Borrowing money from a retirement plan may be tempting: It's already your money, you don't have to get approval, and you won't owe a creditor.

While some retirement plans, such as a 401(k), do offer loan options, an IRA does not.

The good news is that you can sometimes find a workaround to temporarily access your IRA money for short-term cash needs by conducting an "indirect rollover." However, there are risks to this method, and it isn't always an option.

Why borrowing can be better than withdrawing retirement funds

Why borrowing can be better than withdrawing retirement funds

First things first: Borrowing from a retirement plan is often a better option than making a straight withdrawal from your account when you need money. There are two reasons for this:

- You won't get hit with the early withdrawal penalty that normally applies when you take money out of traditional tax-advantaged retirement accounts before age 59 1/2.

- You won't permanently lose the invested funds and their potential for gains. When you withdraw money, you lose out on the compound interest, and your retirement account balance will ultimately be smaller. If you borrow instead of permanently withdrawing, you'll put the money back in your account where it can work for you.

However, while borrowing can be better than withdrawing funds, you won't always have that option -- especially with an IRA.

Indirect rollovers allow you to take a short-term loan from your IRA

Indirect rollovers allow you to take a short-term loan from your IRA

While you cannot take a loan from your IRA, you can make an indirect rollover.

IRA rollovers are common. For example, you might close out one retirement account and roll your funds directly into a new one with lower fees or better service. Your money is rolled over from one account directly to another.

By contrast, an "indirect rollover" occurs when you receive a check for the value of your IRA and are then responsible for depositing it into a new IRA within 60 days. If you stick to that window, you won't be hit with an early withdrawal penalty. And that's where the option to borrow from an IRA comes into play.

If you need money and know you'll be able to pay it back within 60 days, you can initiate a rollover, use that money temporarily, and then pay it back to avoid a penalty. Bonus: You don't even have to deposit the funds into a new IRA; you can stick them right back into your existing IRA.

Now, this strategy is not without risk. If you don't deposit the money back into an IRA within that 60-day time frame, the amount removed will be treated as a distribution, which means it will be subject to a 10% early withdrawal penalty. But if your need for money is very short term (say you're self-employed, have a huge bill to cover, and are awaiting a payment for a major project that's coming within a month), using an indirect IRA rollover as a loan could work.

However, you're limited to one IRA rollover annually, so you can use this trick only once per year.

When you can withdraw money without penalty

When you can withdraw money without penalty

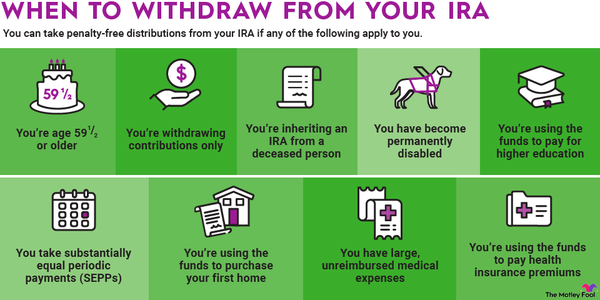

Since you can't take a loan from your IRA, you may consider withdrawing money instead. Be aware that if you take money out of your IRA, you will be taxed at your ordinary income tax rate unless it is a qualified withdrawal from a Roth IRA. You may also be subject to a 10% early withdrawal penalty unless:

- You're at least 59 1/2

- You meet the IRS definition of disabled

- You're taking Substantially Equal Periodic Payments

- You're withdrawing up to $10,000 toward the purchase of a first home

- You're paying medical expenses that exceed a certain percentage of gross income

- You're unemployed and using the money to pay medical insurance premiums

- You're paying past-due taxes because you're subject to an IRS levy

- You're covering eligible higher-education expenses

If you have a Roth IRA, you are always permitted to withdraw the money you've invested (your "contributions") without incurring penalties; penalties would apply only to the early distribution of gains.

Consider a 401(k) loan

Consider a 401(k) loan

Although you cannot borrow from your IRA, it's generally possible to borrow from your 401(k) -- depending on your 401(k) plan's rules. Normally, you may borrow up to $50,000, or 50% of your vested account balance.

Before borrowing or withdrawing from a 401(k) or IRA, however, you should carefully consider the risk to your retirement security and explore other available options.