Financial Leverage and How it Can Help Your Business

While new business owners may hesitate to assume debt, using financial leverage to increase revenue and asset value can pay off in the long term. Learn more about financial leverage, including how to calculate your current financial leverage ratio, and the advantages and disadvantages of taking on debt.

Overview: What is financial leverage?

Financial leverage is the use of debt to acquire assets. When a business cannot afford to purchase assets on its own, it can opt to use financial leverage, which is borrowing money to purchase an asset in the hopes of generating additional income with that asset.

For instance, if your business borrows $50,000 from the bank to purchase additional inventory for resale, that is using financial leverage.

While a business with high financial leverage may be considered risky, using financial leverage also offers benefits, such as a higher return on investment (ROI). FInancial leverage can also appeal to stockholders who may see an increase in their initial investment as well.

While there are occasions when assuming debt is advantageous, business owners need to be aware that financial leveraging also has its downsides.

How financial leverage works

Financial leverage is when your company uses debt in order to purchase an asset that is expected to either increase in value or generate additional income. Here is an example of financial leverage:

Joe owns a small manufacturing company that makes parts for airplanes. He started his business four years ago, and it is currently housed in a small 5,000-square-foot facility.

Joe’s orders have increased by 50% over the past two years, but due to limited space for expansion, he has been unable to purchase additional equipment or hire more employees, making it difficult to keep up with the level of orders he’s receiving.

Joe has begun to look at purchasing a larger manufacturing facility, and currently has two options available. Option A allows Joe to purchase a new building that is slightly larger than his current facility, using cash in the amount of $250,000.

Option B allows Joe to use $100,000 of his own money and borrow an additional $650,000 from the bank in order to purchase a much bigger building. If Joe borrows from the bank, he will also have to pay 5% interest on the loan.

It’s difficult to determine from this information which option is best without considering future events, so let’s look at Option A and Option B to see what happens if Joe sells either building the following year.

Hypothetically, let’s say that the value of both buildings has increased by around 12%, with the smaller building selling for $280,000 and the larger building selling for $850,000.

| Option A | Option B | |

|---|---|---|

| Cash Payment | $250,000 | $100,000 |

| Assumed Debt | $650,000 | |

| Interest per Year | $32,500 | |

| Sale of Factory | $280,000 | $850,000 |

| Profit | $ 30,000 | $67,500 |

Table shows a hypothetical example of profit earned after the sale of the building

Going with Option A would have provided Joe with a profit of $30,000; a 12% return on his initial investment.

If Joe had chosen to purchase the first building using his own cash, that would not have been financial leverage because no additional debt was assumed in order to complete the purchase.

However, if Joe purchased the larger building using financial leverage with the assumption that the building would appreciate in value, his assumption was accurate, since he was able to sell the building for $850,000, earning a profit of $67,500 and a return on financial leverage of 67.5%.

The financial leverage formula

While there are a variety of financial ratios that business owners can use, including the popular debt to asset ratio, which is used to measure the amount of assets financed through debt or equity; the debt-to-equity ratio or financial leverage ratio is typically used to compare the amount of debt a company carries with the amount of equity on the books.

The financial leverage formula is:

Total Debt ÷ Shareholders Equity = Financial Leverage Ratio

Before you calculate financial leverage, you’ll need to do the following:

- Calculate the amount of debt that your business currently holds. Be sure to include both short-term and long-term debt when completing the calculation.

- If you have shareholders, you will need to multiply the number of outstanding shares by the current price of the stock.

Let's look at another example to get a better understanding of how the formula works:

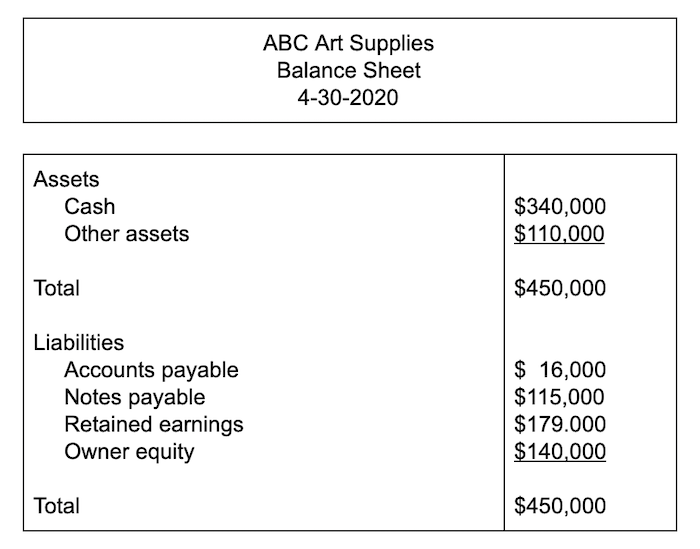

Sample Balance Sheet for ABC Art Supplies Image source: Author

If the owner of ABC Art Supplies wants to know their current financial leverage ratio, the first step they would need to complete is to add together all of the debt listed on their balance sheet above.

This would include both accounts payable and notes payable totals. If they had any other liabilities listed, those would need to be included as well.

$16,000 + $115,000 = $131,000.

With total debt calculated, ABC Art Supplies can now complete the financial leverage ratio calculation:

$131,000 ÷ $140,000 = 0.93.

A financial leverage ratio of 0.93 means that ABC Art Supplies is currently using $0.93 in debt financing for every dollar of equity financing. A financial leverage ratio of less than 1 is usually considered good by industry standards.

A leverage ratio higher than 1 can cause a company to be considered a risky investment by lenders and potential investors, while a financial leverage ratio higher than 2 is cause for concern.

What are the risks of financial leverage?

While financial leverage can be profitable, too much financial leverage risk can prove to be detrimental to your business. Always keep potential risk in mind when deciding how much financial leverage should be used.

Cash flow is another consideration. Being highly leveraged can directly affect current and future cash flow levels due to the principal and interest payments you’ll be required to pay for any loans.

You’ll also have to take the current financial leverage of your business into consideration when creating yearly financial projections, as increased leverage will directly impact your business financials.

Another risk is the possibility of losing money on a purchased asset. For instance, let’s say you buy a building for $600,000. Instead of paying for the building in cash, you decide to use $200,000 of your own money, borrowing the additional $400,000 needed.

Unfortunately, the building quickly loses value, and you are forced to sell it for only $410,000, saddling you with a loss of $190,000.

Always weigh the risks before making any major financial decisions.

Financial leverage should be tracked by all businesses

Financial leverage is a useful metric for business owners to monitor. While financial leverage can help grow your business and your assets, it can also be risky, particularly if assets expected to appreciate actually lose value.

However, the payoff can be tremendous, particularly for smaller businesses with less equity available to use.

If you’re still having difficulty understanding financial leverage, or haven’t yet advanced beyond basic accounting, be sure to consult with an accounting professional or CPA who can provide additional guidance on financial leverage and why it may or may not be a good option for your business.

Of course, having access to accurate financial statements is a must for calculating financial leverage for your company.

If your current accounting software application needs a boost, or you’re looking for more comprehensive reporting options, be sure to check out The Ascent’s accounting software reviews and find a product that works for you.

Alert: our top-rated cash back card now has 0% intro APR until 2025

This credit card is not just good – it’s so exceptional that our experts use it personally. It features a lengthy 0% intro APR period, a cash back rate of up to 5%, and all somehow for no annual fee! Click here to read our full review for free and apply in just 2 minutes.

Our Research Expert

Mary Girsch-Bock is the expert on accounting software and payroll software for The Ascent. She previously worked as an accountant.

We're firm believers in the Golden Rule, which is why editorial opinions are ours alone and have not been previously reviewed, approved, or endorsed by included advertisers. The Ascent does not cover all offers on the market. Editorial content from The Ascent is separate from The Motley Fool editorial content and is created by a different analyst team.

Related Articles

View All ArticlesBy: Ben Gran | Published on Jan. 26, 2024

By: Steven Porrello | Published on Feb. 28, 2024

By: Ben Gran | Published on Feb. 27, 2024

By: Maurie Backman | Published on Feb. 27, 2024

By: Chris Neiger | Published on March 2, 2024