Investing in bonds can be a great way to earn extra money with a more secure investment than the stock market often provides, but it’s not without risk. Understanding concepts like yield to worst can help you make the best decisions when buying bonds.

Bonds

Understanding yield to worst

Understanding yield to worst

On some bonds, your yield is calculated based on the maturity date, but not all operate this way. Other bonds can be cashed in earlier by their issuer if circumstances favor it. When this happens, it can be unexpected, but you can account for the potential event by basing your investment strategy on the yield to worst.

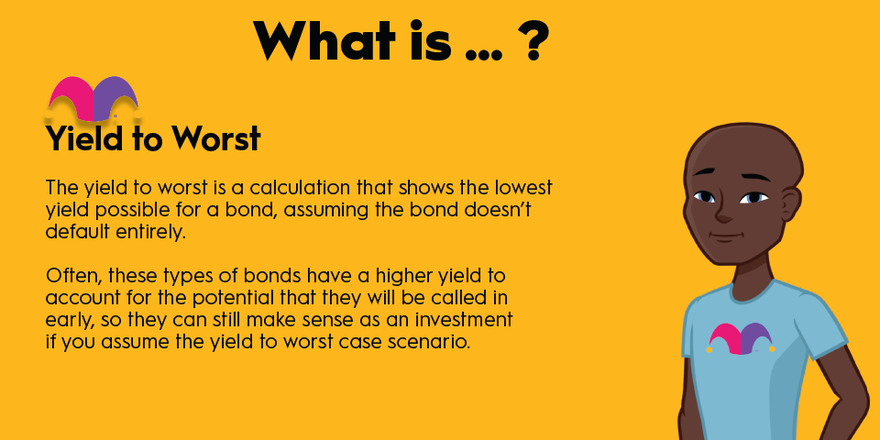

The yield to worst is a calculation that shows the lowest yield possible for a bond, assuming the bond doesn’t default entirely. Often, these types of bonds have a higher yield to account for the potential that they will be called in early, so they can still make sense as an investment if you assume the yield to worst case scenario.

What type of bonds are affected?

What type of bonds are affected?

Bonds that should have the yield to worst calculated are bonds that are callable, meaning they have a provision written into the agreement that allows the issuer to pay them back early. When they’re paid back early, you lose out on a certain amount of interest payments, so it’s important to read the fine print very carefully.

There are three main types of callable bonds:

- Optional redemption. These bonds have a feature that allows the issuer to redeem the bonds after a certain period.

- Sinking fund redemption. With a sinking fund redemption, the issuer is required to regularly redeem a portion of the bonds (as much as 100%) on a fixed schedule.

- Extraordinary redemption. Provides an option for the issuer to call its bonds before the maturity date if specific events occur. This might happen if the project that the bonds are financing is seriously damaged or destroyed.

Why are bonds called in?

Why are bonds called in?

Most of the time, bonds are called in because it makes more financial sense for the issuer to do so than to continue to pay high interest on them to bond holders. They don’t necessarily fully repay the project that was financed with the bonds, but may instead refinance it with a bond issue at a much lower interest rate. This happens mostly when bond rates are falling and an issuer still has many high-rate bonds outstanding.

Interest Rate

However, bonds can also be called in during extraordinary circumstances that might pause, change, or end a bond-funded project. There are other reasons bonds are called in, as well. Sometimes, the bonds were always meant to be paid down in steps, rather than on a single maturity date.

How to calculate the YTW

How to calculate the YTW

For some bonds, the yield to worst is the same as the yield to maturity, but on callable bonds, it may be the same as the yield to call. It’s always the lowest of either the yield to call or yield to maturity. These formulas are below:

YTC = ( coupon interest payment + ( call price - market value ) / number of years until call) / (( call price + market value ) / 2 )

YTM = ( coupon interest payment + (( face value - present value ) / years to maturity ) / (( face value - present value ) / 2 )

Simply choose the worst outcome and that’s the yield to worst. Pretty simple, but it’s important to note that you don’t have to do this for zero-coupon bonds, since you’re not looking to account for missed interest payments.