efficiency is important to you. If you're investing in a taxable brokerage account, having more control over capital gains distributions may be a deciding factor. If you're investing in a tax-advantaged retirement account, tax efficiency is a moot point.

- You're an active trader. You like to set limit orders and stop-limit orders or use margin in your investing strategies. These options are available because ETFs trade just like stocks, but you can't use these strategies with mutual funds.

- You want to gain low-cost exposure to a specific market niche without researching individual companies. A lot of ETF options benchmark niche market indexes. While you could gain exposure through mutual funds, they're often less tax-efficient or rely on active management, increasing their costs.

- You may change brokers in the future. ETFs are easily transferred between brokers, but you typically must close mutual fund positions before changing brokers. You would then have to reinvest the proceeds into mutual funds offered by your new broker.

Use mutual funds if:

- A comparable ETF you're considering is thinly traded. Limited liquidity for an ETF could result in large bid/ask spreads, often requiring you to pay a premium above the fund's net asset value. Mutual funds are always priced at net asset value.

- You value the potential to outperform the market through active management. While actively managed ETFs exist, they're few and far between. Most ETFs are index funds, which simply match the market return. To outperform an index, you need active management. Keep in mind, however, that these funds typically have higher fees and higher tax implications -- and you're not guaranteed outperformance even with active management.

- You're investing in less-efficient parts of the market. Actively managed funds have the best potential to outperform in these areas. Highly traded markets such as large-cap U.S. stocks are very efficient, but sectors with less trading volume have much more potential to benefit from active management research and strategy.