Published April 22, 2024

Cost management is the process of estimating a project’s budget and instituting control measures to keep the project from overshooting that budget.

Projects cost money. You pay employees their salaries and contractors their fees. You buy materials and tools. You rent space and pay for equipment. You allocate funds for travel and other expenses.

If you have a big budget, you can employ more people to speed up project delivery. Or use better materials. Or better technology. If the budget is tight, you may have to scrimp and save here or there to provide wiggle room for more important aspects of the project.

Bottom line: No matter how big or small the allocated project budget, you have to keep expenses within the project’s financial limits -- exactly why cost management is such a critical piece of overall project management.

Overview: What is cost management for projects?

Project cost management, in a nutshell, is estimating the project’s budget and putting in place cost monitoring and control measures to keep expenses from exceeding that budget.

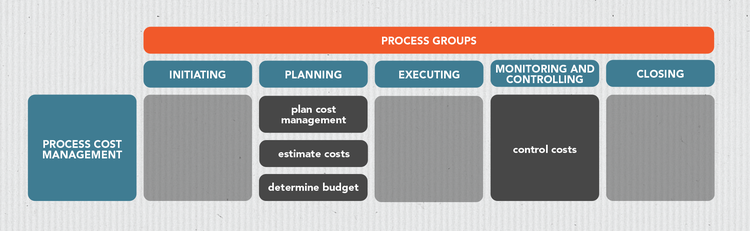

It’s one of the 10 knowledge areas within the Project Management Institute’s PMBOK Guide, a collection of project management standards and best practices, and is made up of four processes (more on these below), namely:

- Plan cost management

- Estimate costs

- Determine budget

- Control costs

Why is cost management important for small businesses?

Small businesses fail for many reasons, and cash flow or funding problems often top the list. So, when working on projects, project managers should carefully watch where the money goes.

Budget plans can go haywire in a number of ways -- suddenly sick critical personnel, late materials shipment, inaccurate expense forecasts, factors totally out of your control, etc. -- but if you’re paying close attention, and you have a cost management system in place throughout the duration of the project, you’re likely to make it through unscathed.

There are three major cost management advantages for small businesses.

1. Prevent the project from going over budget

According to the PMI’s 2018 Pulse of the Profession, the average percentage of budget lost when a project fails is between 27% and 37%, while the average percentage of projects completed within budget is between 43% and 67%.

Organizations with mature value delivery capabilities -- meaning those that can quickly adapt to changing market conditions, balance creativity and efficiency, and espouse continuous improvement -- fare better than their counterparts with low value delivery maturity.

This simply emphasizes just how crucial cost management is to every project. It may not prevent your project from going over budget, as the numbers above show, but it can help keep the overrun to a manageable level.

2. Promote efficiency

A dependable cost management strategy lets you estimate, with a certain degree of accuracy, how much money is needed for each project task, which you can then track, manage, and control throughout the project’s life cycle.

It also allows you to effectively allocate resources when and where they’re needed so work goes as planned, without delay.

3. Increase revenue

Project cost management ensures you don’t overspend, or it will at least allow you to contain spending as much as possible, on projects -- all while meeting timeline expectations and ensuring project quality. A penny saved is a penny earned, after all.

If you’re a small business operating on a small budget, effective cost management enables you to make the best use of your finite resources and pursue other value-adding projects.

How to master cost management for your projects

Inefficient project cost control is one major reason projects fail. But project cost management isn’t about control alone. According to the PMBOK Guide, it’s made up of four processes, each equally important.

A chart showing the different cost management processes and the project process groups in which they occur. Image source: Author

Process 1: Plan cost management

A project plan contains several subsidiary plans, and the cost management plan is just one of them. Other secondary plans are the resource management plan, the communication plan, and the risk management plan, to name a few.

During the plan cost management process, the project manager, with the help of the project team, creates a project cost plan that outlines how project expenses will be estimated, allocated, communicated, and controlled. Again, the aim is to prevent cost overruns.

A cost management plan can be customized to fit your project’s specific needs, but it typically includes:

- Unit of measurement (e.g., man hours vs. actual money value)

- Project budget (the total amount of money necessary to perform the project, plus buffers to account for both identified and unidentified risks)

- Cost baseline (the project’s time-phased spending plan)

- Rules for measuring performance (e.g., earned value vs. percent completion)

- How to track the budget while the project is in progress

- Cost reporting process

- Control thresholds, i.e., the amount of acceptable variance (percentage of deviation from the cost baseline) before action is taken

- How to make changes to the cost baseline

To create your project management plan, you’ll need these input documents:

- Project charter: A document developed during the early phases of the project, the project charter details pre-approved project resources, which can be used to flesh out a more detailed budget.

- Schedule management plan: The project management triangle concept, more popularly known as the triple constraint, illustrates the connection between the three major constraints of time, cost, and scope: Any change in one affects one of the remaining two or both. For example, if you need to accelerate the project schedule (as is the case in some agile projects), you’ll require more resources -- which means a bigger budget than originally planned -- or the product’s features reduced, or both. The schedule management plan establishes how you intend to develop, execute, and control the project schedule.

- Risk management plan: This plan details how you’ll handle project risks. As a result, you may incur costs. For example, you may have to purchase construction cost insurance or procure additional backup systems to ensure data doesn’t get lost or compromised.

Process 2: Estimate costs

Estimating costs is the process of approximating or forecasting the necessary financial resources to complete a project. To do that, you need a thorough understanding of the project’s scope, who’s doing which work, and the required length of time to complete the work.

Let’s say you want to digitize your company’s data. Depending on data amounts and how soon you want everything digitized, you may need a few people to a few dozen people working day and night to finish the work. From there, you can start estimating your costs.

Common techniques used for cost estimation include:

- Analogous estimating: From the word “analogy,” this technique uses previous similar projects to estimate the duration of your project and how much it will cost. It’s usually used when little project detail is available.

- Parametric estimating: Like analogous estimating, parametric estimating also uses historical information to compare the relationships between variables and estimate a cost. For example, if, based on past projects, it takes an hour to review a five-page document, and you need to review a total of 50 pages, then a task will take 10 hours to complete.

Process 3: Determine budget

The project budget is the total amount you’re allowed to spend on a project and is based on the cost estimate created in the previous process. The budget also serves as the cost baseline to compare the project’s cost performance against.

To determine the budget, you need the following information:

- Activity cost estimates

- Basis for estimates

- Project schedule

- Scope baseline (contains the scope statement, work breakdown structure (WBS), and an accompanying WBS dictionary)

- Contracts

- Resource calendar

- Organizational process assets (e.g., company policies, guidelines, or procedures that the project must adhere to)

Techniques and tools used to determine the project’s budget may include:

- Cost aggregation: Cost estimates are done at the activity level. With cost aggregation, you add all activity costs to the work package level. Work packages are tasks in the WBS hierarchy tree that can no longer be broken down.

- Funding limit reconciliation: When project funding is limited, this technique reconciles the project’s planned expenses within a period (e.g., one month) with the available funding for the same period. In other words, it ensures that funds are available for scheduled costs. As a result, work sometimes may have to be rescheduled.

- Reserve analysis: This involves adding buffers into the budget to protect the project from cost overruns. Contingency reserves are for risks that you know will transpire, while management reserves provide protection against risks that haven’t been identified.

Process 4: Control costs

Cost control is the process of tracking and monitoring actual project expenses, and then comparing them against the cost baseline to see if the budget needs to be adjusted.

Said differently, it compares how you’re doing budget-wise versus how you should be doing. This is so you can immediately spot plan variances or deviations, then make the necessary corrective adjustments to minimize risk.

Take note that adjustments to the project’s authorized budget follow an agreed-upon change control process.

Some tools and techniques to control costs include:

- Earned value management (EVM): A technique that measures project performance and progress, EVM lets you know whether the project is on track cost-wise and schedule-wise.

- To-complete performance index (TCPI): TCPI calculates the future cost efficiency required to finish a project within budget. It’s expressed as the ratio of the cost to complete all unfinished work to the remaining budget.

- Project management software: Project management software tools usually come with graphical, easy-to-understand dashboards for showing cost information in real time, making it easier to compare actual costs against the project’s budget.

Keep projects within budget with cost management

Operating under constrained circumstances is not a rarity in project management. It’s, in fact, a reality project managers contend with on an ongoing basis. But with the right cost management techniques up their sleeves, project teams have better chances of meeting agreed-upon budget guidelines.

Our Small Business Expert

Maricel Rivera is a business writer and researcher who has worked with the content teams of multiple B2B software companies. Some of her work appear on sites like Yahoo Small Business, Business.com, and Business2Community. When not writing, she’s most likely spending her time making something out of yarn.

Share This Page

We're firm believers in the Golden Rule, which is why editorial opinions are ours alone and have not been previously reviewed, approved, or endorsed by included advertisers. The Ascent does not cover all offers on the market. Editorial content from The Ascent is separate from The Motley Fool editorial content and is created by a different analyst team.

The Motley Fool has a disclosure policy.