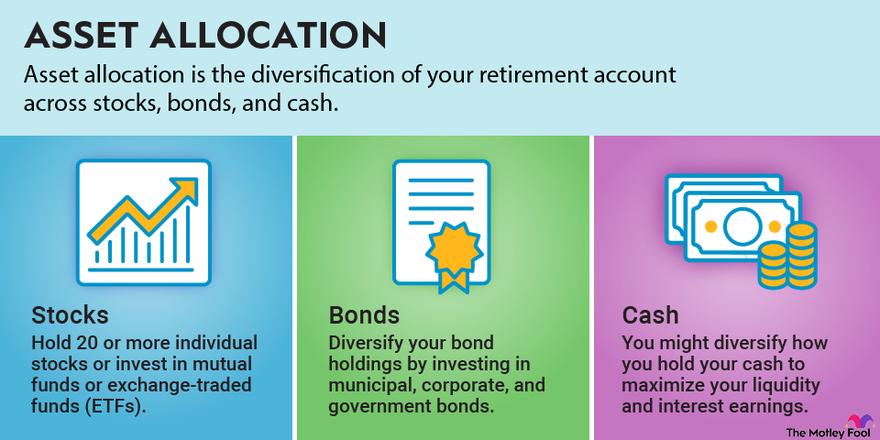

Asset allocation is the diversification of your retirement account across stocks, bonds, and cash. Your age is a primary consideration when you're managing allocation because the older you are, the less investment risk you can afford to take. As you get closer to retirement age, your risk tolerance decreases dramatically, and you can't afford any wild swings in the stock market.

Asset

Save those wild rides for the amusement park. You can increase your wealth and meet your retirement goals by following these five best practices for managing your asset allocation.

1. Asset allocation by age

1. Adjust your asset allocation according to your age

When your investment timeline is short, market corrections are especially problematic -- both emotionally and financially. Emotionally, your stress level spikes because you had plans to use that money soon, and now some of it is gone. You might even get spooked and sell. And financially, selling your stocks at the bottom of the market locks in your losses and puts you at risk of missing the stocks' potential recovery.

Adjusting your allocation according to your age helps you to bypass those problems. For example:

- You can consider investing heavily in stocks if you're younger than 50 and saving for retirement. You have plenty of years until you retire and can ride out any current market turbulence.

- As you reach your 50s, consider allocating 60% of your portfolio to stocks and 40% to bonds. Adjust those numbers according to your risk tolerance. If risk makes you nervous, decrease the stock percentage and increase the bond percentage.

- Once you're retired, you may prefer a more conservative allocation of 50% in stocks and 50% in bonds. Again, adjust this ratio based on your risk tolerance.

- Hold any money you'll need within the next five years in cash or investment-grade bonds with varying maturity dates.

- Keep your emergency fund entirely in cash. As is the nature of emergencies, you may need access to this money with just a moment's notice.

2. Risk tolerance

2. Consider your innate risk tolerance, not just your age

You may have heard of age-based asset allocation guidelines like the Rule of 100 and Rule of 110. The Rule of 100 determines the percentage of stocks you should hold by subtracting your age from 100. If you are 60, for example, the Rule of 100 advises holding 40% of your portfolio in stocks.

The Rule of 110 evolved from the Rule of 100 because people are generally living longer. It works the same way, but you subtract your age from 110 instead of 100.

These rules attempt to determine your ideal asset allocation solely by your age. But your age and how much time remains until you retire aren't the only factors in play. Your innate risk tolerance can be just as important. Ultimately, diversification across asset classes should provide you with peace of mind, regardless of how old you are.

If you're 65 or older, already collecting benefits from Social Security and seasoned enough to stay cool through market cycles, then go ahead and buy more stocks. If you're 25 and every market correction strikes fear into your heart, then aim for a 50/50 split between stocks and bonds. You won't achieve the highest possible returns, but you will sleep better at night.

3. Stock market conditions

3. Don't let stock market conditions dictate your allocation strategy

When the economy is performing well, it's tempting to believe that the stock market will continue to rise forever, and that belief may encourage you to chase higher profits by holding more stocks. This is a mistake. Follow a planned asset allocation strategy precisely because you can't time the market and don't know when a correction is coming. If you let market conditions influence your allocation strategy, then you're not actually following a strategy.

4. Diversification

4. Diversify your holdings within each asset class

Diversifying across stocks, bonds, and cash is important, but you should also diversify within these asset classes. Here are some ways to do that:

Stocks:

Hold 20 or more individual stocks or invest in mutual funds or exchange-traded funds (ETFs). You can diversify your stock holdings by individual company and market sector. Utility companies, consumer staples, and healthcare companies tend to be more stable, while the technology and financial sectors are more reactive to economic cycles. Mutual funds and ETFs are already diversified, which makes them an attractive option when you are working with small dollar amounts.

Bonds:

Diversify your bond holdings by investing in bond funds. Or, vary your holdings across bond maturities, sectors, and types. The different types of bonds available are primarily municipal, corporate, and government bonds.

Cash:

Cash doesn't lose value like a stock or bond can, so diversifying your cash holdings doesn't necessarily need to be a priority. If you have lots of cash, you might hold it in separate banks so that all of it is FDIC-insured. (The FDIC limit is $250,000 per depositor per bank.) But most people aren't sitting on tons of cash. More realistically, you might diversify how you hold your cash to maximize your liquidity and interest earnings. For example, you could hold some cash in a liquid savings account and the rest in a less-liquid certificate of deposit (CD) with a higher interest rate than a typical savings account.

5. Target-date funds

5. Invest in a target-date fund that manages asset allocation for you

If you're nodding off just reading about asset allocation, there is another option. You could invest in a target-date fund, which manages asset allocation for you. A target-date fund is a mutual fund that holds multiple asset classes and gradually moves toward a more conservative allocation as the target date approaches. The target date is referenced in the fund's name and denotes the year that you plan to retire. A 2055 fund, for example, is designed for folks who plan to retire in 2055.

Target-date funds generally follow allocation best practices. They're diversified across and within asset classes, and the allocation takes your age into account. These funds are also easy to own. You personally don't have to actively manage your allocation or even hold any other assets -- except for the cash in your emergency fund.

Even so, there are drawbacks. Target-date funds don't account for your individual risk tolerance or the possibility that your circumstances may change. You might get a big promotion that enables you to retire five years earlier, for example. In that case, you'd want to review the allocations in your portfolio and decide if they still make sense for you.

Related retirement topics

Make (and follow) your own rules, too

No single approach to asset allocation addresses every scenario perfectly. Carefully consider your risk tolerance and when you plan to retire to establish an approach that works for you. You could also wing it -- but make sure that your seat belt is firmly buckled because it could be a wild ride.