If you have a big expense coming up, but you're a little short on cash, you may be considering taking a loan from your 403(b) account. Many 403(b) plans include a loan provision, which allows retirement savers temporary access to their funds. But there are a few important details you need to know to determine whether a 403(b) loan is your best option.

What is a 403(b) loan?

A 403(b) loan is much different from a loan you might get from a bank. There's no credit check, and the loan terms can be quite favorable compared to those of a personal line of credit, a cash advance on your credit cards, or even a secured line of credit such as a HELOC.

In essence, you're just withdrawing funds from your 403(b) with the intention of putting them back over time. As long as you pay the money back on schedule, you won't incur the taxes and fees associated with early withdrawals.

Each plan has different terms for its loan option, so it's important to review the details with your plan administrator. But the mechanics of 403(b) loans all work the same and require the same considerations.

How does a 403(b) loan work?

When you decide to take a loan from your 403(b), you'll need to talk to your plan administrator and sign a loan agreement. The loan agreement should detail the terms of the loan -- how much interest you'll pay and how long you'll have to pay back the loan.

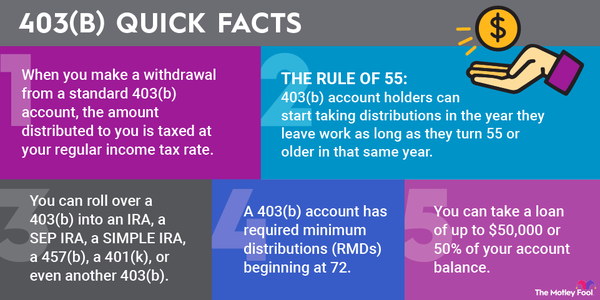

The IRS puts a limit on how much you can loan yourself. The IRS limits the amount to 50% of your vested account balance or $50,000, whichever is smaller. If you have less than $10,000 in your account, the IRS permits you to take the full balance as a loan. Certain plans may have stricter limits.

The IRS also stipulates that the loan must be repaid in equal payments occurring at least quarterly, and that it must be repaid in full within five years. Again, individual plans may have stricter rules.

Once you've taken your withdrawal, you can use the cash for whatever you need. In the meantime, you should be enrolled to make regular loan repayments from your paycheck equal to the minimum payment required to meet the terms of the loan agreement.

Unlike regular contributions to your 403(b), loan repayments do not count toward your contribution limits. The contribution limit for 2024 is $23,000 ($22,500 in 2023), or $30,500 if you're older than 50 ($30,000 in 2023). Furthermore, the interest portion of the loan payment is paid with after-tax dollars, whereas regular contributions are typically pre-tax dollars.

If you have the cash to repay the loan early, you can talk to the plan administrator about creating a payoff statement to pay the remaining balance.

What to consider before taking out a 403(b) loan

There are quite a few considerations when you're taking out a loan from your retirement plan.

While there's no real net interest cost since you're paying yourself the interest, there's still a real cost to taking the loan from your savings -- the returns you'd get from keeping the funds invested.

The S&P 500 averages more than 9% returns per year over five-year periods, but there's a wide range of possibilities. It's impossible to know what the market will do over the life of the loan, but it's more likely to increase than decrease, creating a cost to your loan. If you can get a personal loan with a relatively low interest rate, it's likely a better option than taking a loan from your 401(k).

Furthermore, there are tax implications to consider. The interest you pay yourself into your 403(b) account is treated as after-tax money. That means you pay taxes on it now, and you'll have to pay taxes on it again on withdrawal if you're using a traditional pre-tax 403(b) account.

If your 403(b) plan offers a designated Roth account and you can take your loan withdrawal exclusively from that Roth account, you'll avoid the double taxation on your interest payment. You'll pay tax on the payment but no tax upon withdrawal.

The biggest risk is that of failure to repay. If you lose your job, you'll be asked to repay the entire balance of the loan all at once. If you can't come up with the money, the balance will be treated as a distribution subject to early withdrawal penalties and taxes. So that "loan" could end up costing you a lot more than a more traditional one.

Be sure to consider all the above factors when looking at the 403(b) loan option. As with most financial options, there are advantages and disadvantages, and the deciding factors often boil down to individual circumstances.