Updated

If you're looking to buy a home in Texas, the news is both good and bad. Homes are much more affordable in Texas compared to the United States as a whole. However, property taxes and homeowners insurance premiums are higher.

Your costs will ultimately depend on how much money you put down and what type of mortgage you choose. If you're looking to buy a home in the Lone Star State, use our Texas mortgage calculator to see what you can expect to pay.

If you're looking to buy a home in Texas, the news is both good and bad. Homes are much more affordable in Texas compared to the United States as a whole. However, property taxes and homeowners insurance premiums are higher.

Your costs will ultimately depend on how much money you put down and what type of mortgage you choose. If you're looking to buy a home in the Lone Star State, use our Texas mortgage calculator to see what you can expect to pay.

Texas housing market

The single family housing market in Texas is holding steady, with a median price at $360,000 in July 2023, a drop of just 1.5% over the same time the year before. Days on market have risen by 13 days in the same period, but were still very low at 34 days in July 2023.

Texas struggled with maintaining supply of all home types throughout much of the early pandemic, but is starting to see a tiny bit of uptick in options for buyers. In July 2023, there were three months of supply, 127,127 homes for sale, an increase of 3.1% over the same period the year prior.

This evening out of the market is starting to show even in contracts, with homes on average selling for just 98.2% of the listing price, down only marginally from the same time the prior year, when homes averaged 100.1% of their listing price. However, homes that sold above list price are decreasing, with just 20.8% doing so in July 2023, down significantly from 38% the same period in the prior year.

Check out this list of the best rated mortgage lenders to find a great rate for that Texas home purchase.

How do I calculate my mortgage payment?

Your mortgage payment is the sum of four things, collectively known as PITI: principal, interest, taxes, and insurance. If you live within the boundaries of a homeowners association (HOA), you may have to pay HOA fees too.

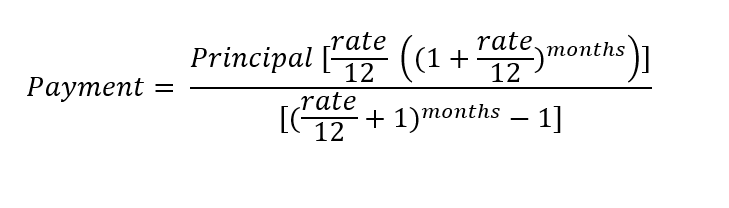

The formula to calculate your monthly mortgage payments by hand is complex. We recommend using a Texas mortgage calculator (like the one on this page) to get accurate results. However, if you'd like to try calculating it yourself, here is the formula:

The median single family Texas home sales price in the second quarter of 2023 was $305,497, quite a bit less than the $416,100 median sales price for single family homes across the entire United States. If you put down 20% on a home like this with a 7.5% interest rate and didn't owe any HOA fees, you could expect a monthly principal and interest mortgage payment of $1,708, according to our Texas mortgage calculator.

Let's look at each of these factors in a bit more detail to see how they might affect your mortgage payment on a Texas home.

Principal

The principal is the amount you borrowed to pay for your home. This is usually paid off over the course of 15 or 30 years. The principal will make up a larger share of your monthly payment over time.

If you can afford a higher down payment, you won't need to borrow as much for your home. That means you'll have less principal to pay off over the years. A lower principal also means a lower monthly mortgage payment.

To see the effects of various down payments on your monthly mortgage costs, try out different numbers in our above mortgage calculator for Texas.

Interest

Interest is the bank's payment for lending you money. The amount of interest you pay is based on your remaining balance on the loan and your interest rate. You can use the Texas mortgage calculator above to see the cost difference between varying mortgage interest rates. Check out our guide to current Texas mortgage rates if you're not sure what interest rate to expect.

In the first years after you buy your home, your remaining balance will be quite large, and so will your interest payments. Over time, as you pay down the remaining balance, your interest payments will get smaller and you'll start to make quicker progress toward paying off the loan.

Taxes

One of the biggest ways local governments earn money is by charging homeowners taxes on their property. The amount you'll pay towards taxes each month will vary depending on where you live and how much your home is worth. Texas homeowners have some of the highest property taxes in the country, ranking 14th out of 50 according to Tax-Rates.org.

The average property tax rate paid by Texans is 1.81% of the property's assessed fair market value. Your lender will normally take this money, put it in an escrow account, and then pay your property taxes for you each year. Once you've paid the mortgage off, you'll need to remember to do this on your own.

In our mortgage calculator for Texas, you can factor in property tax costs by using the "Additional Inputs" option.

Insurance

If you have a mortgage, your lender will also require you to get homeowners insurance. This is usually also rolled into your monthly mortgage payment. In Texas, the average annual premium for homeowners insurance in 2020 was $2,000, according to the Insurance Information Institute. Divided up into a monthly amount, that would be an additional $166.67 per month. This has a moderate impact on your monthly payment. You can see how insurance costs will affect your mortgage payments with our Texas mortgage payment calculator.

If you didn't make a very large down payment, your lender may also require you to pay for private mortgage insurance (PMI). This protects your lender in case you default on the loan. Typically, conventional mortgage lenders require you to put at least 20% down to avoid PMI.

Things to know before buying a house in Texas

If you're looking for a mortgage calculator for Texas, you'll also need to know some other information on home loans. Here are some things to keep in mind.

Check your credit score

One of the biggest factors affecting how much you pay for your mortgage is your credit score. The credit score needed for a home loan varies by lender, but generally a higher credit score is better. That's because your credit score directly affects your interest rate. Even small changes in your interest rate can add up and cost you thousands -- or tens of thousands of dollars -- more over the life of your loan. You can see the differences in cost between low and high interest rates by using our Texas mortgage calculator above.

If you're getting ready to get a home loan, one of the first things you should do is to check your credit score. And unless you have a perfect score, it's worth taking some time to improve your credit score before applying for a Texas mortgage.

Save up as large of a down payment as you can

Most financial experts recommend putting at least 20% down on a home. There are several reasons for this:

- It reduces the size of the mortgage you need to take out

- It gives you more equity in the home right off the bat

- It avoids an additional monthly PMI payment

First-time home buyers may find it difficult to come up with a 20% down payment. After all, a down payment in Texas would be around $72,000 based on the median Texas single family home sales price in July 2023. You'll also have to budget for closing costs, move-in costs, and other expenses.

Some mortgage programs allow you to buy a home with a low down payment, or even no down payment. Some examples include FHA loans and USDA loans. If you decide to consider one of these programs, you'll typically be required to pay PMI or a similar mortgage insurance payment.

This is where using a home loan calculator designed for Texas can come in handy. Use the Texas mortgage calculator above to compare the different monthly payments associated with various down payments and PMI costs. When you know how your loan terms translate to monthly mortgage payments, you can more easily decide on the mortgage program that's right for you.

Tips for first-time home buyers in Texas

Here are three things that first-time home buyers often overlook.

Look out for first-time home buyer programs

Buying a home is never cheap. Luckily, there are many programs out there that offer assistance specifically for first-time home buyers. If you're eligible, these can provide you a financial boost to get your new season started on the right foot. A good place to start is the Texas State Affordable Housing Corporation. There are many other programs available at different state, local, and federal levels.

Remember to budget for closing costs

Buying a home is expensive, even before you take out the mortgage itself. There are forms and deeds to be filed away, inspections to pay for, reports to check, and more.

As the buyer, you're usually expected to pay your portion of these fees. On average, they can range from 2% to 5% of the purchase price. You may be able to roll some of these costs into the mortgage, but others -- like home inspections -- you'll have to pay for out of pocket.

Remember to budget for home repairs

Don't forget to set money aside for regular home upkeep. There are a few rules of thumb for how much to budget, but most experts advise saving 1% to 4% of your home's value per year. In Texas, this means you'd need to set aside an additional $300 to $1,200 per month on average to cover maintenance and upkeep if you're buying a home today.

Still have questions?

Here are some other questions we've answered:

FAQs

-

Bringing as much of a down payment as you can afford can help make your mortgage easier to pay in the long term, but there are several programs that allow much less than 20%. For example, if you qualify for USDA or VA programs, you can bring as little as 0% down to closing. For other buyers, conventional loans start with down payments as low as 3% and FHA allows as little as 3.5% down.

-

The average closing costs for a home purchase in Texas are about $4,548. However, if you're only refinancing your mortgage, you may only pay $3,588.

Our Mortgages Experts

Kristi Waterworth has been a writer since 1995, when words were on paper and card catalogs were cool. She's owned and operated a number of small businesses and developed expertise in digital (and paper) marketing, personal finance, and a hundred other things SMB owners have to know to survive. When she's not banging the keys, Kristi hangs out in her kitchen with her dogs, dropping cheese randomly on the floor.

Ashley Maready is a former history museum professional who made the leap to digital content writing and editing in 2021. She has a BA in History and Philosophy from Hood College and an MA in Applied History from Shippensburg University. Ashley loves creating content for the public and learning new things so she can teach others, whether it's information about salt mining, canal mules, or personal finance.

Share This Page

We're firm believers in the Golden Rule, which is why editorial opinions are ours alone and have not been previously reviewed, approved, or endorsed by included advertisers. The Ascent does not cover all offers on the market. Editorial content from The Ascent is separate from The Motley Fool editorial content and is created by a different analyst team.

Please note that this calculator is not personalized financial advice and should not be considered or used as such. Nor are we promising that by use of this calculator, will you be able to save more money, preserve wealth, or otherwise.

Kristi Waterworth has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Zillow Group. The Motley Fool has a disclosure policy.