18 Tax Moves You Should Make for 2018

18 Tax Moves You Should Make for 2018

It's never too early to start preparing

Another tax season is in the books, and unless you had to file for an extension, you've probably been hoping that after getting your tax returns prepared back in April, you could just forget about taxes for a while. Yet tax planning knows no season, and it's never too early to start thinking about how you can get yourself in position to save on your taxes in the coming year. Below, we've come up with 18 popular moves that can help you pay less to Uncle Sam in 2018.

1. Contribute to an IRA

Many people think about IRAs as a great last-minute way to save on taxes, because you get until mid-April of next year to make contributions for the current tax year. Yet the sooner you get money into an IRA, the more time your investments will have to generate tax-deferred income and gains. That can make a huge difference to your long-term returns, and with the ability for those of any age to contribute up to $5,500 to a traditional IRA and typically get a tax deduction for your contributions, using this type of retirement can produce hundreds or even thousands of dollars in tax savings.

2. Save in a tax-favored retirement plan

Many employers offer retirement plans as part of their benefits packages at work, and if you're fortunate enough to have access to a 401(k) or other workplace retirement plan, you can set aside even more money. The limits for 2018 are $18,500, and some employers are even kind enough to add matching contributions that are essentially free money to entice you to participate.

3. See if you can use a health savings account

Health savings accounts have even bigger tax benefits if you qualify. HSAs are tied to high-deductible health insurance plans, and for 2018, those with individual health coverage can contribute $3,450, while family coverage participants can put $6,850 into an HSA. Those contributions are deductible on your taxes, and you don't have to pay tax on investment income or gains if you use the money for qualifying healthcare expenses. That double benefit can give you even more savings.

4. Catch up if you can

IRAs, 401(k)s, and HSAs all offer the ability to make special catch-up contributions once you reach a certain age. Those over 50 can add $1,000 to the maximum IRA contribution and $6,000 to the maximum 401(k) contribution, while those over 55 can add another $1,000 to their HSAs as well. This perk is designed to help you make up for lost time as you near retirement age, so take advantage of it if you can.

5. Look at your tax withholding

You might have noticed that your take-home pay changed at the beginning of 2018, even if your salary stayed the same. That's because tax reform affected how much tax gets withheld from your paychecks. By looking at the information on your IRS Form W-4 with your employer, you can change how much money gets taken out for tax withholding. By making sure your withholding is as accurate as possible, you can avoid having to wait for a big year-end refund and instead keep as much of your hard-earned money upfront as you can.

6. Take advantage of a flex plan at work

Many employers offer flexible spending accounts, or flex plans for short, that let you set money aside for medical or childcare expenses. The benefit of these accounts is that the money you divert from your paycheck to the flex plan is pre-tax, and when you use the money for its intended purpose, you don't have to pay taxes on it. Maximum contribution limits apply, but the more important thing to remember is that unlike a health savings account, you risk forfeiting flex plan money if you don't use it by the end of the year. Check with your employer for your plan's details, but it can still be smart to use flex plans when you know that you'll need to use the money.

7. Move to a lower-tax state

Picking up and moving somewhere isn't necessarily something everyone can do, but the problem with tax reform is that you're now limited in how much in state and local taxes you can take as an itemized deduction. The maximum deduction is now $10,000, and if you live somewhere that the combination of state and local income and property taxes are high, you might routinely blow through that upper limit. Starting in 2018, paying more than the limit won't do you any good. Especially if you were already considering a move, taking taxes into account could lead you to a tax-saving decision.

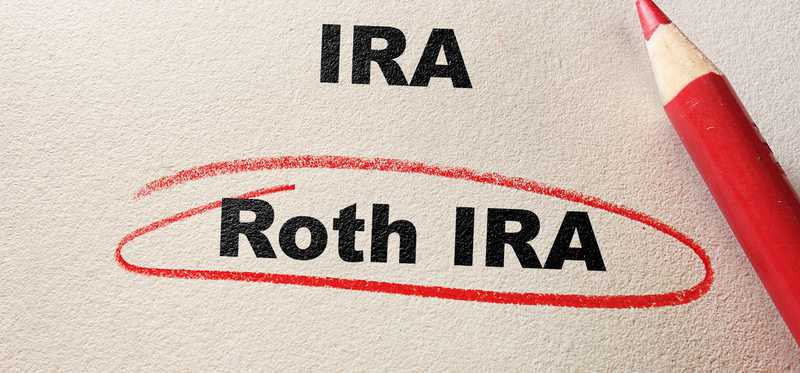

8. Consider a Roth conversion

Unlike traditional IRAs, Roth IRAs let your money grow on a tax-free basis, avoiding tax even when you take withdrawals in retirement. If all you have are traditional IRAs, you can convert all or part of them to a Roth, but you have to include the amount converted as taxable income in the current year. That won't save you on your taxes this year, but if you're in a low bracket and expect to be in a higher one later on, converting could end up saving you money in the long run.

9. Take another look at 529 plans

College savings plans, also known as 529 plans, have been around for years, letting you set money aside on a tax-deferred basis toward college costs. As long as you use the money for qualified educational expenses linked to college, you don't have to pay on the account's gains. Tax reform made it possible to spend 529 plan money tax-free on elementary and secondary school costs as well, so those who pay tuition for a child's K-12 schooling should take another look at how the plans might help them save on their taxes.

10. Sell losing investments early

If you own stocks or other investments that have lost money, selling them through a strategy called tax loss harvesting can get you a capital loss that you can use to offset capital gains on winning investments. You can also reduce other types of income by up to $3,000 per year with any extra losses you have. Many people wait until the end of the year to harvest tax losses, but doing so earlier can let you redeploy your savings more effectively, and there's no need to wait.

11. Donate winning investments to charity

If you have a big winner in your portfolio, giving it to charity can give you a double tax break. Not only do you not have to pay capital gains tax on your profits, but you can deduct the full value of the investment as long as you've held it longer than a year. This method is available for everything from stocks to cryptocurrencies, so if you're charitably inclined, look at your portfolio to see what might be a good candidate for a donation.

12. Take required minimum distributions if you have to

Those who have traditional IRAs or 401(k)s have to start taking mandatory withdrawals from those accounts once they turn 70 1/2 years old. The calculation of exactly how much you're required to take is a bit complicated, but the cost of failing to comply is severe: a 50% IRS penalty on the amount you should have taken. Most people have until Dec. 31 to take their required minimum distribution, but there's no need to wait that long if you'd prefer to have it sooner.

ALSO READ: 5 Things You Need to Know About Required Minimum Distributions

13. Own a business? Find the best structure

Tax reform had a big impact on businesses, creating a tough choice for owners. Corporate tax rates got cut from 35% to 21%, making incorporation a less expensive option for business owners. Yet pass-through entities like partnerships and LLCs also got a tax break. Taxes are only one element of whether one form of business is better than another, but every dollar you save in tax is another dollar to invest into making your business a success.

14. Pay estimated taxes if you need to

If you have substantial income from a source other than a traditional job -- whether it's investment income, self-employment, or a side job where you're treated as an independent contractor rather than an employee -- then you might need to make quarterly estimated tax payments. Failing to have enough tax withheld can lead to penalties if you don't, so take a look at Form 1099-ES and run the numbers to see whether you should be paying quarterly estimates and if so, how much will be enough to stop you from getting penalized.

15. Retired? Coordinate Social Security with IRA and 401(k) withdrawals

Many people don't realize that Social Security income can be taxable. Add up your income from other sources and then put in half of your Social Security benefits, and if that number is higher than $25,000 for singles or $32,000 for joint filers, you'll probably owe tax on a portion of your Social Security. To avoid that, timing when you claim Social Security with the taxable withdrawals from retirement accounts like IRAs and 401(k)s can help you keep your overall income under the threshold above which you'll get taxed.

16. Look at diverting investment income to your children

If you're in a high tax bracket and have children, you might be able to get a benefit by holding some investments in your children's names. Kids can earn up to $1,050 tax free, and the next $1,050 gets taxed at the child's lower rate. Moreover, new tax reform laws give kids a 10% rate on an additional $2,550 of income. The net result can be thousands in saved taxes compared to what you'd pay simply keeping investments in your own name.

17. Rich? Make bigger gifts tax-free

Tax reform also boosted the lifetime gift and estate tax exemption from $5.49 million in 2017 to $11.18 million in 2018. That number affects those who pass away, but it also establishes the limit for taxable gifts made during one's lifetime. Even those wealthy individuals who've routinely maxed out their lifetime taxable gifts can therefore make an additional $5.69 million in gifts in 2018 without having to pay any out-of-pocket tax thanks to the higher exemption. With the higher lifetime exemption set to go away after 2025, however, there's at least some uncertainty about what will happen after that date for those who made large gifts.

ALSO READ: 2018 Tax Exemptions and Deductions: What You Need to Know

18. Pay off a home equity loan

Tax reform took away the mortgage interest deduction for most home equity loans, so there's no longer a tax advantage for having that debt outstanding. The exception is that if you used the home equity loan to buy, build, or improve your home, the interest is still deductible. If you have both a regular mortgage and a home equity loan, it now makes sense to prioritize getting the home equity loan paid down first unless the deduction still applies -- or unless the interest rate on the mortgage is a lot higher.

Save everything you can

You don't have to make all of these moves in order to save a bundle when you file your tax return next year. But the more you do, the bigger your refund is likely to be come April 2019.

The Motley Fool has a disclosure policy.

HOW THE MOTLEY FOOL CAN HELP YOU

-

Premium Investing Guidance

Market beating stocks from our award-winning service

-

The Daily Upside Newsletter

Investment news and high-quality insights delivered straight to your inbox

-

Get Started Investing

You can do it. Successful investing in just a few steps

-

Win at Retirement

Secrets and strategies for the post-work life you want.

-

Find a Broker

Find the right brokerage account for you.

-

Listen to our Podcasts

Hear our experts take on stocks, the market, and how to invest.

Premium Investing Services

Invest better with The Motley Fool. Get stock recommendations, portfolio guidance, and more from The Motley Fool's premium services.