The Roth individual retirement account, or IRA, is a versatile retirement plan that confers multiple benefits. You can use your Roth IRA to fund a home down payment and higher-education expenses, for example. But the plan's tax benefits are, to many investors, its most compelling feature. Contributing to a Roth IRA enables the account's earnings to grow on a tax-deferred basis, withdrawals in retirement are tax-free, and there are no required minimum distributions (RMDs).

Here's a closer look at the many advantages of contributing to a Roth IRA.

Biggest advantages of Roth IRAs

Biggest advantages of Roth IRAs

The contributions you make to a Roth IRA are not tax-deductible in the current year. While that may sound like a drawback, it's actually not. Some of the Roth IRA's best features are allowed specifically because this type of plan only accepts after-tax contributions.

Here's one feature that's sure to spark your interest: Since Roth IRAs are funded with after-tax dollars, you can withdraw your contributions at any time without paying a penalty or additional tax. To be clear, this applies to your contributions only, not the earnings on those contributions.

The earnings in your Roth IRA do have some restrictions. These earnings are tax-deferred, meaning any tax that may be assessed is deferred until you make a withdrawal. Not having to withdraw money annually to pay taxes on capital gains earned by the securities in the account enables the value of the Roth IRA to increase more rapidly. Even better, when you reach retirement age, your Roth IRA withdrawals of both earnings and contributions are tax-free.

A Roth IRA can also help you to buy a home or earn a college degree. You may withdraw earnings from a Roth IRA prior to reaching retirement age if you use the money to pay for qualified education expenses or a down payment on your first home. When you access your Roth IRA to buy a home, you may withdraw up to $10,000 in earnings without paying a penalty, plus any amount of your contributions.

Finally, the funds in your Roth IRA are not subject to required minimum distributions, which are annual withdrawals required by the U.S. Internal Revenue Service (IRS) for some types of retirement plans. With Roth IRAs, if you don't need the funds to pay your bills, you can leave your account intact. Provided that your funds stay invested, the account can continue to grow.

Tax benefits of Roth IRAs

Tax benefits of Roth IRAs

The most immediate tax benefit of a Roth IRA is the tax-free growth of your contributions. Although Roth IRAs have contribution limits, you can receive an unlimited amount of dividends, interest, and realized capital gains without increasing your tax liability for the current year. This tax treatment enables your Roth IRA to grow at an attractive rate because you don't have to withdraw money every year to pay taxes to the IRS.

Once you reach age 59 1/2, and five years have passed since you first contributed to your Roth IRA, you may withdraw funds tax-free. A stream of tax-free income simplifies your budgeting in retirement, and there's another advantage, too. The IRS assesses what portion of your Social Security benefits is taxable based on your combined income, which equals half of your annual Social Security income, plus any other taxable income and any nontaxable interest.

You may be taxed on up to 50% of your Social Security income if your combined income is between $25,000 and $34,000 as a single taxpayer, or between $32,000 and $44,000 as a married couple filing jointly. If your combined income exceeds $34,000 as a single tax filer, or $44,000 as a jointly filing married couple, then the IRS may tax up to 85% of your Social Security benefit.

Roth IRA withdrawals, since they are not taxable in retirement, don't count toward your combined income. Investing enough money in your Roth IRA to receive, say, $100,000 annually, would limit your combined income to be just half of your Social Security benefit, provided that you don't also have other sources of taxable income or nontaxable interest. Receiving funds only from a Roth IRA in retirement could mean that you don't owe any federal taxes at all on your Social Security payments.

A Roth IRA can also indirectly spare you from paying income taxes because you don't have to take RMDs from this type of account. For retirement accounts with taxable distributions, the IRS requires RMDs after you turn 73. Those mandated withdrawals, by being considered as taxable income, could increase the portion of your Social Security benefit that is taxed. Your RMDs may also be large enough to push your income into a higher tax bracket. Since no RMDs are required for Roth IRAs, your money can stay in your account until you need it.

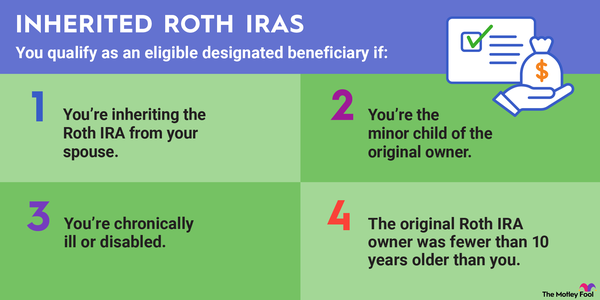

You can even hold a Roth IRA long enough to bequeath it to your heirs. Withdrawals by the new beneficiaries would be tax-free provided that the Roth IRA has been open for at least five years. The beneficiaries would only need to withdraw all the funds from their inherited Roth IRA within 10 years of your death. That provides another decade during which the account can grow tax-free and potentially substantially increase in value.

Benefits of Roth IRAs for young adults

Benefits of Roth IRAs for young adults

Roth IRAs are well suited for young adults who are early in their working careers. There are three main reasons why.

First, having a relatively low income maximizes the tax advantages of a Roth IRA. Remember that you contribute to a Roth IRA with after-tax dollars. You pay taxes in the current tax year on the amount of this year's contribution instead of being taxed on the withdrawals in retirement. This arrangement is advantageous because your tax bracket when you first start working is likely lower than your tax bracket later in life.

Second, you are more likely to not exceed the Roth IRA income limits when you're just starting your career. In 2023, you may not contribute directly to a Roth IRA if your modified adjusted gross income is more than $153,000 for a single filer, or $228,000 for married taxpayers filing jointly. In 2024, these income limits increase to $161,000 and $240,000, respectively.

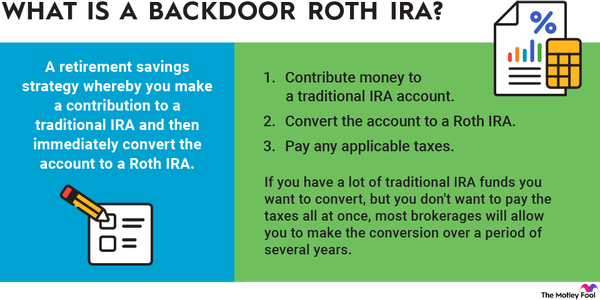

The only way for a high earner to still contribute to a Roth IRA is to use a backdoor Roth IRA strategy.

And, finally, the earlier you start contributing to a Roth IRA, the greater the tax advantages. You have more years to increase your earnings on a tax-deferred basis and more money to withdraw tax-free in retirement.

Benefits of Roth IRAs for kids

Benefits of Roth IRAs for kids

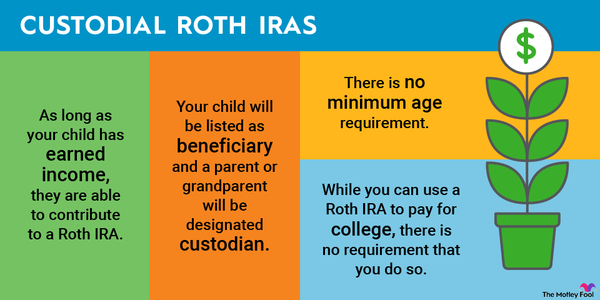

Children can also benefit financially from Roth IRAs for reasons similar to those given above and other reasons, too. An 18-year-old, for example, likely still has several milestones ahead -- including college, a first home purchase, and retirement. Roth IRA beneficiaries may access the funds without penalty at any age provided the money is used for college tuition or a down payment on a first home. Their Roth IRA contributions are also available at any time without restrictions. As adults, people with Roth IRAs may even retire a few years early if they have enough money in contributions to fund their living expenses.

Investors of any age may contribute to Roth IRAs as long as they have taxable income. A person's contributions can't exceed his or her earned income or the standard contribution limit for the year. And the standard income limits do still apply. For beneficiaries younger than 18 or 21, depending on the state where you live, custodians are required to supervise their accounts. The child assumes legal ownership of the Roth IRA upon reaching the age specified by your state.

Consider establishing a Roth IRA

Consider establishing a Roth IRA

If you meet the income requirements for Roth IRAs, it's smart to open an account and start investing now. That's still true even if you don't yet have a retirement strategy, or you're prioritizing a different financial goal. You can always access your contributions to a Roth IRA at any time. Meanwhile, you're creating a stream of tax-free retirement income and can benefit from the tax-deferred growth of your Roth account.