If you really want to have your financial house in order, you need to know how to prepare for a recession. A recession is a normal part of the economic cycle. The United States has experienced 11 recessions since the end of World War II. But they don't occur regularly, usually coming as a bit of a surprise.

Understanding economic recessions and what you can do to prepare for one will help you get through a challenging economic environment and potential financial distress.

Understanding recessions and why they happen

Understanding recessions and why they happen

A recession, plainly speaking, is a downturn in economic activity. While many cite two consecutive quarters of negative growth in gross domestic product, or GDP, that's not the official definition of a recession.

A recession is determined by the National Bureau of Economic Research (NBER), which prefers to look at the economy as a whole. The NBER includes data such as domestic production, unemployment rates, labor participation, manufacturing and wholesale trade, and inflation.

Gross Domestic Product (GDP)

A coinciding of a number of unpredictable and hard-to-prevent factors usually leads to a recession. A war could break out, for example, leading to supply chain disruptions. Inflation could push the Federal Reserve Board to raise interest rates to purposely slow the economy. Interest rates could be a major factor in a recession.

If a central bank maintains extremely low interest rates, it makes debt much more attractive. People buy bigger houses and more expensive cars. Businesses take on more risk, taking advantage of the low rates to expand quickly. But when businesses fail, this results in layoffs, home foreclosures, and car repossessions, and we find ourselves in a recession.

Interest Rate

There's no timeline for how long a recession lasts. The pandemic-related recession in 2020 went on for just two months, but the Great Recession lasted 18 months, from December 2007 until June 2009. Let's look at 10 ways to prepare for a recession.

1. Preparing for a Recession: Tips 1-5

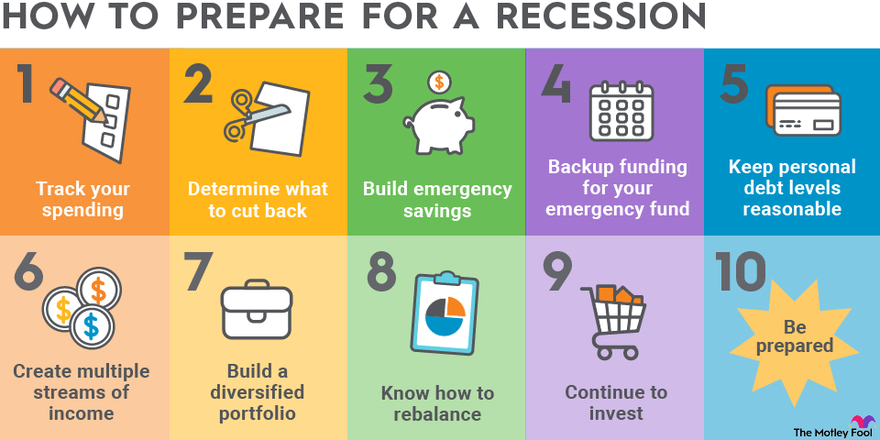

1. Track your spending

This isn't about making a budget; it's about seeing where your hard-earned money goes. When you track your spending, you'll get a rough idea of just how much your life costs as it is today. Knowing how much you spend in an average month is great, but knowing how much you spend in an average year is even better.

Knowing how much you spend is a great starting place for any financial plan. And if you want to be prepared for a recession, which could include a disruption in your income, you need to know how much you're spending.

Many apps (free and paid) can help you track your spending. You can also dig into your credit card statements and make a spreadsheet. You don't have to be extremely detailed. Keep things broad until you need more information than you're currently tracking.

2. Determine what you can cut back

You probably don't need to cut back now, but what would you stop spending on if you lost your job or your income dropped? This is why tracking your spending is so crucial.

If you know how much you spend on necessities (e.g., housing, groceries) and how much on nonessentials (e.g., dining out, entertainment), you can start making a plan in case of a financial emergency. Determining what you can cut from your budget now will make things easier if or when you have to do it.

3. Build emergency savings

Once you've determined your bare-bones budget, you can plan for your emergency savings. Most experts recommend three to six months' worth of expenses in your emergency fund. If you're self-employed and the only source of income in your household, you may want a bigger emergency fund.

You can base your emergency fund on your bare-bones budget. You won't be eating at restaurants or traveling much when you're spending down your emergency fund. So several months of bare-bones expenses should be enough to survive a job loss in a recession.

4. Have backup funding for your emergency fund

It never hurts to have a backup plan. If we enter a prolonged recession and you can't find work for some time and eventually deplete your emergency fund, you'll want to know what to do next. Doing a little prep work now could set you up with a better backup plan than just trying to figure things out on the fly.

If you have a substantial stock portfolio, you may plan on selling some assets to make ends meet in a prolonged recession. This is far from ideal, of course, because stock values crash in a recession. That said, it's way better than being unable to pay your bills, and sometimes, it's the best option available.

Another option is to set up a line of credit. That might be a home equity line of credit, a personal line of credit, or even a credit card. Setting up lines of credit will be easier while employed, so you can do that now. There may be fees to set up a line of credit, but it won't incur interest unless used.

5. Maintain reasonable personal debt levels

Maintaining low debt levels means you won't have to worry about paying off debt in the middle of a recession. Consistently carrying debt balances means one more bill payment to worry about. Paying down high-interest debts while you have a steady income will make it easier to stay afloat if you lose your income or it's cut.

Moreover, paying down debt might allow you to qualify for better rates and bigger credit lines on a home equity line of credit (HELOC) or personal line of credit. Your credit score is heavily affected by your percentage of total credit in use, or credit utilization. Access to a big line of low-interest credit can be a key source of backup funding for an emergency if it reaches a point where you need to use debt.

Preparing for a Recession: Tips 6-10

6. Create multiple streams of income

One of the best ways to protect yourself from losing income during a recession is to have multiple income streams. In a dual-income household, you're more protected than if you're going it alone. But even if you're a solo act, you can build multiple income streams. For example, you can create a side hustle or buy income-producing assets such as rental properties.

While there's no guarantee either of those will hold up in a recession, having multiple sources of income is better protection against a recession than relying on a single source for all your income.

7. Build a diversified portfolio

Markets typically sell off during a recession; a diversified portfolio will help protect your investments. Portfolio diversification doesn't just mean owning many different stocks. You want your stock investments spread across various sectors; some will get hit worse than others in a recession.

A diversified portfolio also includes multiple asset classes with uncorrelated price changes. Better yet, finding assets with negative price correlation will help smooth the ride. Stock and bond prices have historically moved in opposite directions, but not always. Investing in multiple asset classes, such as real estate, commodities, metals, and international markets, may be a better way to ensure your portfolio holds up in a recession.

8. Know how to rebalance

Your portfolio will get out of balance in a recession; it's best to know how to put it back on track. If you establish a diversified portfolio with target asset allocations, you want to keep your portfolio around those levels.

One way to rebalance is to establish bounds on the percentage of your portfolio allotted to each asset. When assets exceed those bounds, you'll have to sell some and buy others. Opportunities to rebalance are likely to pop up during a recession. Equity values usually decline, which should push you to sell other assets to buy more stocks and rebalance the portfolio.

9. Continue to invest as long as you can afford to do so

You should continue investing in the markets as long as you remain employed. Even if you fear a recession is approaching or that we're already in one, it's best to keep buying. Trying to time the market is much more likely to cause you stress than to generate outsized returns.

Maintaining the habit of saving and investing every paycheck will help protect your budget and give you a greater basket of assets you can draw from in case your emergency fund runs out.

10. Be prepared to lose your wits

Losing a job or watching your portfolio value decline can cause anyone to lose their mind. If you have a plan for dealing with a sudden layoff or what to do if the value of your stocks falls 20%, 30%, or 50%, you'll be prepared to act when you're reeling from the loss.

But be aware that sticking to the plan may feel uncomfortable. The emotional side of your brain can get in the way of the rational side. Preparing for the emotional impact of events that could befall you during a recession is hard. But if you have a plan in place, it will be easier to deal with those feelings of uncertainty.

Related recession topics

Stay ahead of the next recession

Recessions are an inevitable part of the economic cycle. If you understand what can cause a recession and how to prepare for one, you'll be on solid enough financial footing to withstand almost anything the economy throws your way.

Recession-preparation FAQs

Recession-preparation FAQs

What's the best thing to do in a recession?

If you developed a plan for managing your finances in a recession, you should try your best to stick to that plan. Emotions can get in the way as uncertainty creeps into your mind, but trust and execute your plan. Batten down the hatches on your budget, use your emergency fund if needed, and rebalance your portfolio.

What should you not do in a recession?

Don't panic. Recessions are a normal part of the economic cycle. There's no need to sell every investment you've made, and you don't need to turn your life upside down worrying about your financial future.

Follow the guidelines above to help you create a plan to prepare for a recession. And while your emotions may try to distract you from following the plan, do your best to execute it.

What thrives during a recession?

Industries that do well in a recession are those that benefit when consumers start cutting back on purchasing. Grocery stores can benefit when fewer people are going out to eat, and discount retailers benefit as shoppers look to save money.

Defensive industries tend to hold up well, too. Healthcare, utilities, defense, and consumer staples can all support a portfolio when a recession causes the values of growth stocks to decline.