Self-employed workers often have a lot more freedom than their traditionally employed counterparts, but they face unique challenges, too. One of the biggest is the lack of an employer-sponsored retirement account.

When you're self-employed, the burden of saving enough rests entirely on your shoulders, but a solo 401(k) can make meeting that challenge a little easier. It's similar to a traditional 401(k), but it's designed specifically for the self-employed. Here's what you need to know about it.

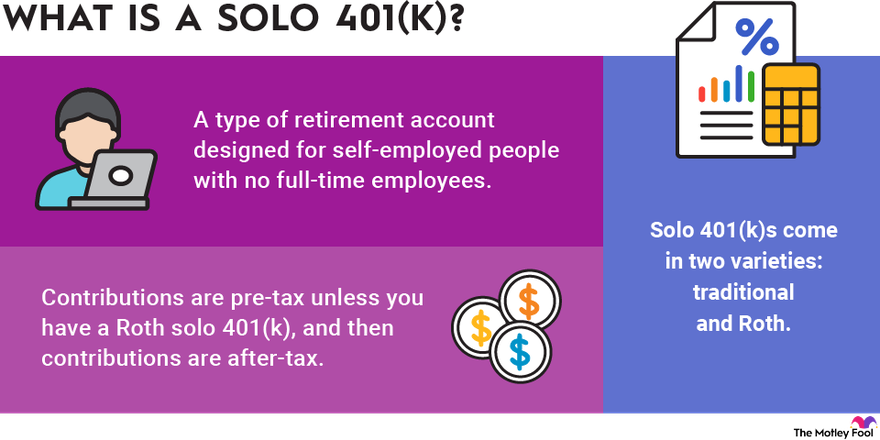

What is a solo 401(k)?

What is a solo 401(k)?

A solo 401(k), sometimes known as an individual 401(k), is a type of retirement account designed for self-employed people with no full-time employees. There is an exception if your spouse works for your business. In that case, both of you may contribute to a solo 401(k).

It works similarly to a 401(k) a traditional worker might be offered through their job, but because self-employed people act as both employee and employer, they can contribute larger sums each year.

At a glance

Solo 401(k) at a glance

| Eligibility | Contribution Limits | Taxes |

|---|---|---|

| Self-employed or small business owner with no employees | $66,000 (2023) and $69,000 (2024). Those 50 or older can contribute up to $73,500 (2023) and $76,500 (2024). | Contributions are pre-tax unless you have a Roth solo 401(k), and then contributions are after-tax. |

Benefits

Benefits of a solo 401(k)

One advantage of a solo 401(k) is the opportunity to choose the type of plan and the investment options that work best for you. Traditionally employed workers are limited to what their company offers, which might not be what's best for their money. When you're the boss, you select how you're going to invest your funds based on your risk tolerance. You also get to decide which type of 401(k) provides you with the best tax advantages.

Solo 401(k)s come in two varieties: traditional and Roth. Traditional solo 401(k)s are tax-deferred. You make contributions with pre-tax dollars, and these reduce your taxable income for the year. But then you must pay taxes on your solo 401(k) distributions in retirement. It's a smart play for those who think they're earning more money right now than they'll be spending annually in retirement. Delaying taxes until your income is lower will help you hold on to more of your hard-earned money.

Roth solo 401(k)s work the other way. You pay taxes on your contributions this year, but the money grows tax-free afterward. When you withdraw the funds in retirement, you get to keep it all for yourself. This is a better choice for those who think they're earning about the same as or less than what they expect to spend annually in retirement. In this case, paying taxes now will cost you a smaller percentage of your income than waiting.

In exchange for these tax benefits, the government usually doesn't allow you to withdraw your solo 401(k) funds before age 59 1/2 unless you use the money for a qualifying exception such as a first home purchase or a large medical expense. You can withdraw Roth solo 401(k) contributions at any time, however, as long as you've had the account for at least five years. But withdrawing money without a qualifying reason before age 59 1/2 results in a 10% early withdrawal penalty.

Contribution limits

Contribution limits for a solo 401(k)

Self-employed workers may contribute up to $66,000 to a solo 401(k) in 2023, or $73,500 if age 50 or older. The 2024 limits are $69,000, or $76,500 if you're 50 or older.

These limits are a lot higher than what traditional employees can contribute to a 401(k) because self-employed workers can make employer contributions as well.

The 401(k) employee contribution limit for traditionally employed workers is $22,500 in 2023, and $23,000 in 2024. If you're 50 or older, you can contribute up to $30,000 in 2023, and $30,500 in 2024.

The employer contribution is up to 25% of an employee's contribution, or about 20% of your net self-employment income, which is defined as all your self-employment earnings minus business expenses, half your self-employment tax, and the money you contributed to your solo 401(k) for your employee contribution. For example, if you earned $100,000 in net self-employment income, you could make an employer contribution of up to around $20,000 to your solo 401(k).

Your maximum contribution is the lesser of the annual contribution limit (discussed above), or up to $22,500 of your compensation in 2023, and $23,000 in 2024, plus 25% of your compensation from your employer-side contribution. If you're 50 or older, you can contribute an additional $7,500 in both 2023 and 2024. If you're younger than 50, you cannot contribute more than $66,000 in 2023 or $69,000 in 2024, even if your employer contribution would allow for it. You can't exceed your maximum employee and employer contributions for the year even if you haven't hit the annual limit.

How to start a solo 401(k)

How to start a solo 401(k)

Follow these steps if you're interested in opening up a solo 401(k):

- Get an Employer Identification Number (EIN): You need an EIN to open a solo 401(k). You can apply for one of these on the IRS website.

- Choose your broker: Explore different brokerages and look into their investment offerings, their fees, and their customer service.

- Fill out the appropriate paperwork: Your broker will send you a plan adoption agreement and an application to fill out before you can put money into your account.

- Fund your account: You may put money into your solo 401(k) by sending a check or using direct deposit to fund the account.

Once you've done these four things, you can start choosing your investments and making regular contributions to your account. You can also roll over funds from other retirement accounts in your name if you choose.

You must make your solo 401(k) employee contributions by Dec. 31, but you have until the tax filing deadline for the year -- usually April 15 of the following year -- to make your employer contribution.

One last thing to note is that if you have $250,000 or more in your solo 401(k) by the end of the year, you're required to submit a Form 5500-EZ information return to the IRS with your taxes for that year so you don't run into trouble with the federal government.

Solo 401(k) vs. other plans

Solo 401(k) versus other retirement plans

If you don’t think a solo 401(k) is a good fit for you, here are some other options you may want to consider:

- Simplified Employee Pension (SEP) IRA: A SEP IRA is another popular option among self-employed individuals with no employees. You may contribute up to the lesser of $66,000 in 2023 and $69,000 in 2024, or 25% of your net income. You can use one of these accounts if you have employees, too, although you’ll have to make mandatory contributions to your employees’ accounts. This could limit how much you can afford to contribute to your own retirement.

- Traditional or Roth IRA: Traditional IRAs and Roth IRAs are open to all workers, even those who aren’t self-employed. You can open them with most brokers, and you’re free to choose from many common investments. You may contribute up to $6,500 in 2023, or $7,000 in 2024. If you're 50 or older, you can contribute an extra $1,000 in both 2023 and 2024.

- Self-directed IRA: Self-directed IRAs are traditional, Roth, or SEP IRAs that allow you to invest your money in real estate and other assets you can’t typically invest in with an IRA.

Each account has its pros and cons, so you’ll have to decide which is best for you. A SEP IRA might be a better fit if you don’t want to deal with the more complex reporting requirements of a solo 401(k). But solo 401(k)s let you choose between tax-deferred and Roth accounts and take out loans, while SEP IRAs don’t allow these things.

If you can’t decide on a single type of retirement account, you could always consider more than one. For example, a Roth IRA could be a smart complement to a tax-deferred solo 401(k) if you want to set aside some extra money above and beyond what the solo 401(k) allows.

Just make sure you understand the rules associated with the various accounts you use, particularly their contribution limits, so you don’t have problems with the IRS. You also need to keep in mind when you’ll owe taxes on the funds in each account so you know how to plan your withdrawals in retirement.

A solo 401(k) is definitely worth considering, especially if you don’t have any employees and you’d like to set aside a lot of cash for retirement. But if you don’t think it’s the right fit for you, there are plenty of other options out there. Focus on what makes the most sense for you right now. If that changes down the road, you can always do a rollover later on.