Roth IRAs offer some significant tax benefits, but, like all tax-advantaged retirement accounts, they're subject to annual contribution limits set by the IRS. In 2023, the Roth IRA contribution limits for most people are $6,500, or $7,500 if you're 50 or older. In 2024, these limits are $7,000, or $8,000 if you're 50 or older. But things get messier if you earn a lot of money.

Here's a closer look at how the IRS decides how much you're allowed to contribute to a Roth IRA annually.

How much can I contribute to a Roth IRA?

How much can I contribute to a Roth IRA in 2023 and 2024?

Your Roth IRA contribution limit depends on your tax filing status and your modified adjusted gross income (MAGI). If you don't know your MAGI, see below for information on how to calculate it.

The following table outlines how much you can contribute to your Roth IRA in 2023 and 2024:

Single, Head of Household, or Married Filing Separately if you did not live with your spouse at all during the year

You may contribute up to the annual limit if your MAGI is less than: $138,000 (2023) or $146,000 (2024)

You may contribute a reduced amount if your MAGI is between: $138,000 to $153,000 (2023) or $146,000 to $161,000 (2024)

You may not contribute directly to a Roth IRA if your MAGI is more than: $153,000 (2023) or $161,000 (2024)

Married Filing Jointly or Qualifying Widow(er)

You may contribute up to the annual limit if your MAGI is less than: $218,000 (2023) or $230,000 (2024)

You may contribute a reduced amount if your MAGI is between: $218,000 to $228,000 (2023) or $230,000 to $240,000 (2024)

You may not contribute directly to a Roth IRA if your MAGI is more than: $228,000 (2023) or $240,000 (2024)

Married Filing Separately if you lived with your spouse at any point during the year

You may contribute up to the annual limit if your MAGI is less than: N/A

You may contribute a reduced amount if your MAGI is between: $0 and $10,000

You may not contribute directly to a Roth IRA if your MAGI is more than: $10,000

If you're only able to contribute a reduced amount to your Roth IRA, you'll have to calculate your maximum contribution based on your income. Keep reading for more on how to do this.

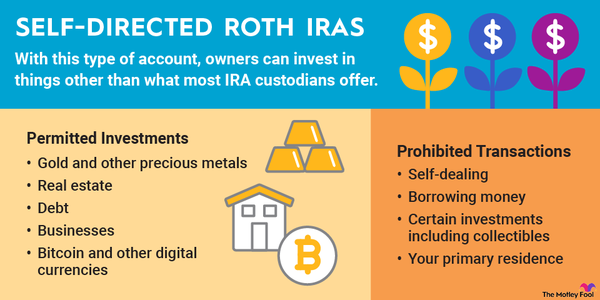

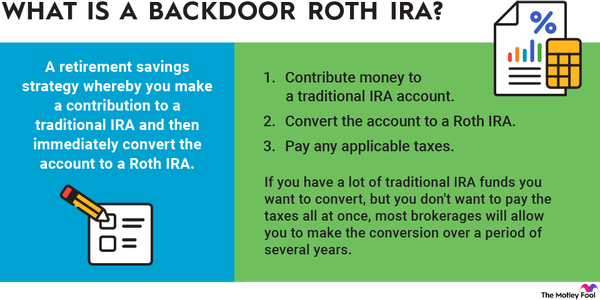

You still have options if you earn too much money to contribute directly to a Roth IRA in 2023 or 2024. You can use a backdoor Roth IRA in which you contribute money to a traditional IRA and then convert it to a Roth IRA. Or, if your income is that high, you may be better off contributing to a tax-deferred retirement account that will save you money this year rather than getting a tax break later on.

How do I calculate my modified adjusted gross income (MAGI)?

How do I calculate my modified adjusted gross income (MAGI)?

Modified Adjusted Gross Income

For many people, adjusted gross income (AGI) is the same as their MAGI. However, your MAGI is not listed on your tax return, so you will have to calculate it to be sure. To do this, start with your AGI. (Note that your AGI from past years is listed on previous tax returns if you want to start there, but you may have to do the math if you're looking for your AGI for the current year.) To calculate your AGI, take your gross income -- all the money you earn during the year -- and subtract certain tax-deductible expenses, including:

- Half of self-employment taxes, if applicable

- Student loan interest

- Tax-deferred retirement plan contributions

- Health insurance premiums, if you're self-employed

- Tuition and fees

- Health savings account (HSA) contributions

- Educator expenses

- Moving expenses, if you're a member of the military

- Penalties on early retirement account withdrawals

- Alimony paid, for pre-2019 divorce agreements

Then, because MAGI actually includes a few of those, add back these more common deductions, including:

- Student loan interest

- IRA contributions

- Tuition and fees

- Half of self-employment taxes

- Employer-paid adoption expenses

- Passive losses or passive income

- Rental losses

- Taxable Social Security payments

- Foreign earned income or housing exclusions

- Any losses from publicly traded partnerships

How much can I contribute to a Roth IRA if I'm a high earner?

How much can I contribute to a Roth IRA if I'm a high earner?

Use the following formula to determine how much you're eligible to contribute to a Roth IRA in 2023 and 2024 if you earn too much to make the maximum contribution:

- Calculate your MAGI.

- Follow the appropriate next step based on your tax filing status: If you're filing as Single, Head of Household, or Married Filing Separately (if you didn't live with your spouse all year), subtract $138,000 (for 2023) or $146,000 (for 2024) from your MAGI. If you're Married Filing Jointly, subtract $218,000 (for 2023) or $230,000 (for 2024) from your MAGI.

- If you're Married Filing Separately and did live with your spouse during the year, proceed with your MAGI straight to the next step.

- Divide your result from Step 2 by $15,000 -- or by $10,000 if you're Married Filing Jointly, a Qualifying Widow(er), or Married Filing Separately if you lived with your spouse at any point during the year.

- Multiply your result from Step 3 by the annual contribution limit for the year ($6,500, or $7,500 if you're 50 or older in 2023, and $7,000, or $8,000 if you're 50 or older in 2024).

- Subtract your result in Step 4 from your annual contribution limit.

High Net-Worth Individual (HNWI)

To illustrate how this works, consider a 40-year-old married couple filing jointly with a MAGI of $236,000 who want to make a Roth IRA contribution for 2024. They would:

- Subtract $230,000 from their MAGI of $236,000, leaving them with $6,000.

- Divide $6,000 by $10,000. This leaves them with 0.6.

- Multiply 0.6 by the $7,000 contribution limit for adults younger than 50 to get $4,200.

- Finally, they would subtract the $4,200 from the $7,000 limit and end up with a maximum contribution of $2,800 for each spouse for the year.

Keep in mind that all of your IRA contributions count toward the same limit, so if you've also contributed some money to a traditional IRA this year, that could reduce your maximum Roth IRA contribution even further. You must make sure your total annual individual retirement account (IRA) contributions remain less than $6,500, or $7,500 if you're 50 or older for 2023. In 2024, these limits increase by $500 to $7,000, or $8,000 if you're 50 or older.

Related retirement topics

Most people won't have to worry about Roth IRA income limits, but if you're a high earner, keep these in mind so you don't accidentally wind up with a Roth IRA excess contribution. Income and contribution limits may change from year to year, so check them every year to figure out exactly how much you're allowed to contribute.