As the digital economy continues to expand, the use of digital currency is also increasing rapidly. Digital currency is money in an electronic form exchanged for goods and services without the use of physical money such as paper bills or coins.

Technology is growing and evolving. As a result, digital currency is steadily replacing physical money. Here's what you need to know about the types of digital currencies and the advantages and disadvantages of digital currency.

What is a digital currency?

What is a digital currency?

As technology advances, so does digital currency. An early form of digital money was the electronic exchange of cash between bank accounts or an electronic payment utilizing credit. This still takes place (mostly by debit or credit card) with bank-to-bank electronic wires, an online payment system, or the use of a smartphone that carries a user's payment information.

Digital money today mostly facilitates the movement of fiat currency -- money issued and backed by a government such as the U.S. dollar, the Canadian dollar, or the euro. But digital currency now also includes cryptocurrencies. Bitcoin (BTC -0.92%) is the original cryptocurrency and was privately developed as a means of exchange on the internet.

Since its creation in 2009, Bitcoin has been accepted by some investors as a store of value (an asset that can be saved for later with the reasonable belief it will not depreciate in value). After Bitcoin, thousands of cryptocurrencies were developed for various uses in the digital economy and the real world.

Many governments that issue fiat currency are also considering developing their own digital currency as a variant of the traditional money they already create.

What makes a digital currency

What makes a digital currency

Money in digital form (such as dollars sitting in your bank account) is a type of digital currency, but it isn't the same as cryptocurrency. The reason is that money in digital form can be converted into physical cash (for example, via an ATM) when making a withdrawal. Traditional money in its digital form can be used to facilitate electronic payments by card at physical merchants and online, but there are some differences between it and money built as an actual digital currency.

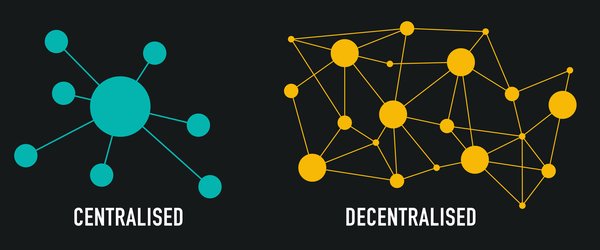

Money in its current form -- including digital forms of cash on deposit at the bank -- is created and distributed by a central bank Think of the U.S. dollar, which is printed by the U.S. Treasury and distributed by the Federal Reserve. In a centralized process, a system of serial numbers is usually used to make sure each note is unique. Bank partners are used to distribute cash into the economy.

A digital currency such as cryptocurrencies, however, makes use of an electronic ledger system to create a network of computing nodes to process transactions. Cryptography is often used to make user identities and transaction details anonymous. A digital currency can also bypass bank and financial institution intermediaries and be provided directly to users.

The IRS defines digital currency as a "virtual currency" if it "functions as a medium of exchange, a unit of account, and/or a store of value." The IRS defines Bitcoin as a type of "convertible virtual currency" since it can be easily exchanged for U.S. dollars. In this context, virtual currency purchases and sales will trigger taxable events, per the IRS.

Types of digital currencies

Types of digital currencies

There are currently three basic types of digital currencies in development or circulation:

Central bank digital currencies: A growing list of money-issuing governments are considering issuing digital versions of their fiat currencies, known as central bank digital currencies (CBDC).

For example, China is testing its digital renminbi (e-CNY) to facilitate cross-border payments and circumvent existing digital payment channels. Chinese e-commerce giant JD.com (JD 2.08%) started accepting e-CNY payments from customers in late 2021. The U.S. Federal Reserve is also studying digital currency and working on a plan for its own CBDC. Other countries, such as Switzerland, continue to study the impact of CBDCs on the economy but currently have no plan to implement them.

Cryptocurrencies: Cryptocurrencies are developed by private parties independent from a central bank or government institution. Cryptos make use of blockchain technology, a digital ledger system that records crypto transactions. Most cryptocurrencies also use cryptography to make the digital currency tamper-resistant and the network more secure.

The two largest cryptocurrencies are Bitcoin and Ethereum (ETH -0.1%). A growing list of companies are either working on blockchain and crypto development or using cryptocurrencies in their operations. Unlike CBDCs, cryptocurrencies are decentralized, meaning there is no single party responsible for issuing or changing the currency.

Stablecoins: Stablecoins are a type of cryptocurrency and make use of blockchain technology and cryptography. The key difference between stablecoins and traditional cryptocurrencies, however, is that stablecoins are backed by a reserve asset such as the U.S. dollar or gold, and they're designed not to fluctuate in value like traditional cryptos. They will instead track the value of the asset that backs them.

Tether (USDT -0.02%) is currently one of the largest stablecoins. Meta Platforms (NASDAQ:FB) (formerly Facebook) was also developing a stablecoin project called Diem, but it recently sold the crypto assets to bank Silvergate Capital (NYSE:SI), which intends to launch its own stablecoin sometime in 2022.

Advantages and disadvantages of digital currency

Advantages and disadvantages of digital currency

As with all technology, digital currencies solve some of the problems associated with traditional money. There are also concerns and drawbacks.

Pros of digital currencies

- Digital currency speeds transaction times. The modern financial infrastructure is made up of a complex web of participants. In some instances, like with a fully decentralized digital ledger system, two parties can transact business directly without any bank or financial institution intermediaries. That avoids payment settlement times that can traditionally take days or even weeks.

- Digital currency can reduce costs. With the elimination of some or all intermediaries, transaction fees associated with digital payments can be greatly reduced. This is especially the case with the high costs associated with the cross-border movement of money.

- Physical money has security issues. Risk of theft, forgery, and the need for physical storage at a bank can be reduced or eliminated with digital currency.

- Some digital currencies (such as cryptocurrencies) aim to decentralize monetary policy and can include people in the distribution of currency previously handled by a central bank's financial institution partners.

- Digital currency technology automates accounting and other recordkeeping, saving time and expenses for issuers, merchants, and everyday users.

Cons of digital currencies

- Since it is a computing technology, digital currency is not immune to hacking and other cybercrimes. If an economy adopted digital currency, financial stability and national security could become a cybersecurity risk.

- Cash is anonymous, but digital transactions can be tracked. While most digital currencies seek to anonymize user identity, transactions leave a trail.

- Digital currency reduces traditional transaction costs, but it carries its own unique set of expenses. Cybersecurity costs are one. Many cryptocurrency users, for example, choose to store their digital assets in a crypto wallet, a piece of hardware that can be disconnected from the internet (known as cold storage). Blockchain-based payments also have to pay fees associated with the computing transactions.

- Digital currency presents new challenges for regulators and policymakers trying to ensure financial stability.

Future of digital currency

Future of digital currency

Digital currencies are still in the early days of development. Cryptocurrency values have skyrocketed in recent years as various companies have expressed interest in building new services and products with them, and investors have increasingly viewed cryptos as an investment asset class. Central banks that create and back fiat currency may also alter the landscape if they begin issuing their own digital currencies.

The future for digital currencies and other digital assets utilizing them is in flux, but the steady expansion of technology bodes well for the proliferation of electronic forms of money and payment. It's possible to invest in this development via cryptocurrencies, stablecoins, and company stocks involved in their creation and use, so it's an exciting realm for investors to explore. Just remember to stay diversified and focused on the long term if you choose to invest in the digital currency movement.