A recession refers to a period of declining GDP and is generally defined as a sustained decline for two or more consecutive quarters.

Recessions aren't just about poor economic growth. They are often accompanied by several other characteristics -- widespread job losses, fewer available jobs, and more government relief (think stimulus payments and increased unemployment benefits).

With all that in mind, you may wonder if investing is a good idea if we're in a recession or are headed in that direction. Is it wiser to take every dollar you make and keep it in cash?

Is it safe to invest during a recession?

During a recession, stock values often decline. In theory, that's bad news for an existing portfolio, yet leaving investments alone means not locking in recession-related losses by selling.

What's more, lower stock values offer a solid opportunity to invest on the cheap (relatively speaking). As such, investing during a recession can be a good idea but only under the following circumstances:

- You have plenty of emergency savings. You should always aim to have enough money in the bank to cover three to six months' of living expenses, with the latter end of that range being more ideal. If you're there and have extra money at your disposal, you can feel free to invest it. If not, be sure to build a solid emergency fund first.

- You're not planning to touch your portfolio for at least seven years. Investing during a recession isn't for the faint of heart. You may think you're buying at a low, only to see your portfolio value decline a few days later. The best way to avoid losses in a recession -- and come out ahead -- is to take a long-term approach to investing. Plan on leaving your money alone for at least seven years.

- You're not going to obsessively check your portfolio. When the economy is in bad shape and there's lots of stock market movement, you may be more inclined to log on to your brokerage account every day and see how your portfolio is doing. But, if you're going to invest during a recession, you simply can't do that. The more you check up on your investments, the more likely you are to panic. And, when you panic, you risk making rash decisions, such as unloading poorly performing stocks, that force you to lock in losses.

It can be a great idea to invest during a recession -- but only if you're in a strong enough financial position to do so and only if you have the right attitude and approach. You should never compromise your near-term financial security for long-term gain. Remember that if you're hurting financially, there's no shame in missing out on opportunities. Instead, focus on paying your bills and staying physically and mentally healthy. You can always ramp up your investments at a later point in life -- once your job is more secure, your earnings are steady, and your mind is more at ease on the whole.

Real-world results of investing in recessions

Long-term investors who put money to work during a recession have done pretty well over time. Looking at data from three recent recessions prior to the COVID-19 pandemic -- the Great Recession from 2007-2009, the recession in 2001 fueled by the dot-com crash and the 9/11 attacks, and the 1990-91 recession that followed a long economic expansion in the 1980s -- you might be surprised at the long-term results, even if investors' timing wasn't perfect.

If you invest at the market's lowest point during a recession, you're likely going to do quite well over time. But one thing investors should realize is that trying to time the market is almost always a losing battle. There's no crystal ball that can tell you when the market will bottom. In other words, you are not going to invest at the absolutely perfect time.

But you don't have to. Even if you had invested in an S&P 500 index fund at the worst possible moment in 2007 -- the market's peak before the financial crisis began -- you would have achieved an 8.4% annualized return in the 13 years since. If you had bought at the highs before the 1990-91 recession, you would have achieved a 9.8% annualized return in the nearly 30 years since.

Consider what this means. If you had invested $10,000 in a standard S&P 500 index fund at the worst possible time during the 1990-91 recession, your investment would have grown to more than $150,000 in value today, assuming dividends were reinvested along the way.

What to invest in during a recession

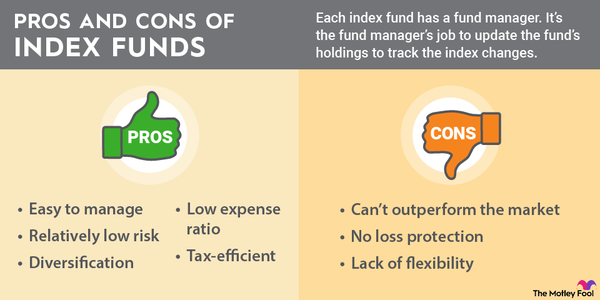

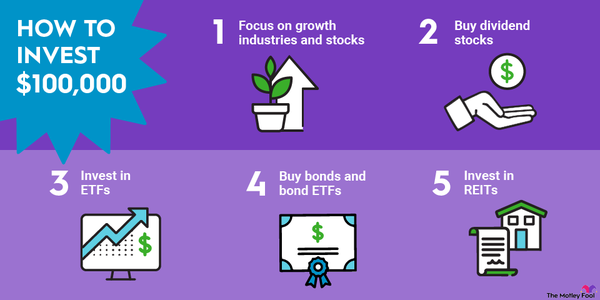

In the last section, we mentioned index funds, and those can be a great way to invest -- recession or not. By purchasing index funds -- especially S&P 500 index funds -- you're betting on the long-term success of U.S. business. Over long periods of time, that's been a pretty solid bet.

However, we completely understand that many people reading this prefer to invest in individual stocks. The best investment strategy in any environment is to find good businesses and hold on to them for as long as they remain good businesses, but this focus on quality is especially important in a recession.

As an example, during the COVID-19 pandemic and subsequent recession, companies in affected industries that had stronger balance sheets going into the crisis had an advantage over those that didn't. Companies with the financial flexibility to survive a long disruption started to look like excellent long-term investment opportunities, while companies with otherwise good businesses but low liquidity were among the hardest-hit stocks, and some didn't survive.

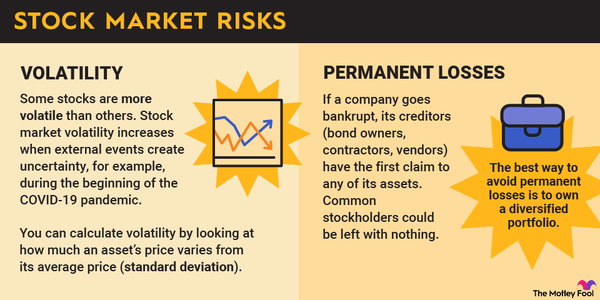

In a recession, how you invest can be just as important as what you invest in. In recessions, stocks tend to be rather volatile, as anyone who was involved in the market during the 2008-09 financial crisis can tell you.

Rather than trying to time the market, invest incrementally. Known as dollar-cost averaging, this strategy refers to investing equal dollar amounts at certain time intervals as opposed to buying all at once. This way, if prices continue to fall, you can take advantage and buy more. And, if prices start to rise, you'll end up buying more shares at the lower prices and fewer shares when your favorite stocks start to get more expensive.

In a nutshell, a recession can be a great time to buy the stocks of top-notch businesses at favorable prices.

What not to invest in during a recession

A recession is a good time to avoid speculating, especially on stocks that have taken the worst beating. Weaker companies often go bankrupt during recessions, and while stocks that have fallen by 80%, 90%, or even more might seem like bargains, they are usually cheap for a reason. Just remember -- a broken business at an excellent price is still a broken business.

That said, the most important thing isn't necessarily what not to invest in but what behaviors to avoid. Specifically:

- Don't try to time the bottom. As previously mentioned, trying to time the market is a losing battle. Wouldn't it have been great if you had invested as much as you possibly could on March 9, 2009, when the S&P 500 was at the lowest levels of the financial crisis? Sure, but it would also be great if you knew tomorrow's lottery numbers ahead of time. Nobody knows when the market is going to hit bottom, so invest in stocks or funds you want to hold for years, even if the market continues to fall in the near term.

- Don't try to day trade. These days, it's easier than ever to start casually trading stocks, thanks to zero-commission stock trades and user-friendly trading apps. If you want to mess around with a small amount of money you're OK with losing, that's fine. But long-term investing is a far more certain path to wealth in the stock market. Day trading as an investment strategy is generally a bad idea.

- Don't sell just because your stocks went down. Last, but certainly not least, one thing that's extremely important to avoid during recessions is panic selling when stocks fall. It's human nature to avoid volatile situations -- when the stock market is in free fall, you might be tempted to sell "before things get any worse." Don't give in to your emotions. The goal of investing is to buy low and sell high, but panic selling is the exact opposite.

Related investing topics

Investing in a recession

The bottom line is that, during recessions, it's important to stay the course. It becomes a bit more important to focus on top-quality companies in turbulent times, but, for the most part, you should approach investing in a recession in the same manner you would approach investing any other time. Buy high-quality companies or funds and hold on to them for as long as they stay that way.