Chances are good that no matter what type of investor you are, you've heard the term "short sale." For some, it represents an opportunity to move forward with their lives despite a high mortgage, and for others, an opportunity to make some extra money on their investments.

Two types of short sales

Two types of short sales

There are two very distinct types of short sales: one involving mortgages and one involving stocks. They both involve an asset that's being sold for less than is expected, but short-selling stocks is generally done to gain a profit, and short-selling a home is done to help a distressed homeowner get out from under a crushing mortgage debt.

Both can have huge impacts on your financial future when deployed strategically and can be devastating to your financial life when approached without a great deal of planning and thought.

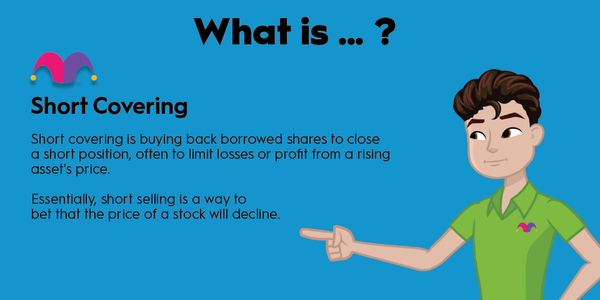

How does short selling work in stocks?

How does short selling work in stocks?

When it comes to stocks or other securities, short-selling is a way to make a tidy profit when planned well. An investor borrows stocks or other tradable securities that they believe will decrease in value from a brokerage or other party willing to loan them (typically for a small fee). There's a time limit on how long they can borrow those stocks before they must be returned or purchased.

Generally, what happens in a stock short sale is that the borrower will put the stocks up for sale immediately, hoping that the price will drop substantially. If the price does drop, they will buy the stocks back and return them to the owners, pocketing the difference between the initial sale price and the buyback price.

So, for example, if I borrowed 10 shares of XYZ, Inc. from my broker when they were worth $50 a share with the intention to short, I'd turn around and immediately put them up for sale. The magic happens when that stock drops in value, say to $35. I have to buy the stock back to return it by the deadline, but now I'm only paying $350 to buy those shares, and I get to put $150 in my pocket (This is a very simplified example).

What is a short sale in real estate?

What is a short sale in real estate?

A short sale in real estate is something very different and happens when a distressed borrower is allowed to sell their home for less than they owe on it. This doesn't happen often in the kind of market we're currently experiencing, but when markets drop suddenly, you can see it quite a lot. It was a common practice during the Great Recession.

The homeowner has to get permission from the lender to sell their home short, but it is often in the lender's best interest to do so because it can be expensive to go through the entire process that's required to repossess a home and prepare it for sale. This way, the bank only loses the difference between the loan and the cash at closing, some of which may be able to be made up by the mortgage insurance (if any) on the shorted mortgage.

In some cases, the borrower will have to pay back the difference between their loan and the sale price, but it depends on the rules in the state where the sale happens, and this is considered at the bank's discretion.

Related investing topics

Real estate short sales versus foreclosure

Real estate short sales versus foreclosure

Both short sales and foreclosures are difficult times for many homeowners since they occur when they're in financial distress. However, they have very different effects on a homeowner's ability to recover financially. Both will eventually fall off your credit if you satisfy any outstanding debt that may be associated with them.

However, a short sale shows a potential future lender that you were attempting to do right by the bank that loaned you your mortgage; a foreclosure reflects poorly on your willingness to communicate your need with the bank. Because foreclosure is more expensive and difficult legally, banks are less likely to loan to you again in the short term, but a short sale is looked at far more favorably when it comes to applying for a new mortgage.

You won't be looked at exactly the same as a squeaky-clean borrower, but it's still better than having a foreclosure on your record.